Truist Financial Corporation is a purpose-driven financial services company committed to inspiring and building better lives and communities. Truist has a leading market share in many high-growth markets in the country. The Company offers a wide range of services. Headquartered in Charlotte, North Carolina, Truist is a top 10 U.S. commercial bank. Truist Bank, Truist’s largest subsidiary, was chartered in 1872 and is the oldest bank headquartered in North Carolina. Truist Bank provides a wide range of banking and trust services for clients through 2,123 offices as of December 31, 2022, and its digital platform.

Truist Financial Corporation is the result of a 2019 merger between BB&T and SunTrusts Banks (it was actually BB&T buying SunTrusts Banks but the official company stance was that was a “merger“). At the time of the merger, it was reported that the new entity would have a combined $324 billion in deposits, and adding to the $442 billion in assets would have made Truist Bank the sixth largest bank in the United States.

FAST Graphs Analyze Out Loud Video

Size matters in the banking industry.

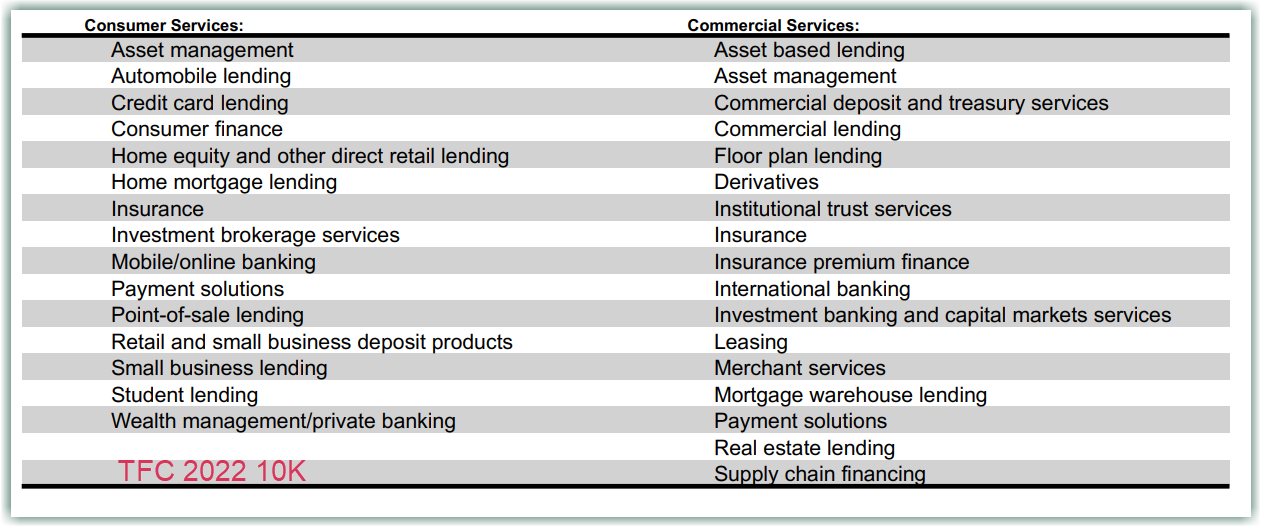

With size comes a larger pool of customers from whom to draw capital from. With size comes economy of scale as it does not cost much more to extend the same digital services for instance across one million depositors or fifty million depositors. With size, revenue sources can be diversified. Prior to the merger, SunTrust Banks and BB&T each had their niche. SunTrust Banks was focused on the commercial side of the business and on larger clients while BB&T's focus had a larger chunk of its income coming from the insurance business. Together, each niche area not only becomes a smaller piece of the combined pie but as a whole, the new entity can offer a wider array of products and services, sufficient to rival the four largest banks (JPMorgan Chase, Bank of America, Wells Fargo, and Citibank). Now, Truist is able to serve both individual depositors looking for home mortgage lending and automobile lending, as well as business owners looking for payment solutions and supply chain financing.

