Municipal Closed-End Funds: Near Term Pain, Long-Term Gain?

Membership required

Membership is now required to use this feature. To learn more:

View Membership BenefitsKey takeaways

- Municipal closed-end funds (“CEFs”) primarily invest in investment grade municipal bonds with longer maturities to maximize tax-exempt income.

- Duration has had a negative impact on municipal CEF returns for the past 18 months and a flatter yield curve has caused leveraged funds to reduce distributions1

- Municipal CEF discounts typically widen in periods of market stress, but we believe this time may be different as credit remains on strong footing.

- Municipal CEFs are now trading at some of their widest discount levels over the past 20 years.

Mixed feelings

Over the past year, the municipal bond market has seen increased volatility stemming from rising interest rates across the yield curve. This volatility has been magnified for Municipal CEFs which primarily invest in long duration bonds and use leverage to maximize tax-exempt income. Following challenged performance in 2022 (down -24.4% on market price), municipal CEFs started the year strong, up 5.9% in January 2023, demonstrating how performance rebounded as interest rates fell and investor demand returned. We then saw a reversal in February 2023 given renewed investor fears of future rate hikes by the Fed. The volatility to start the year has been pronounced, and through March 2023 municipal CEFs are up 2.8% on market price for the year.1

To compound matters, the rapid increase in short-term rates, driven by one of the most aggressive Federal Reserve (“Fed”) tightening cycles on record, has resulted in a flatter yield curve and reduced the benefits of leverage, leading to lower fund earnings. This sparked distribution reductions across leveraged municipal CEFs and reduced investor demand for municipal CEFs. As a result, municipal CEFs saw increased selling pressure on the secondary market, causing the funds to move from a -1.5% discount at the start of 2022 to a -10.9% discount as of the end of March. For context on this change in premium/discount levels, municipal CEF valuations have been narrower 96% of the time over the last 20 years.2

While municipal CEFs are trading at discounts levels similar to those of other periods of market stress such as the 2008 global financial crisis, we believe underlying municipal bond credit fundamentals remain strong. We believe long-term investors seeking attractive tax-exempt income may want to consider municipal CEFs given their historically wide discounts.2

All eyes on distributions

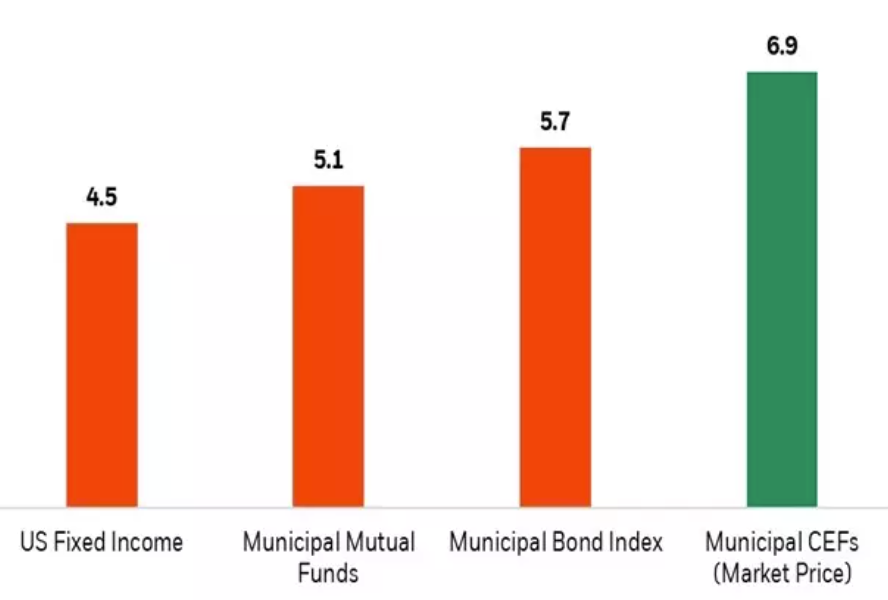

When evaluating municipal bonds, it is important to consider their tax equivalent yield3. Municipal bonds are exempt from federal taxes and investors can potentially receive additional tax benefits by purchasing state and local tax-exempt bonds issued by states and municipalities in which they reside. Municipal CEFs, which typically invest in longer maturity investment grade bonds, are currently offering a median tax equivalent distribution rate of 6.9%, which is higher than the current distribution rate of individual municipal bonds (Exhibit 1). This is after many leveraged municipal CEFs have had to cut their distributions over the past year4.

