A Portion of U.S. Consumers Seem Stressed Out, So Is This What Everyone is Looking for as the Canary in the Coal Mine?

A Closer Look at Auto ABS & Investment Opportunities

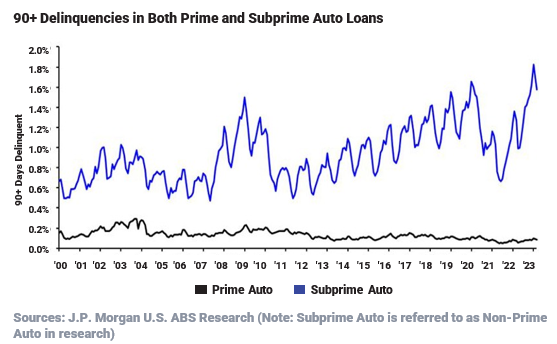

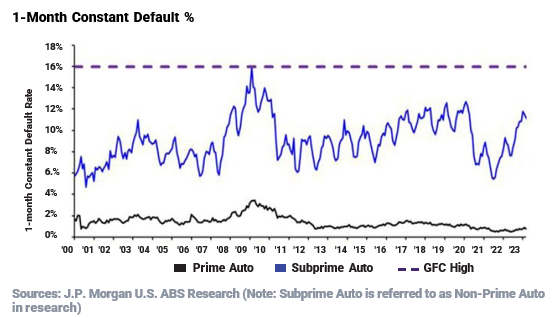

Subprime Auto Loan Borrowers Are Acting More Stressed Than They Did During the Great Financial Crisis

Despite the resilient employment numbers in the U.S. economy, it’s difficult to ignore the fundamentals of certain asset types we con- stantly monitor, most specifically subprime auto loans. Looking back at historical auto loan delinquencies since 2000, in the chart below, prime auto loans performed relatively well during the Great Finan- cial Crisis (“GFC”), whereas subprime auto loans spiked from ~0.5% in the first half of 2007 to ~1.5% by the beginning of 2009. The sub- prime auto loan delinquency rate recovered back down to a post-GFC low of ~0.5% in the middle of 2011, but then gradually creeped higher towards ~1.6% by the beginning of 2020 (pre-COVID). COVID-19 re- lated stimulus payments, from the U.S. Government, assisted in drop- ping the delinquency rate back down to ~0.7% in the middle of 2021. However, now that the subprime borrowers are facing a tremendous amount of headwinds from higher cost of living, higher interest rates, and no further stimulus payments from the U.S. Government, their delinquency rates in the first quarter of 2023 have been experiencing new highs (with a peak since of ~1.8% as of the end of February 2023) since the beginning of 2000.

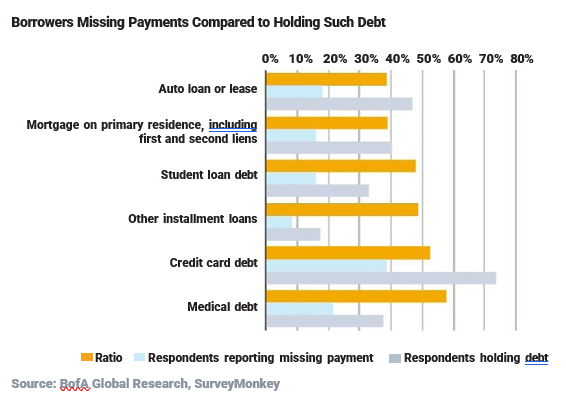

What’s interesting about their poor performance is that U.S. borrow-ers have repeatedly demonstrated that they are more likely to skip pay-ments on medical debt and credit card debt versus missing payments on their auto loan/lease or primary residence. The chart below shows that auto loans/leases have the lowest ratio of missing payments over the six months prior to January 2023 compared to the percent of respondents holding each type of debt at such time. This helps explain why prime auto delinquencies continue to hold up well.

Auto Loans Have Larger Balances and Longer Terms

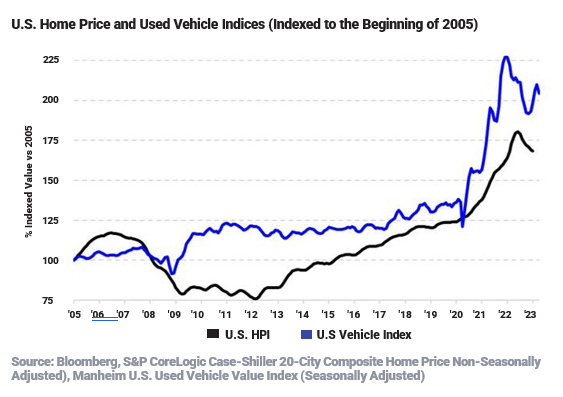

As we look at the various factors that are potentially causing such weakness in the subprime auto Asset-Backed Securities (“ABS”) sector versus other sectors, it’s important to note how much the nominal val- ue of used vehicles have increased over the past 20+ years. Although many other goods often become more economical over time (such as flat-screen televisions and mobile phones), used vehicle values have grown at a very rapid rate since the GFC. However, used vehicle values exploded at an unsustainable growth rate resulting from the COVID-19 related stimulus payments and supply chain issues causing insatiable demand coupled with unprecedented inflationary conditions.