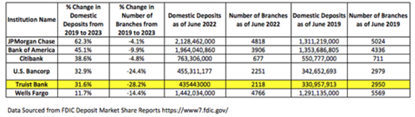

When compared to the four largest banks (JPMorgan Chase, Bank of America, Wells Fargo, and Citibank) and US Bancorp, it is clear that size in terms of deposits confers clear advantages. JPMorgan Chase had the second-largest pool of domestic deposits in 2019, and it was able to grow that by 62.3%, surpassing Bank of America. And that was before it took over another $100 billion in deposits from First Republic Bank just this month. Bank of America did well too; it had the largest amount of domestic deposits as of June 2019 and grew that by an impressive 45.1% by June 2022 coming into second place. Banks like Truist, US Bancorp, and Citibank with smaller deposits grew too but not as much as JPM or BAC.

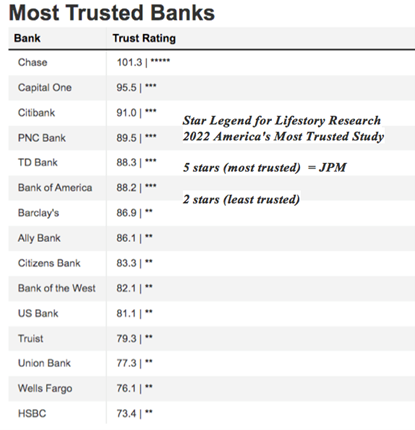

Wells Fargo is the only odd one out with the third largest deposits in 2019 right after JPM and BAC but grew deposits only 11.7%. I will attribute that to the reputation of the bank. Lifestory conducted a study in 2022 that surveyed 17,614 people in the evaluation of banks throughout the year. According to the researcher, “trust” is measured by a Net Trust Quotient, which is derived from consumer answers to several questions about their impression of each bank, including how trustworthy they believed it to be. Wells Fargo scored 2 stars and fall in the least trusted category.

Why Truist Financial Corporation?

Since JPM is clearly the best bank, should we not just invest in it?

A few reasons to consider Truist Bank instead of the rest.

Truist is Large

In March of 2023, a lot of uncertainty and fear were going around with one bank failing and another. Lots of misinformation were making its rounds on social media, amplifying these uncertainties even more. Many regional banks came under pressure simply by association and their stock prices took massive hits and fell.

Many people may still associate Truist Bank with its former self, be it SunTrust Banks or BB&T, and think that it is still a regional bank, similar in asset size to the fallen First Republic Bank ($212 billion), Silicon Valley Bank ($211 billion) and Signature Bank ($110 billion).

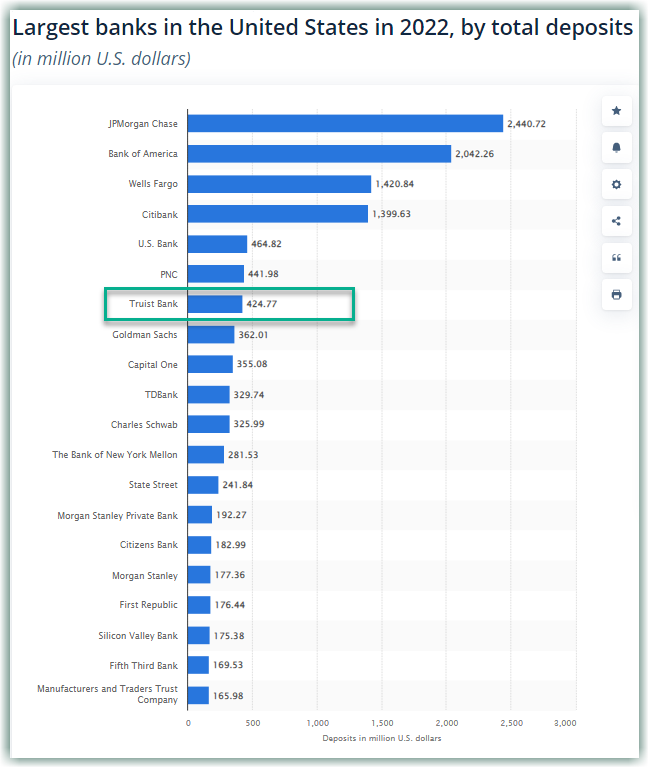

The fact is Truist is more than twice are large as these former peers. In 2022 Truist was already the seventh-largest bank in the United States by total deposits.