Exhibit 1: Municipal CEFs can offer investors higher distributions

Tax equivalent rates for Munis

Source: S&P, Morningstar as of 3/31/2023. US fixed income is represented by S&P U.S. Aggregate Bond Index (yield to worst), Municipal Bond index is represented by the S&P Municipal Bond Index (yield to worst), Municipal mutual funds are represented by the median 12-month yield of the US CE Muni National Long category, Municipal CEFs are represented by the Morningstar US CE Muni Long category. Tax Equivalent yield is using a 40.3% tax rate. Past performance is not indicative of future results. You cannot invest directly in an unmanaged index.. For more information on BlackRock closed-end funds’ performance please see please see the following link: BlackRock Closed-End Fund Performance. Index and Morningstar category performance are shown for illustrative purposes only and are not meant to represent the past or future performance for any BlackRock fund.

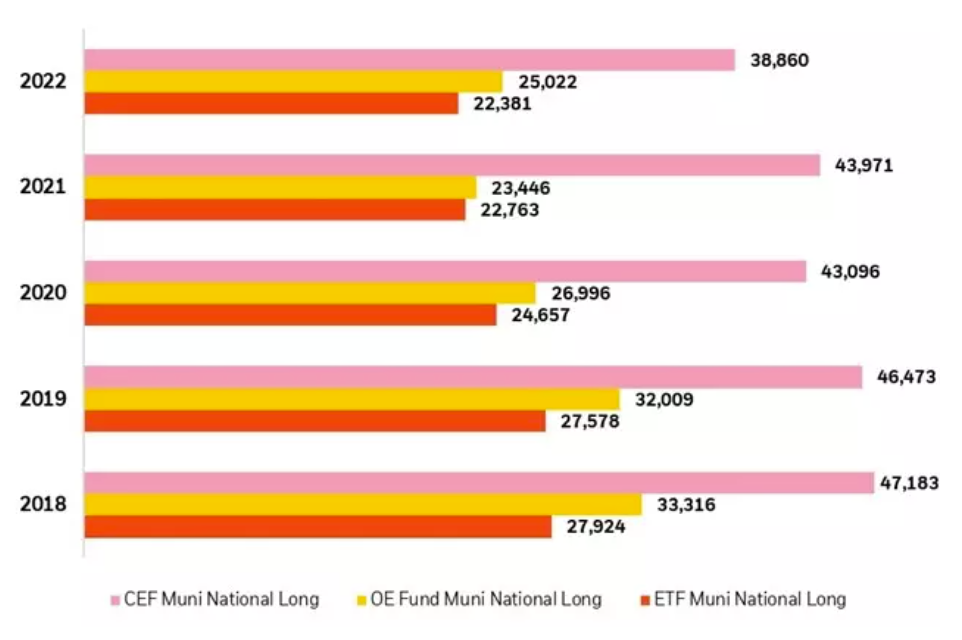

Municipal CEFs can deploy leverage by borrowing money at short-term interest rates, taking those proceeds, and investing in municipal bonds with longer maturities (and theoretically higher yields). In the current environment, a flatter yield curve (i.e., narrower spread) has negatively impacted the earnings of leveraged municipal CEFs. Over the long-term, leverage has helped Muni CEFs pay higher distributions then other products (Exhibit 2).

Exhibit 2: Municipal CEFs may offer investors higher distributions

2018-2022 annual distributions of a hypothetical $1 million investment made every January 1st

Source: Morningstar as of 12/31/2022. Categories are represented by the Morningstar category of the same name. Distributions are based the average yearly income return for each category. Past performance is not indicative of future results. You cannot invest directly in an unmanaged index. Morningstar category performance are shown for illustrative purposes only and are not meant to represent the past or future performance for any BlackRock fund.

