Investor activism in Japanese companies has been the subject of a fair amount of recent conjecture. Specifically, foreign investors have been concerned about the relative prevalence of minority interest and the ghosts of fading Keiretsus on Japanese companies’ financial statements. This, combined with significant insider shareholding and apparent unfriendliness to shareholders, has led investors to worry about companies failing to prioritize profitability and returns to investors. We conducted a preliminary statistical inquiry into the first of these grievances.

We tested the following metrics, drawn from each company’s fiscal year-end reports and stated in USD, and correlated them with the percent price return in Japanese Yen over the past five years.

- -Accumulated minority interest as a percentage of total capital and of total assets.

- -The percentage of shares outstanding closely held (held by insiders, institutions, etc.)

- -Minority interest expense as a percentage of the cost of goods sold.

- -Equity in affiliate income as a percentage of sales.

As is standard practice with statistical hypothesis testing, we defined our hypotheses as follows for each of the items listed above.

H0 (null hypothesis): There is no statistically significant correlation between a given financial metric and five year % price return. This would be verified by a correlation’s P-value above 0.05.

H1 (alternate hypothesis): A given financial metric has a statistically significant correlation with price returns. A correlation P-value below 0.05 would identify a given correlation as likely statistically significant and would be the cause for rejecting the null hypothesis for a given metric.

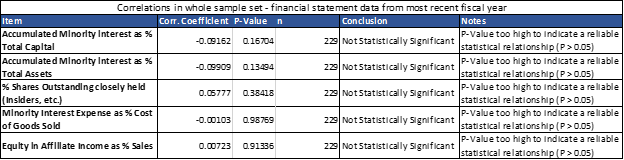

Starting with a universe of 456 mid- and large-cap Japanese companies, we trimmed out any without fully reported and complete data for the items specified above, leaving us with a sample size of 229 companies. Testing the correlations described above yielded the following results.

Not only do none of the metrics tested show a strong correlation with price returns, none of the correlations listed above have a P-value anywhere near 0.05, meaning that none of them are statistically significant. We cannot reject the null hypothesis for any of the tests performed.

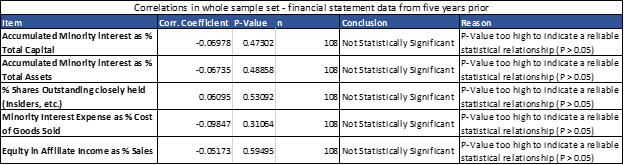

We repeated the test drawing financial statement items from five fiscal years ago instead of the most recent items, with a smaller sample size of 108 companies, but came up with similar results.

Again, none of the tests performed resulted in either a particularly strong correlation between price returns and the tested metric from five years prior, or a statistically significant result as determined by the resulting P-value. There is, of course, always room for more testing with a broader dataset and different data points, but our work thus far is fairly conclusive in providing support for the null hypothesis.

Our analysis shows that none of the financial statement items we tested which are held by many Western investors to be highly prevalent, endemic drags on the profitability and investment return prospects of Japanese companies show a strong relationship with price returns in Japanese Yen over the past five years. Nor are they even especially prevalent, which we will explore further in coming posts next week. Knowledge Leaders Capital’s quarterly strategy report will dive deeper into this line of inquiry as well, so keep an eye out for more on this topic.

A message from Advisor Perspectives and VettaFi: To learn more on this and other topics, check out our full schedule of upcoming CE-approved virtual events.

© Knowledge Leaders Capital

Read more commentaries by Knowledge Leaders Capital