Truist is Profitable

Truist Financial has the largest net interest income growth rate of 16.98% in the past three years, outpacing all the other banks in comparison by a mile, even against the mighty JPM.

Net interest income is a measure of a bank’s profitability and as a newly merged bank, Truist has grown its net interest income by 16.9% in the past three years.

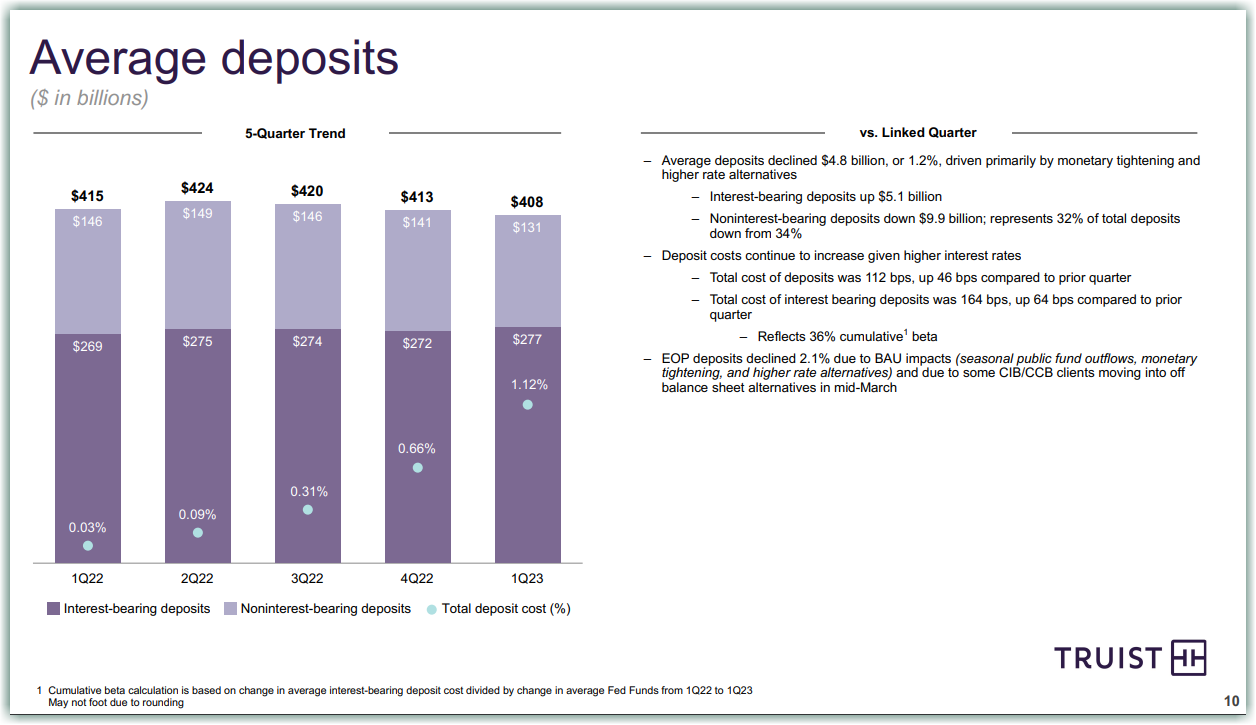

This is not to say Truist is immune to the wonky interest rate environment that banks are experiencing now. On a quarter-to-quarter basis, Truist registered a decline in net interest income of 2.8% and net interest margin fell by 7-8 basis points or 0.07%-0.08%.