Health check on municipal CEF distributions

Over the past year, leverage costs have increased sharply as the Fed has rapidly raised short-term interest rates by 5%. The SIFMA Municipal Swap Index, a common base rate used to calculate municipal CEF leverage costs, currently sits a 3.97%, which is 295 basis points higher than the 5-year average rate of 1.02%5. This increase has led to distribution reductions across the industry as fund earnings have declined. While the municipal yield curve rarely inverts and is not nearly as flat as the Treasury curve, this is a dynamic that investors should be aware of going forward. On a positive note, given their structural benefits (no inflows or outflows), municipal CEFs may be able to “lock in” the higher yields we are seeing today, which could provide distribution stability going forward. We believe investors should regularly monitor municipal CEF distribution coverage ratios on a fund-by-fund basis. Many CEF issuers publish this data, including BlackRock, which publishes the data every month. This allows investors to see if the fund’s distribution is being “earned” in addition to the average cost of leverage for each fund.

Discounts: A long-term opportunity?

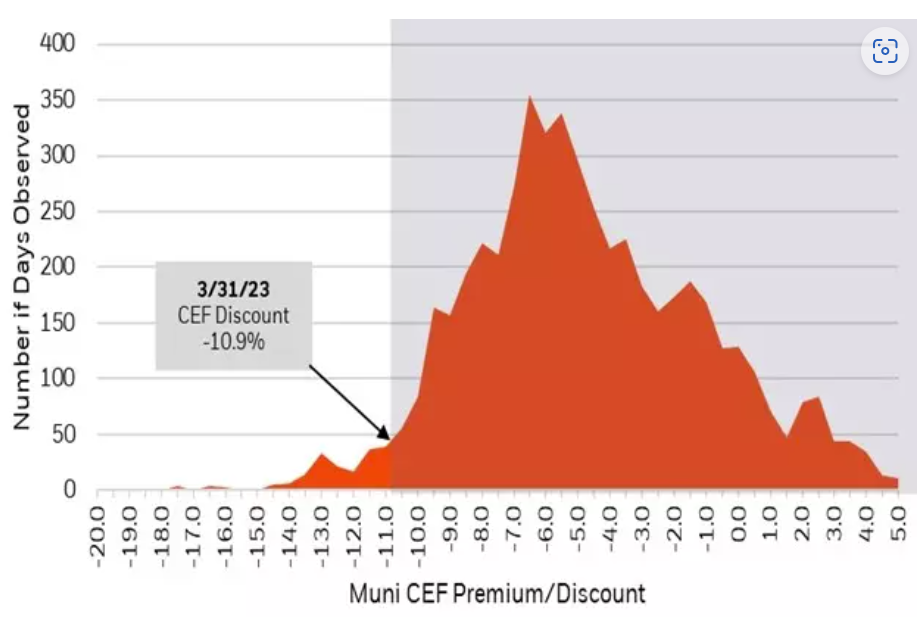

Municipal CEF premiums/discounts have widened substantially over the last year given negative market sentiment as investors assess the impact of rising interest rates on municipal CEF performance and distributions. Municipal CEF premiums/discounts have widened by 480 basis points over the past year and 1,180 basis points from their 10-year high (narrowest) in 2021, and now trade at a median discount of -10.9% discount6. As mentioned earlier, municipal CEF valuations have been narrower 96% of the time over the last 20 years (exhibit 3).

Exhibit 3: Room to run? Municipal CEF have traded at wider discounts only 4% of the time over the past 20 years

Daily premium/discount observations for municipal CEFs over the last 20 years

Source: Morningstar as of 3/31/2023. Daily premium/discount observations for municipal CEFs over the last 20 years for the median of the Morningstar US CE Muni Long Category. Past performance is not indicative of future results. Morningstar category performance are shown for illustrative purposes only and are not meant to represent the past or future performance for any BlackRock fund.

We’ve seen this before

Investors buying municipal CEFs at abnormally large discounts caused by market stress may see strong relative returns during market rebounds (falling interest rates). As demand returns, discounts may narrow and may boost market price performance.

