ChatECB? An AI-Based Analysis and Summary of the June ECB Rate Decision

Membership required

Membership is now required to use this feature. To learn more:

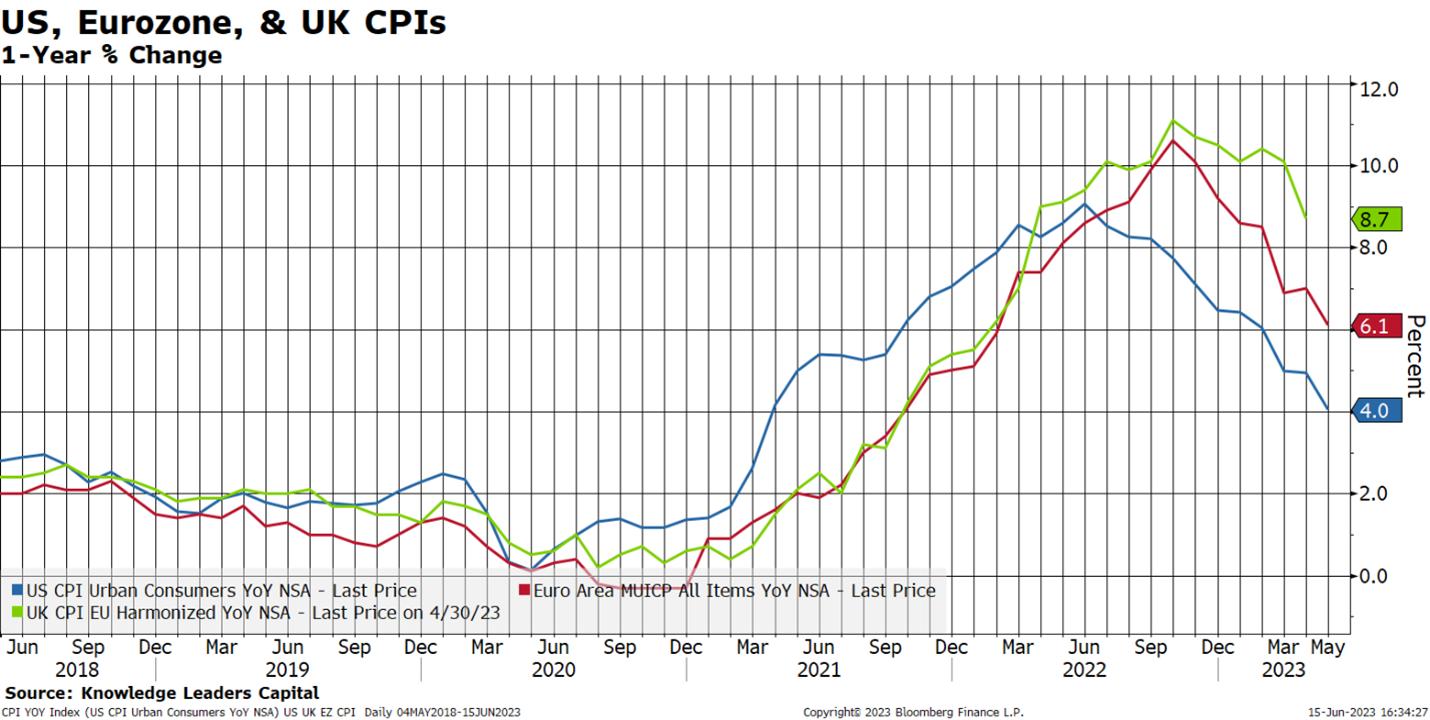

View Membership BenefitsFew were surprised when the ECB made a 25bps rate hike announcement yesterday. The move was aligned with analyst expectations, and in the face of 6.1% year-over-year Euro Area inflation, there was little room for ECB President Christine LaGarde to follow US Fed Chair Jerome Powell with a “hawkish pause.” In the chart below, you’ll notice that the ECB’s inflation has been moving parallel to US CPI, with the Euro Area about four months behind. While the Euro Area reported inflation of 6.1% in May, the US was able to post 6% year-over-year as of February. In this framework, a hike, and potentially two more to follow, was to be expected before a pause could occur.