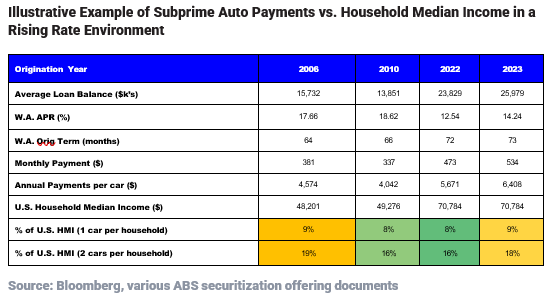

The rapid growth rate of used vehicle values was countered by auto orig- inators offering longer terms to suppress the average monthly payment of an auto loan. As shown in the illustrative example below, average sub- prime loan balances continued to increase and ended up approximately doubling between 2010 and 2023 although U.S. Household Median In- comes (“U.S. HMI”) have not (U.S. HMI has increased by approximately 40% from 2010 to 2023).

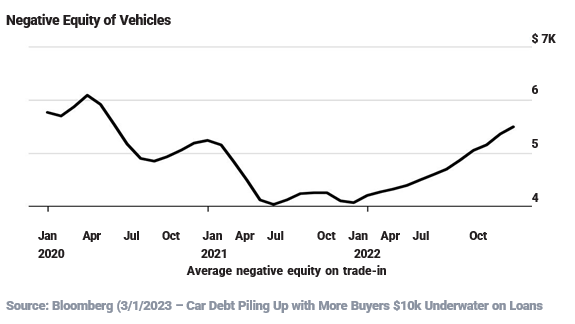

Negative Equity, Declining Vehicle Values and Rising Rates Are Stressing Borrowers

Granting longer maturities to subprime auto borrowers resulted in the creation of more negative equity during the term of their ownership of their vehicle. Furthermore, the earlier these borrowers trade-in their previous vehicles, the more underwater they will be in their succeeding auto loan causing a downward spiral of larger negative equity.

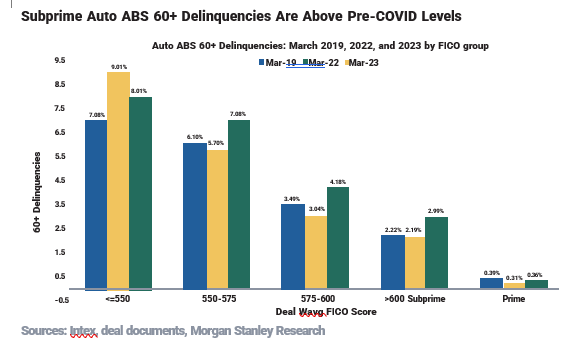

As inflation continues to increase the cost of living for all U.S. Consum- ers, it is very apparent to us that it is negatively affecting subprime bor- rowers (who tend to have lower credit scores and lower incomes) more harshly than others. As you can see in the chart below, the credit scores (“FICOs”) under 600 have risen much more dramatically than those with credit scores above 600.

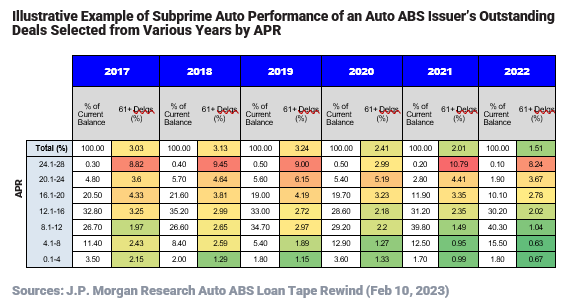

Conversely, the lower the credit score a borrower has generally results in a higher Annual Percentage Rate (“APR”). As can be seen from the illustrative example below, the higher the auto loan APRs are in a port- folio, the higher the probability that such cohort of borrowers are at least 60 days delinquent. As the U.S. Federal Reserve Bank continues to hold rates higher for longer to combat inflation, we foresee this weakening performance in subprime auto continuing to deteriorate.