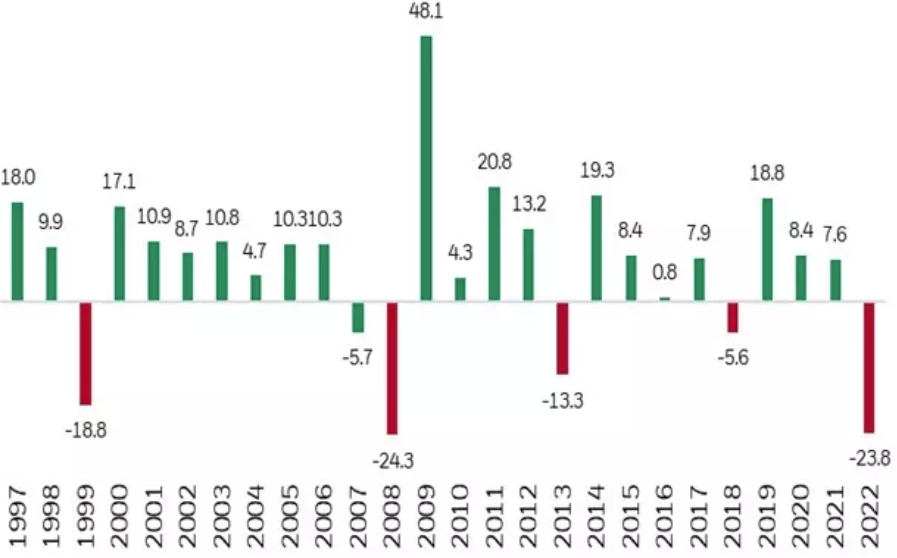

This dynamic has played out for municipal CEFs after sustained periods of negative performance. With history as a guide, we can see that Municipal CEFs tend to recover in the year following negative performance – in fact, the calendar year following a sell-off has produced a 16% return7 on market price as investors took advantage of larger discounts and depressed asset prices (Exhibit 4).

Exhibit 4: The power of narrowing discounts

Muni CEFs market price returns (1997 – 2022) – 25 years

Source: Morningstar as of 12/31/22. Represents Median market price return of the Morningstar US CE Muni National Long Category. Past performance is not indicative of future results. Morningstar category performance are shown for illustrative purposes only and are not meant to represent the past or future performance for any BlackRock fund.

1 Source: Morningstar as of 3/31/23. Muni CEFs are represented by the Morningstar US CE Muni National Long category. Performance is based on market price. Returns and Premium/Discounts are based on category median. Morningstar US CE Muni National Long category was down -4.6% on market price in February 2023 and down -20.9% on market price over the past 18 months. Past performance is not indicative of future results.

2Source: Morningstar as of 12/31/22. Based on daily premium/discount data over the past 20 years. More details in Exhibit 3. Past performance is not indicative of future results. Morningstar category returns are shown for illustrative purposes only and are not meant to represent the past or future performance for any BlackRock fund.

3Tax equivalent yield (“TEY”) is used by investors to compare yields on taxable and tax-exempt securities after accounting for taxes. TEY represents the yield a taxable bond would have to earn in order to match, after taxes, the yield available on a tax-exempt municipal bond.

4Source: Morningstar as of 3/31/23.

5Source: SIFMA as of 3/29/23. The SIFMA Municipal Swap Index is a 7-day high-grade market index comprised of tax-exempt Variable Rate Demand Obligations (VRDOs) with certain characteristics. The Index is calculated and published by Bloomberg. The Index is overseen by SIFMA’s Municipal Swap Index Committee.

6Source: Morningstar as of 3/31/23. Muni CEFs are represented by the US CE Muni National Long category. Past performance is not indicative of future results. Morningstar category performance are shown for illustrative purposes only and are not meant to represent the past or future performance for any BlackRock fund.

7Source: Bloomberg, Lipper as of 12/31/22. Muni CEFs are represented by the Lipper General & Insured Municipal (Leveraged) category. Past performance is not indicative of future results. Morningstar category performance are shown for illustrative purposes only and are not meant to represent the past or future performance for any BlackRock fund.

Carefully consider each Fund’s investment objective, risk factors, and charges and expenses before investing. This and other information can be found in each Fund’s prospectus, if applicable, or shareholder report which may be obtained by visiting the SEC Edgar database. Read the prospectus, if applicable, or shareholder report carefully before investing.