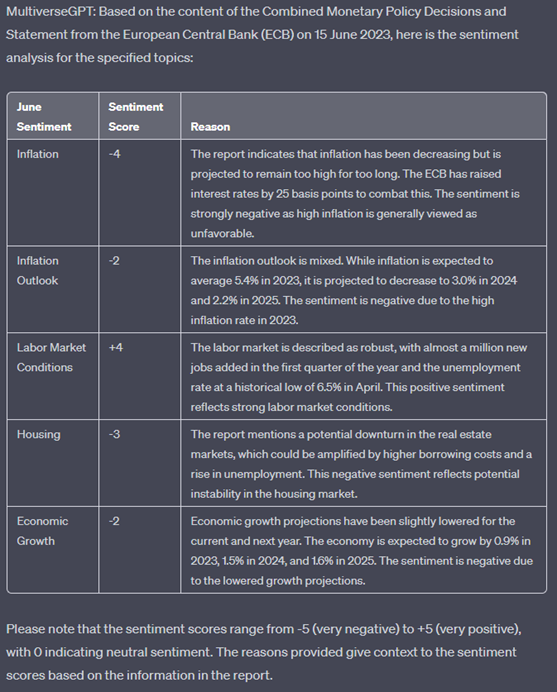

By using ChatGPT’s GPT4 Model with extensions, we were able to perform some basic sentiment analysis on the statement that may explain some of the initial drops in the Stoxx Index’s value.

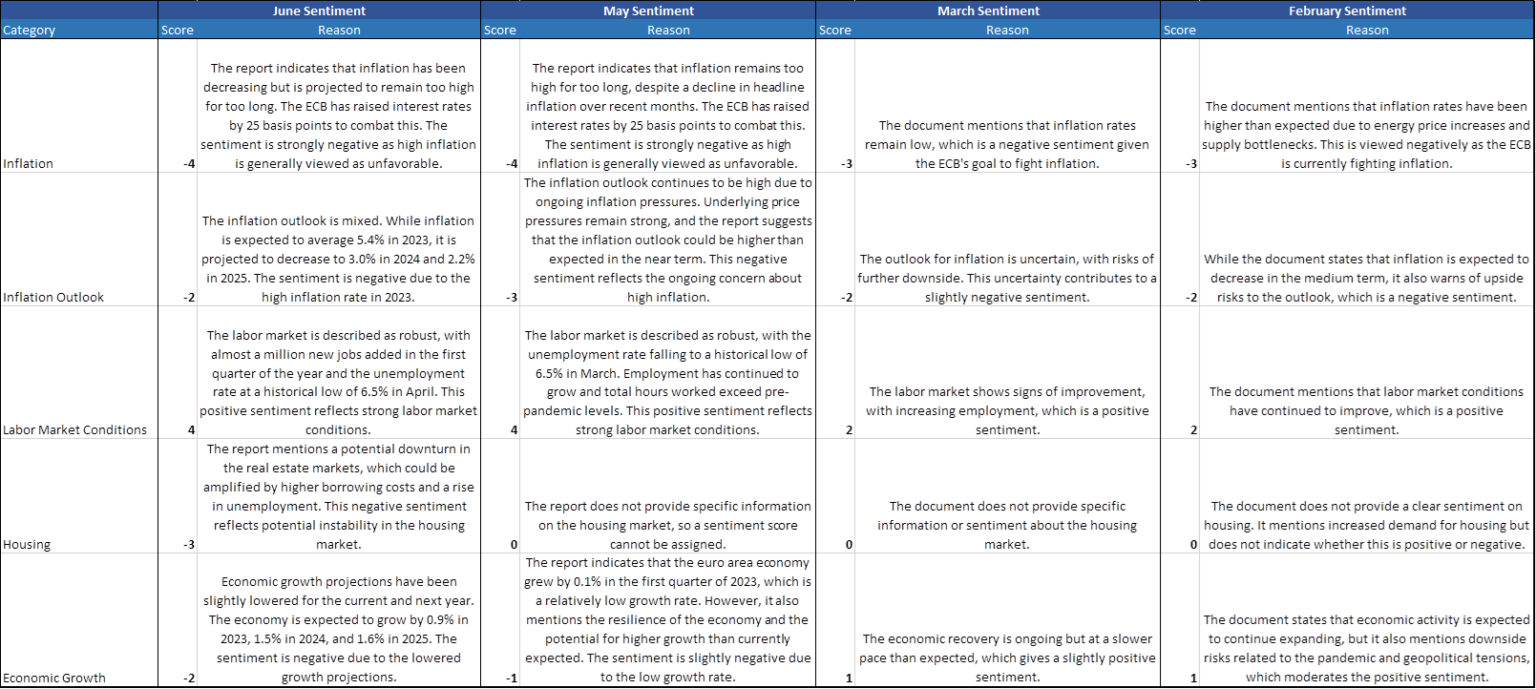

Compared to former statements, the sentiment of today’s report showed slightly better signs for the inflation outlook, but slightly worse projections for economic growth. Readings on current inflation levels and the labor market were unchanged from the last meeting.

