The worst may be over for residential investment.

The global financial crisis cast a lingering shadow over residential investment. Since 2020, the rapid runup and subsequent flattening of house prices raised worries of another cycle of housing stress. But those concerns may be overdone. More construction is needed.

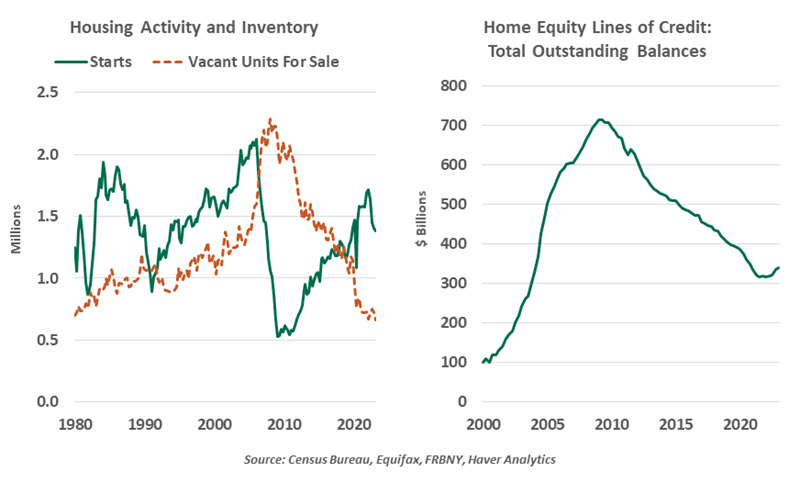

The pandemic surge in home demand demonstrated that the U.S. has an undersupply of housing. Today, the inventory of homes for sale is depleted, standing at a level last seen in 1980, despite a population that has grown 47% over the same interval. Construction has room to grow without repeating the excesses of the housing bubble. Through the pre-COVID cycle, housing starts barely returned to the levels of the 1990s.

The median homeowner stayed put in the pandemic era, refinancing into very low mortgage rates. Some have lucked into a carry trade, paying an interest rate on their seasoned mortgage that is lower than the income offered by safe assets like money market funds. The higher interest rate on new mortgages renders those homeowners less likely to move. By staying put, they constrain inventories (supporting house prices), and they become customers for home renovation projects.

At the start of 2023, home equity lines of credit (HELOCs) reversed their 12-year decline. In the housing bubble, lines of credit secured by homes were an easy way to realize a gain from rising home values. Through the prior cycle, with low rates, many homeowners preferred cash-out refinancing to HELOCs. Now, with unfavorable mortgage rates and high home values, homeowners are borrowing against their equity. Maintaining their locked-in low mortgage adds to incentives to modify their existing homes rather than move. Even if new home construction falls flat, builders can find work in renovations, and residential investment can grow again.

Today’s tight housing market stems from years of underinvestment.

After a difficult 2022, builders are now reporting more buyer interest and are starting new developments. The short down-and-up turn of housing may set a pattern for the current economic cycle. Last year’s laggards, like construction and technology, are getting back on track this year. Stress will roll through other sectors in due course. With patience and perseverance, sector shocks can be contained and not spill over to a broader downturn.

Information is not intended to be and should not be construed as an offer, solicitation, or recommendation with respect to any transaction and should not be treated as legal advice, investment advice, or tax advice. Under no circumstances should you rely upon this information as a substitute for obtaining specific legal or tax advice from your own professional legal or tax advisors. Information is subject to change based on market or other conditions and is not intended to influence your investment decisions.

© 2023 Northern Trust Corporation. Head Office: 50 South La Salle Street, Chicago, Illinois 60603 U.S.A. Incorporated with limited liability in the U.S. Products and services provided by subsidiaries of Northern Trust Corporation may vary in different markets and are offered in accordance with local regulations. For legal and regulatory information about individual market offices, visit northerntrust.com/terms-and-conditions.

A message from Advisor Perspectives and Vetta Fi: To learn more on this and other topics, check out our full schedule of upcoming CE-approved virtual events.

© Northern Trust

Read more commentaries by Northern Trust