Cash Can Be a Drag When Rate Hikes End

Membership required

Membership is now required to use this feature. To learn more:

View Membership BenefitsKey takeaways

- Waiting too long to shift cash into bonds can be costly.

- Bonds can be better diversifiers of equity risk post-rate hikes.

- Quality stocks have been resilient through volatility and still captured the upside.

What’s next for rates and the economy?

The Fed may be toward the end of this rate-hiking cycle but the dust is not settled. Current market pricing implies that the Fed will begin lowering rates as early as this summer, yet there are reasons to believe the Fed is more likely to hold rates steady until either inflation comes down meaningfully or the economy spirals toward a hard landing and deep recession.

How well the economy endures the current level of interest rates is a considerable variable. We’ve already seen signs of stress in the financial system manifested in the failure of a few small regional banks, and corporate earnings have thus far been a mixed bag. Whether you’re an individual buying a house or a business in need of equipment, high-interest rates make borrowing more costly, which has the effect of slowing economic growth. However, the labor market remains strong and Q1 earnings thus far have not been as bad as analysts had forecasted.

Cash can be comfortable but costly

Uncertainty around the economy and interest rates can make it tempting to sit out of the markets for a while. And thanks to the Fed’s rate hiking, investors have been earning decent returns in short-term cash instruments such as money market funds or certificates of deposit (CDs) yielding 4% or more with little risk.

Indeed, cash can be comfortable, but these high short-term yields won’t last forever. Long-term investors will eventually need to shift into bonds to meet their return objectives. Making that move too late can be costly and markets can be really hard to time. Making the move now helps investors mitigate reinvestment risk and the opportunity cost that comes with staying in cash too long.

For example, consider a one-year CD paying 4%. If interest rates fall 100 basis points (1%) over the year (as the market expects), the CD can be reinvested at only 3% at maturity. That’s your reinvestment risk.

Now consider the opportunity cost. While the CD earned 4%, a bond yielding 3% may have earned more amid falling rates given the price appreciation resulting from its longer duration. (Bond prices rise when rates fall.) The Bloomberg U.S. Aggregate Bond Index, with an average duration of 6.5 years and yield of 4.2%, would have earned 10.7% (4.2% yield + 6.5 duration * 1% decline in rates). The opportunity cost of holding the CD would be 6.7% (10.7% - 4.0%).

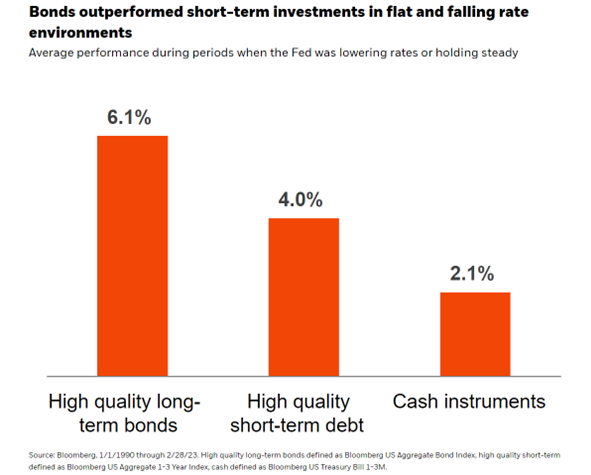

High-quality long-term bonds have historically outperformed high-quality short-term debt and cash instruments during periods when the Fed was lowering rates or holding them steady.

Bonds can be better diversifiers when the Fed isn’t raising interest rates.

History shows us that during periods when the Fed was hiking interest rates, the performance of stocks and bonds has been positively correlated. Last year, concerns about the impact of the Fed’s rate hikes drove stock prices down at the same time that the rate hikes themselves drove bond prices down. Bonds were not effective diversifiers in 2022.

In periods when the Fed has lowered rates or kept rates on hold, the correlation between stock and bond performance has been negative. Given their duration, bond prices rise when interest rates go down. The Fed has typically lowered rates in reaction to economic stress, so stocks are typically falling in such an environment. When interest rates are flat, bond prices shouldn’t change, but their coupon payments should make their total returns positive.

Whether the Fed hits pause and keeps rates high or starts lowering rates, it is highly likely that bonds will regain their equity diversification properties until the next rate hiking cycle.

If you are concerned about a recession driving stock prices down, it’s even more valuable to invest in an asset that is negatively correlated – or is expected to rise in that scenario. We have historically seen a “flight to quality” in times of market stress, where investors seeking safety have piled into Treasury bonds, driving up their value. In this particular time, the greater the recession, the more likely the Fed will be stepping in and lower rates, which could provide an even bigger boost to longer-duration, high-quality bonds.

Stay in stocks, but opt for quality.

You may be concerned about an upcoming recession, but it’s still important to stay invested for your longer-term goals. Markets are notoriously difficult to time, and many of the best market days follow the worst market days. Selling at the wrong time is even more expensive than sitting in cash.

In times like these, we prefer higher-quality stocks – profitable companies with low debt and consistent earnings, stable and predictable cash flows, and the ability to grow their dividends. Companies like these have historically been more resilient through market volatility and still captured some upside when markets recovered.

What goes up must come down

Whether it happens this summer or next year, eventually the Fed will conclude this rate hiking cycle, and cash yields will come down. Investors who remain in cash will miss the price appreciation in high-quality longer-duration bonds that can be expected when rates fall. As they regain their ability to diversify equity risk, bonds can be especially helpful if a recession negatively impacts stock prices. You can also seek to reduce equity risk by shifting toward higher-quality stocks.

BlackRock can help you manage risk in today’s markets. Contact your BlackRock representative or explore our online investment tools and resources.

Carolyn Barnette, CFA, CFP, Director, is Head of Market and Portfolio Insights for BlackRock’s U.S. Wealth Advisory business.

Membership required

Membership is now required to use this feature. To learn more:

View Membership BenefitsSponsored Content

Upcoming Virtual Events View All