Notably, this is the first statement that has mentioned the housing market, and the sentiment therein was quite low.

Below is a bulleted summary with key points from the press conference, generated using Wordtune AI and with transcription from OpenAi’s Whisper. The below has been edited slightly and formatted for clarity.

Statement:

- The ECB raised the three key interest rates by 25 basis points today to combat rising inflation.

- Euro system staff expect headline inflation to average 5.4% in 2023, 3% in 2024, and 2.2% in 2025, with underlying price pressures remaining strong. They have slightly lowered their economic growth projections for this year and next.

- At the same time, financing conditions have tightened, which is a key reason why inflation is projected to decline further towards our target.

- We will continue to follow a data-dependent approach to determining the appropriate level and duration of restriction, based on the inflation outlook, underlying inflation dynamics, and the strength of monetary policy transmission.

- The Euro Area economy has stagnated in recent months and is likely to remain weak in the short run, but strengthen in the course of the year.

- Conditions in different sectors of the economy are uneven, with manufacturing continuing to weaken and services remaining resilient. The labor market remains a source of strength.

- As the energy crisis fades, governments should roll back support measures and gradually bring down high public debt to avoid driving up medium-term inflationary pressures.

- Inflation fell further to 6.1% in May, according to Eurostat’s flash estimate, from 7% in April. The decline was broad-based, with energy price inflation resumed its downward trend, and food price inflation remaining high at 12.5%.

- Indicators of underlying price pressures remain strong, with past increases in energy costs pushing up prices across the economy. Pent up demand from the reopening of the economy is also driving up inflation, especially in services.

- The outlook for economic growth and inflation remains highly uncertain, with bad risks including Russia’s unjustified war against Ukraine and an increase in broader geopolitical tensions. However, the strong labor market and receding uncertainty could boost growth.

- Bad risks to inflation include renewed upward pressures on energy and food prices, a lasting rise in inflation expectations above our targets, and higher than anticipated increases in wages or profit margins.

- The monetary policy tightening continues to be reflected in risk-free interest rates and broader financing conditions, with credit becoming more expensive for firms and households. The annual growth of loans to firms and households declined again in April.

- The financial stability outlook has remained challenging since our last review in December 2022. Tighter financing conditions, combined with recent tensions in the US banking system, could give rise to systemic stress and depress economic growth in the short run.

- The Governing Council decided to raise the three key ECB interest rates by 25 basis points to ensure that inflation returns to its 2% medium-term target in a timely manner. It will continue to follow a data-dependent approach to determining the appropriate level and duration of restrictions.

Q&A:

Q: President Lagarde, six weeks ago you provided a fairly similar guidance in your statement and in the press conference, you said there’s more ground to cover and the ECB is not pausing. Do you see a reason for the ECB to contemplate a similar pause?

A: We have looked at data, revised our projection and increased all three rates by 25 basis points. We are determined to reach our target in a timely manner and will continue to apply the principles that we have applied today, data dependency, the three elements of our reaction function and moving meeting by meeting. To your second question, I don’t know what difference to make between a pause and a skip, but the ECB has hiked interest rates and will continue to hike at its next meeting.

Q: Annette Weisbach of CNBC has two questions. She wants to know what needs to happen for core inflation to actually come down, and what would make you rethink that it’s enough when it comes to tight financial conditions.

A: I wish I could give you a simple answer, but unfortunately it doesn’t work like that. We look at multiple cuts and subsets of inflation to arrive at what is the poorest of the core, and we need to be confident that it is heading down. We measure the strength of transmission at each and every step of the way from market rates, bond prices, credit by banks, banking funding, and ultimately to inflation, so that we head towards our target.

Q: Alexander Weber of Bloomberg News asks how alarmed he is by the upward revision to the 2025 inflation outlook and whether he thinks he can achieve the 2 percent inflation target with unemployment remaining as low as it is now.

A: The core inflation revision that we have decided for 2024 is the reason why we are making the monetary policy decision that we make today, and why we are thinking that unless there was a material change to the baseline, we would again hike interest rates in July. We spent a lot of time on the labor market, and wages are playing a significant role as a driver of inflation. The output is stagnant, and there is an issue of unit labor cost, which clearly has an impact on inflation.

Q: Good afternoon. I was surprised by how strong the revision of the core inflation projection was, and I have a question about the decision today.