This material is for informational purposes only and is not intended to be relied upon as research or investment or tax advice, and is not a recommendation, offer or solicitation to purchase or sell any securities or to adopt any investment strategy, nor shall any securities be offered or sold to any person in any jurisdiction in which an offer, solicitation, purchase or sale would be unlawful under the securities laws of such jurisdiction.

There is no assurance that a Fund will achieve its investment objective. Investing in a Fund involves numerous risks, including investment risks and the possible loss of principal amount invested. The Funds are not complete investment programs and you may lose money investing in a Fund. An investment in a Fund may not be appropriate for all investors.

Performance results reflect past performance and are no guarantee of future results. Current performance may be lower or higher than the performance data quoted. All returns assume reinvestment of all dividends and/or distributions at the price of the Fund on the ex-dividend date. The distribution rate, market value and net asset value of a Fund's shares will fluctuate with market conditions. Closed-end funds may trade at a premium to NAV but often trade at a discount.

The amounts and sources of Fund distributions reported in any notices to shareholders are only estimates and are not being provided for tax reporting purposes. The actual amounts and sources of the amounts for tax reporting purposes will depend upon a Fund's investment experience during the remainder of its fiscal year and may be subject to change based on tax regulations. A Fund will send a Form 1099-DIV for the calendar year that will tell shareholders how to report these distributions for federal income tax purposes. Some Funds make distributions of ordinary income and capital gains at calendar year end. Those distributions temporarily cause extraordinarily high yields. There is no assurance that a Fund will repeat that yield in the future. Subsequent monthly distributions that do not include ordinary income or capital gains in the form of dividends will likely be lower.

Some investors may be subject to the alternative minimum tax (AMT).

Index Definitions:

S&P Municipal Bond Index: The S&P Municipal Bond Index is a broad, market value-weighted index that seeks to measure the performance of the U.S. municipal bond market.

S&P U.S. Aggregate Bond Index: The S&P U.S. Aggregate Bond Index is designed to measure the performance of publicly issued U.S. dollar denominated investment-grade debt. The index is part of the S&P AggregateTM Bond Index family and includes U.S. treasuries, quasi-governments, corporates, taxable municipal bonds, foreign agency, supranational, federal agency, and non-U.S. debentures, covered bonds, and residential mortgage pass-throughs.

The opinions expressed are as of April 5, 2023, and may change as subsequent conditions vary.

The Funds are actively managed and their characteristics will vary. Stock and bond values fluctuate in price so the value of your investment can go down depending on market conditions. International investing involves special risks including, but not limited to political risks, currency fluctuations, illiquidity and volatility. These risks may be heightened for investments in emerging markets. Fixed income risks include interest-rate and credit risk. Typically, when interest rates rise, there is a corresponding decline in bond values. Credit risk refers to the possibility that the bond issuer will not be able to make principal and interest payments. Principal of mortgage- or asset-backed securities normally may be prepaid at any time, reducing the yield and market value of those securities. Obligations of U.S. government agencies are supported by varying degrees of credit but generally are not backed by the full faith and credit of the US government. Non-investment-grade debt securities (high-yield/junk bonds) may be subject to greater market fluctuations, risk of default or loss of income and principal than higher rated securities. Investments in emerging markets may be considered speculative and are more likely to experience hyperinflation and currency devaluations, which adversely affect returns. In addition, many emerging securities markets have lower trading volumes and less liquidity. A Fund may use derivatives to hedge its investments or to seek to enhance returns. Derivatives entail risks relating to liquidity, leverage and credit that may reduce returns and increase volatility. Refer to a Fund’s prospectus, if applicable, or shareholder report for more information.

50 Hudson Yards, New York, NY 10001

© 2023 BlackRock, Inc. or its affiliates. All Rights Reserved. BLACKROCK is a trademark of BlackRock, Inc. or its affiliates. All other trademarks are those of their respective owners.

USWAH0423U/S-2829589-5/7

Membership required

Membership is now required to use this feature. To learn more:

View Membership Benefits