However, the banking crisis of 2023 did not result in a massive outflow of depositors. The average deposits have declined 1.2% from Q4 2022 to Q1 2023 but that was not a rush-to-the-exit situation.

CEO Bill Rogers shared in more detail during the Q1 2023 earnings call,

Within the month of March, more deposit flows were concentrated in the period from March 11 to March 18 and have largely been business as usual since including through yesterday. Positive outflows during mid-March were primarily related to CIG and CCB clients. We chose to diversify in the money market mutual funds and in some cases, across multiple bags. These outflows tended to be a higher cost of non-operational deposits.

We also experienced deposit inflows as we’re both attracting new clients and expanding our relationships with existing clients. Retail production continues to improve due to our shift from integrating to operating and leading with the value proposition of Truist One. In the first quarter, Truist saw record new deposit production, including an 18% year-over-year uplift in branch account openings with improved client retention driving strong net new account performance.

Truist Is Undervalued

We like to be guided by sages of the past. We like it even better when the sages still walk and breathe among us.

Regarding when to buy, Peter Lynch had this to say,

My system for over 30 years has been this: When stocks are attractive, you buy them.

Examining Truist within the timeframe of its existence as a merged entity, a few things made it clear that Truist is attractive now.

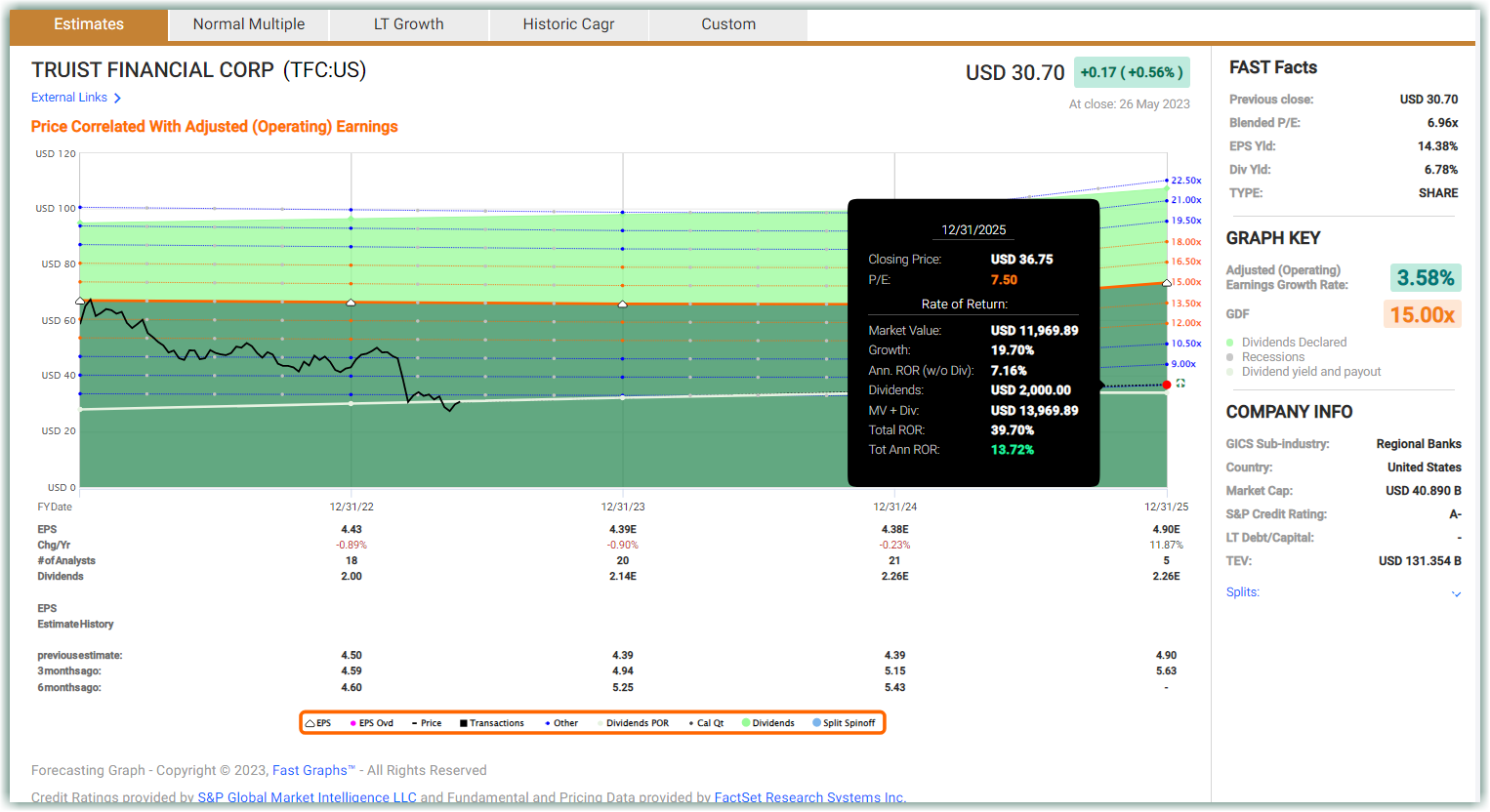

One: Other than the decline in adjusted operating earnings in 2020 due to the pandemic, earnings have been increasing from $3.76 per share in 2019 to $4.47 in 2021. Due to the rapidly rising interest rate environment in 2022 and 2023 and slower economic activity and loan issuance in areas such as mortgage and automobile loans, coupled with greater provision for loan default to be set aside, accounted for the slightly lower $4.43/share in earnings in 2022. Adjusted earnings are expected to stabilize around this range in 2023 and 2024. This is not a bad situation as Truist shows resiliency in the face of macro-challenges and cyclicality in business cycles.

Two: Truist normally traded around a blended P/E of 13.67 within this timeframe yet it is trading at just a blended P/E of 6.96 now. That means even a slight P/E expansion say from 6.96 to 7.50 can potentially return 13.72% in total annualized return.

