“Inflation has not really moved down. It has not so far reacted much to our existing rate hikes, and so we’re going to have to keep at it.”

— Jerome Powel FOMC Press Conference 6.14.23 (Transcribed by Open AI’s Whisper).

Going into the Fed meeting today it seemed like the consensus was toward a skip, pause, or possibly a full-on stop in raising interest rates going forward. Indeed, there are reasons to be optimistic about inflation coming down despite currently sticky “core numbers.” For instance, we observe CPI ex-shelter is currently at 1.8% and since rent is tumbling and housing costs make up a third of CPI, we’re expecting inflation numbers to come in cooler in coming months.

In preparation for today’s meeting, we used our AI tools first to look back at pre-FOMC blackout comments by Jerome Powell and Neel Kashkari, two of the most hawkish FOMC members. Then we looked at Powell’s press conference today and compared sentiment on topics like inflation to the previous three meetings.

Here’s a synopsis of their comments a few weeks ago from Powell’s panel interview with Ben Bernanke, and Kashkari’s CNBC interview, with transcripts summarized by ChatGPT. They pointed to these hawks seeming to become more dovish at the time. The financial press had caught on in recent days to the idea of a “skip” looking more likely. However, the FOMC’s dot plot suggests as much as two more hikes in the next year to bring inflation under control.

Pre-blackout comments summarized by ChatGPT:

- Based on the comments by Jerome Powell, he seems to take a balanced and data-dependent approach towards monetary policy. His stance appears neither strictly hawkish nor dovish, but rather guided by the evolving economic data and conditions.

- He talks about the progress the FOMC has made in policy tightening and notes that the current policy stance is restrictive. He also acknowledges uncertainty about the lagged effects of the tightening so far and the impact of recent banking stresses.

(Ok, Chat, you might be onto something here, and in fact today Powell made references to still being data dependent. But as expected, a hawkish tone was likely on the docket in the event of a pause/skip.)

Neel Kashkari’s comments summarized here by ChatGPT are relatively dovish.

- Concern about Banking Stability: Kashkari advocates for a simpler and more effective solution to banking stability, higher equity capital requirements. This typically reflects a dovish stance, as it emphasizes stability and caution over potential economic growth from riskier banking activities.

- Emphasis on Inflation Management: Kashkari is focused on bringing inflation back down to the Fed’s target of 2%, indicating that he’s not willing to let inflation run high for an extended period. However, he seems cautious about the pace of interest rate hikes, reflecting concern about the potential negative effects on the banking sector and overall economy. This balanced stance leans towards dovish.

- Hesitation about June Rate Hike: Kashkari mentions that it’s a “close call” between raising rates in June or skipping, showing his hesitance about moving too quickly. This again leans dovish.

- Emphasizing Stability Over Growth: Kashkari repeatedly stresses the need for stability in the banking sector and cautions against risk-taking behavior that could lead to instability. This is generally seen as a dovish stance.

(That’s interesting. Kashkari was supposed to be a super hawk-like Bloomberg’s Fed spectrometer labels him. It sounds here like he’s almost going back to his dovish roots.)

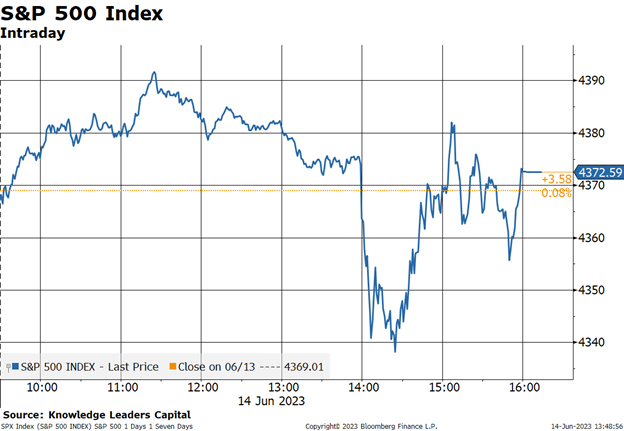

Nevertheless, the Fed’s DOT Plot Projection, released with the policy decision at 2pm Eastern, caused US equity markets to instantly dive, but then recover when Powell walked back the impression that two hikes were imminent, only to decline once more before a later afternoon rally as comment sentiment seemed to deteriorate later in the press conference.

Sentiment hit a press conference low according to SpeakAI’s analysis, when Powell addressed the deleterious effects of inflation on society. Powell’s transcribed comments around this included:

“So we’re still talking about, I mean, what is as strong a labor market as we’ve seen in, you know, a half-century here in the United States. So overall, the unemployment of 3.7 percent is three-tenths higher than it was measured to be at the last-a month ago, but still, it’s extraordinarily low. And so it’s a very, very tight labor market.” –Powell

“People on a fixed income are hurt the worst and the fastest by high inflation.” –Powell