Losses Are Looming

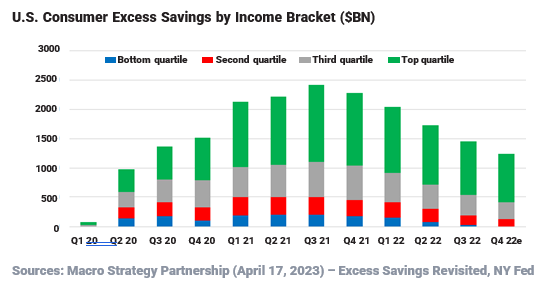

As the level of excess savings continues to drop from its peak in the mid- dle of 2021, we anticipate a greater percentage of U.S. Consumers will run out of excess savings leaving them more susceptible (i.e. life event such as a major medical expense or job loss) to miss payments and be- come delinquent on their outstanding loans. Illustratively, you can see from the chart below, the bottom quartile has already drained their share of the total excess savings. The second-most bottom quartile should be the next to completely drain their excess savings soon, and so on up the quartiles.

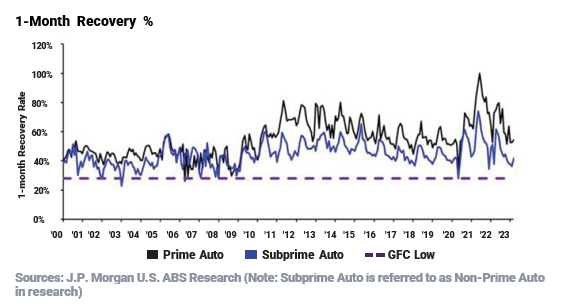

All else being equal and continuing the current path, we are assuming defaults and recoveries will continue to deteriorate more towards levels not seen since the GFC. While some issuers and investors continue to invest at today’s fun-damental levels, we intend to “skate towards where the puck is headed” and assume potential losses akin to the GFC for not only subprime loans, but for prime loans as well, as we anticipate more potential hardships ahead for the U.S. Consumer.

By taking all the risks and rewards into account and focusing on loss-ad- justed total returns, we expect the following in regards to Auto ABS in 2023:

1) We will remain somewhat defensive and focus on investments that are secured by underlying assets with stronger borrowers such as prime auto and stay higher up in the capital structure and shorter in duration. It is unlikely lower mezzanine/subordinate bonds as well as bonds backed by collateral originated to lower credit quality borrowers will result in risk-adjusted total returns that are compelling as investments. Examples of potential near term investments being 1-2 year duration seniors and heavily cashflowing bonds secured by auto loans and leases returning mid-to-high single digit types of returns.

2) After the fundamentals flow through and “bottom out” (i.e. unem- ployment increases to the top of the cycle), defaults and recoveries should reach more distressed levels potentially leading to sellers of distressed assets at very attractive valuations. We will look to make opportunistic investments in both senior and subordinate credits and/or lower credit borrowers in subprime auto, credit cards, residential, etc., that offer good risk-adjusted total returns that show promise of high single to mid-teens types of returns.

We believe that all-in-all the backdrop of a weakening economy and a hawkish U.S. Federal Reserve Bank (albeit in the later stages) will be a good foundation for most fixed income, especially in select Structured Products such as Auto ABS, and will help highlight that good asset se- lection resulting from a repeatable process with a long track record will allow Bramshill Investments to outperform our peers.

Disclosure:

Bramshill Investments, LLC (“Bramshill”) is an asset management firm and investment adviser registered with the U.S. Securities and Exchange Commission (“SEC”). Registration with the SEC does not imply any skillset of Bramshill or its employees. All statements and opinions are subject to change as economic and market conditions dictate. Investing involves risk, including the potential loss of principal, and the profitability of any particular investment strategy or product cannot be guaranteed. Our view and opinions are accurate as of the date of this letter and are provided for informational purposes only and are for the sole use of the intended audience/recipients, all of which are or represent current or potential investors in one or more investment vehicles or mutual fund (each a “fund” and collectively the “funds”) managed by Bramshill. The data and information presented herein has not been audited (except as otherwise expressly indicated) and is subject to subsequent adjustment. Bramshill has no obligation, express or implied, to update any of the information or to advise you of any changes. Similarly, Bramshill does not make any express or implied warranties or representations as to the completeness or accuracy, or accept responsibility for inaccuracies, errors or omissions. Past performance is not necessarily indicative of future results. No representation is being made that any fund or portfolio managed by Bramshill will or is likely to achieve profits or losses similar to those shown. The reader should not assume this is investment advice or an offer to solicit into one of our investment strategies. Further information regarding the funds and investment strategies are available upon request. For more information, please refer to www.bramshillinvestments.com

Read more commentaries by Bramshill Investments