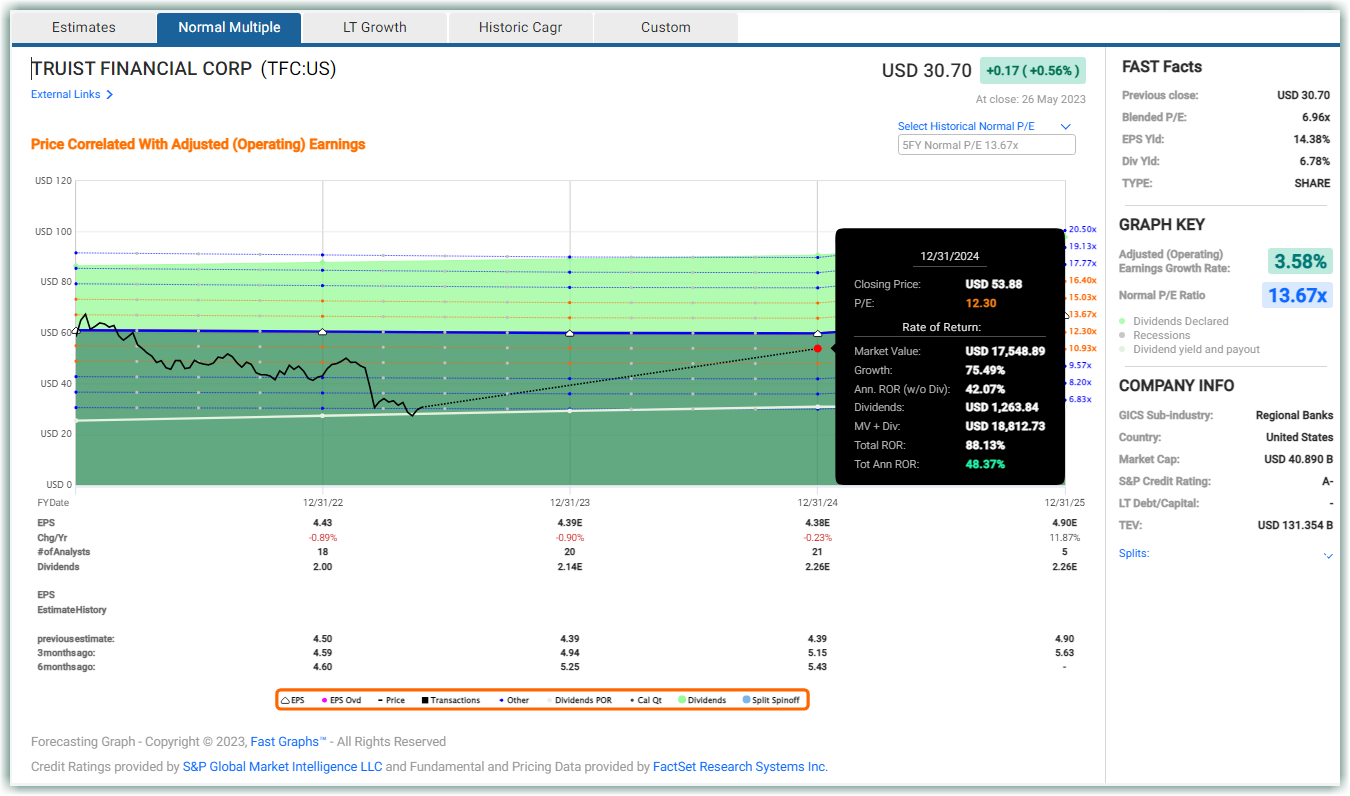

A reversion closer to its normal P/E will mean a much higher potential annualized rate of return of 48.37%.

If Truist can be purchased at a price low enough to provide that margin of safety, it does not have to grow earnings rapidly to provide outsize returns.

That is when it comes to what makes a good investment, Howard Marks insisted it boils down to one thing,

It’s not what you buy, it’s what you pay for It determines whether something is a good investment.

Three: Truist is an A- credit-rated company that pays a healthy 6.78% dividend yield at a comfortable dividend payout ratio of under 50%. This is a company that allows investors to get paid while waiting for capital appreciation.

Is TFC Safe?

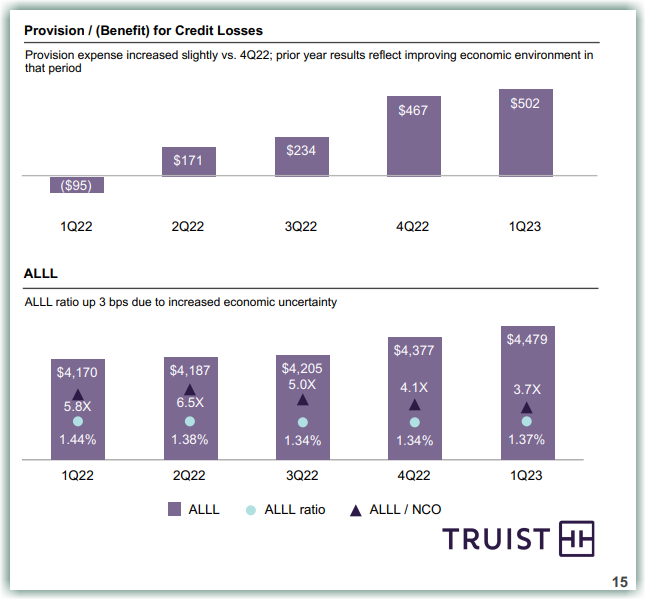

We are living in a tough macroeconomic environment and Truist’s increased provisions for credit losses and ALLL (Allowance for loan and lease losses) are clear reflections of that reality.