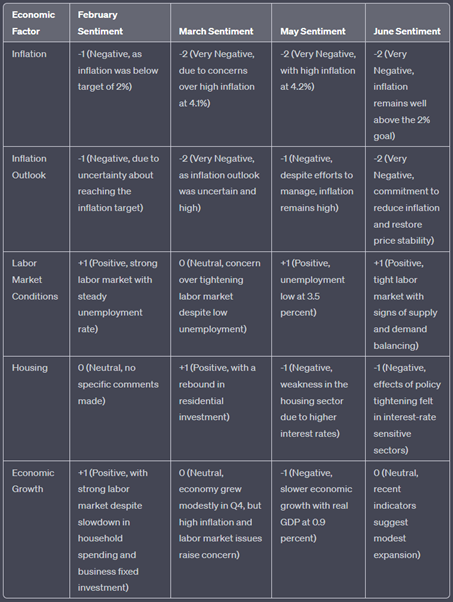

Is the Fed suddenly more hawkish than expected? Here’s a table comparing sentiment according to ChatGPT for the June meeting and the previous three opening comments made by Powell. As we can see, Chat is picking up on Powell’s hawkish tone today in his opening comments on inflation:

Indeed, in the press conference, Powell reiterated later in the Q&A portion of the press conference. “Inflation has not really moved down.”

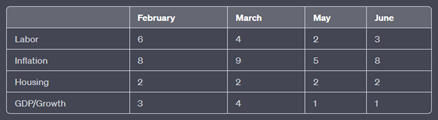

Here’s the number of times each of these words was mentioned in Today’s FOMC meeting, compared to the previous three meetings (according to ChatGPT). Inflation discussion was back on the menu after a brief credit crisis scares interlude in May.

ChatGPT summarizing Powell’s comments during the press conference on inflation gives us the following notes:

- Inflation remains well above the longer-run 2 percent goal, and the process of getting it back down to 2 percent has a long way to go.

- The Federal Reserve remains committed to reducing inflation and restoring price stability, as it is guided by its mandate to promote maximum employment and stable prices for the American people.

- The risks to inflation are still viewed as being on the upside, but the balance between inflation and underinflation is getting closer to being in balance.

- The Committee recognizes the importance of wages in driving inflation and expects wage increases to continue gradually, consistent with 2 percent inflation over time.

On rents, which make up a large percentage of inflation Chat summarizes Powell’s comments like this:

- In terms of housing services inflation, you are seeing new rents, and new leases coming in at low levels, and it’s really a matter of time as that goes through the pipeline.

- I think we’re seeing rents and house prices filtering into housing services inflation, and I don’t see them coming up quickly.

- We haven’t seen the slowdown in rents show up in CPI yet, but Governor Waller talked about how that might play into today’s outcome.

- We need to see rents bottom out or at least stay quite low in terms of their increases, because we want inflation to come down, and we want to see that.

Thus, rents will play a crucial role in how the Fed responds in the coming next meetings.

Here are ChatGPT’s top ten most important takeaways from today’s meeting:

- Inflation remains a major concern, with prices well above the 2 percent goal.

- The U.S. economy experienced a significant slowdown last year, impacting business fixed investment.

- The labor market remains tight, with robust job gains, indicating positive employment conditions.

- The FOMC has significantly tightened monetary policy, but its full effects are yet to be felt.

- The Committee is focused on its dual mandate of maximum employment and stable prices.

- There are signs that supply and demand in the labor market are coming into better balance, easing upward inflation pressures.

- The housing and investment sectors are experiencing the effects of policy tightening, which will take time to fully realize.

- Inflation has moderated somewhat since last year but remains high, requiring further attention.

- The Committee’s confidence in waiting to take action is based on elevated core inflation and ongoing recovery in interest-rate-sensitive sectors.

- The median projection for total PCE inflation suggests a gradual decline in the coming years.

Disclosures

The information presented here is for informational purposes only and is not to be construed as an offer to sell, or the solicitation of an offer to buy securities. Some investments are not suitable for all investors, and there can be no assurance that any investment strategy will be successful. Hyperlinks may be included in this message that provides direct access to other internet resources, including websites. While we believe these links are to reliable sources, Knowledge Leaders Capital (“KLC”) has no control over the accuracy or content of information contained on these sites. Although we make every effort to ensure such links are accurate, up-to-date, and relevant, we have no control over pages maintained by external providers. The views expressed by these external providers on their own web pages or on external sites they link to are not necessarily those of Knowledge Leaders Capital.

The information provided on this blog is for illustrative or example purposes only and should not be construed as KLC’s opinion or investment outlook. As of the most recent quarter-end, the named companies may have been held by KLC. For full information including additional policies and full disclosures, please visit our website: KnowledgeLeadersCapital.com.

Any reference to Index performance does not represent the performance of any investment product offered by Knowledge Leaders Capital, LLC. An investor cannot invest directly in an index. The performance of the client account may vary from the Index performance. Index returns shown are not reflective of actual investor performance nor do they reflect fees and expenses applicable to investing.

Companies are selected for “Spotlights” based on high levels of innovation activities in their respective industries and illustrate innovation being employed across all sectors and geographies. Spotlight selection is separate from stock selection by the investment team. Spotlights are not necessarily representative of investment opportunities and can be selected regardless of investment performance or inclusion as a KLC holding.

A message from Advisor Perspectives and VettaFi: To learn more on this and other topics, check out our full schedule of upcoming CE-approved virtual events.

© Knowledge Leaders Capital

Read more commentaries by Knowledge Leaders Capital