A: The large part of the revision to core inflation is attributable to the unit labor cost, and the rest is based on past upward surprises. The decision to change the policy rate was informed by data that came in after the last projection was made in March. According to projections, the inflation target will not be reached in the next three years. However, the central bank is confident that it will remain at 2%. We are seeing some effects of the decisions we have made in the last soon to be a year, both in terms of speed and volume of hikes. We are monitoring the lag time very carefully to see how fast it moves.

Q: The Bank of Canada recently restarted its rate hikes, saying that it thought the neutral rate had risen from its previous expectations. Do you think similarly, and could the ECB consider skipping rate rises, certain meetings, perhaps going to only changing policy when you are issuing forecasts?

A: It’s difficult to say whether we’re in the same position as the Bank of Canada because we did not pause. So in a way, we don’t have to ask ourselves whether we are at neutral rate or not. We believe that we have ground to cover.

Q: Isabella Bufaki of Il Sol Event Quatorra asked two questions. She asked how the governing council is concerned that the ECB is going far and how far do they look at growth weakening in response to their policies.

A: We will be as restrictive as long as needed to make sure that we reach our destination of 2.2% in 2025, which is why we are making the decisions that we are making today and later on. Banks will reimburse 477 billion euros that they had borrowed under Teltrow at the end of June and in the first days of July. The repayment was known for a long time, and banks have done their funding plans to avoid a massive reimbursement. The APP reinvestment will be completed at the end of June, and we will let runoff take place as of July. We will be very attentive to this process, and we will use all the tools available if needed.

Q: You’ve touched on the problem of wage increases and corporate profits at your speech at the European Parliament. How confident are you that the relevant parties will moderate on these issues?

A: The labor market situation and the employment situation is the good news in Europe, and we see unemployment rate going from 6.5 percent to 6.3 percent. We also see wages continuing to increase, and we are confident that the European Central Bank will return inflation to 2 percent. The persistency of inflation is due to the unit labor cost, which is going to be high, and services are going to continue to go strongly. Energy costs are going to continue to fade, and we expect that resistance of inflation to gradually fade away.

Q: Andres Stumpf of Expansion asked if the risk of an inflation spiral has increased since March. Madame Lagarde responded that we are not seeing second round effect and we are not seeing this wage price spiral.

A: The ECB is seeing a revision in the core inflation projection, which is caused by unit labor cost, which is slightly different from wages. The ECB is not seeing a wage price spiral, which would cause a second-round effect.

Q: Javier Luengo of Negotiostv asked if the ECB would be able to increase the balance sheet reduction on July onwards and if they had room to reduce it further. The ECB said they had room to reduce it further, but the teletro reimbursement was due at the end of June.

A: We decided to stop reinvesting redemptions under APP and let APP move into a runoff mode. The PEP continues as indicated in the only part of forward guidance that we still have.

Disclosures

The information presented here is for informational purposes only and is not to be construed as an offer to sell, or the solicitation of an offer to buy securities. Some investments are not suitable for all investors, and there can be no assurance that any investment strategy will be successful. Hyperlinks may be included in this message that provides direct access to other internet resources, including websites. While we believe these links are to reliable sources, Knowledge Leaders Capital (“KLC”) has no control over the accuracy or content of information contained on these sites. Although we make every effort to ensure such links are accurate, up-to-date, and relevant, we have no control over pages maintained by external providers. The views expressed by these external providers on their own web pages or on external sites they link to are not necessarily those of Knowledge Leaders Capital.

The information provided on this blog is for illustrative or example purposes only and should not be construed as KLC’s opinion or investment outlook. As of the most recent quarter-end, the named companies may have been held by KLC. For full information including additional policies and full disclosures, please visit our website: KnowledgeLeadersCapital.com.

Any reference to Index performance does not represent the performance of any investment product offered by Knowledge Leaders Capital, LLC. An investor cannot invest directly in an index. The performance of the client account may vary from the Index performance. Index returns shown are not reflective of actual investor performance nor do they reflect fees and expenses applicable to investing.

Companies are selected for “Spotlights” based on high levels of innovation activities in their respective industries and illustrate innovation being employed across all sectors and geographies. Spotlight selection is separate from stock selection by the investment team. Spotlights are not necessarily representative of investment opportunities and can be selected regardless of investment performance or inclusion as a KLC holding.

A message from Advisor Perspectives and VettaFi: To learn more on this and other topics, check out our full schedule of upcoming CE-approved virtual events.

Membership required

Membership is now required to use this feature. To learn more:

View Membership Benefits