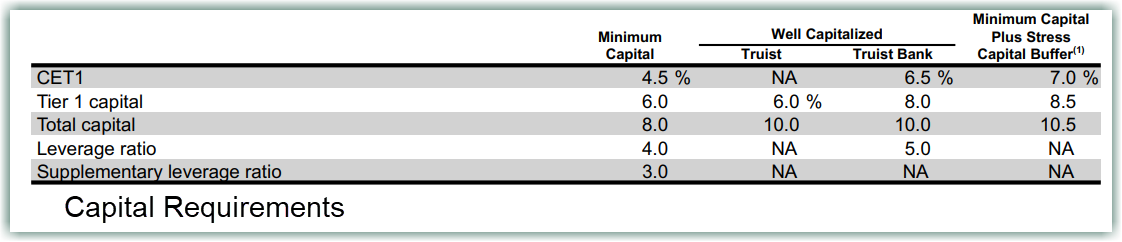

The Federal Reserve’s capital framework for banks with $100 billion or greater in total consolidated assets is partly determined by the supervisory stress test results. The table below shows the total common equity tier 1 (CET1) capital requirement for Truist, which is made up of several components, including

a minimum CET1 capital requirement of 4.5 percent, which is the same for each bank;

the stress capital buffer (SCB) requirement, which is determined from the supervisory stress test results and is at least 2.5 percent

According to Truist’s Q1 2023 10Q,

Truist regularly performs stress testing on its capital levels and is required to periodically submit the Company’s capital plans and stress testing results to the banking regulators. Management regularly monitors the capital position of Truist on both a consolidated and bank-level basis. In this regard, management’s objective is to maintain capital at levels that are in excess of internal capital limits, which are above the regulatory “well capitalized” minimums.

Capital ratios remained strong compared to the regulatory requirements for well-capitalized banks.

Risk and Uncertainty

Eric Compton with Argus Research presented the following discussion of the risk and uncertainty he sees with TFC:

“Truist has been an active acquirer of other banking institutions over the years. Thus, Truist faces the risk that its deals could eventually destroy shareholder value via overpaying or poor integration. We don’t view this as a large risk, as Truist has generally been a smart acquirer and many of the recent bolt-on acquisitions were relatively smaller in scale. We view the macroeconomic backdrop as the other primary risk to the bank. Truist’s future profitability will largely be determined by the interest-rate cycle as well as the effects of credit and debt cycles, all of which are not under management’s control.”

Although we agree that these risks and uncertainties are realistic worries, we further believe that those risks are already built into the incredibly low valuation and price. In other words, we believe current and prospective shareholders would be well compensated by adding to their holdings or outright purchases at these levels.

Conclusion

We believe that Truist is a well-capitalized bank that is safe, profitable, and well-priced. Even though there are arguably a few higher-quality banks, it is very hard to argue with the advantage based on the long-term opportunity that TFC offers. TFC’s high current yield and potential dividend growth provide the double-barrelled benefit of current income and long-term capital appreciation.

However, with the above said, prospective investors should recognize that the real opportunity here is based on the company’s valuation. TFC, along with many other regional banks, fell in sympathy with the banking crisis brought on by SIVB and other weaker and less capitalized competitors. As a result, we see the current valuation of TFC as overdone and therefore is an excellent long-term opportunity. Given today’s valuations, it is only necessary that fundamentals, specifically earnings, do not deteriorate. In other words, as long as the company maintains current levels, even if it does not grow, we believe the long-term opportunity of investing in TFC is extraordinary.

Disclosure: Long C, TFC, JPM

Disclaimer: The opinions in this document are for informational and educational purposes only and should not be construed as a recommendation to buy or sell the stocks mentioned or to solicit transactions or clients. Past performance of the companies discussed may not continue and the companies may not achieve the earnings growth as predicted. The information in this document is believed to be accurate, but under no circumstances should a person act upon the information contained within. We do not recommend that anyone act upon any investment information without first consulting an investment advisor as to the suitability of such investments for his specific situation.

A message from Advisor Perspectives and VettaFi: To learn more about this or other topics, please check out our most recent white papers.