The Northern Trust Economics team shares its outlook for U.S. growth, employment, interest rates and inflation.

Just a month ago, we were in the grips of a panicked interval for the financial sector. Would the challenges of Silicon Valley Bank (SVB) spill over to other banks, grow into a systemic shock, and spur the next recession? Today, circumstances are far calmer, but the incident has cast a shadow over the outlook. SVB demonstrated that stress can manifest quickly, and some of its challenges are shared by most financial institutions.

The SVB storm did offer a silver lining: Regulators and industry leaders showed their readiness to act to maintain stability. Selective enhancements of deposit insurance curtailed the bank run, while emergency lending facilities ensured banks stay liquid. It is too soon to say a financial crisis has been avoided, but these measures did restore calm.

Lingering concerns about stability have brought the Fed even closer to the end of its hiking cycle. Current inflation and employment readings support the case for a tight monetary policy posture. Further improvement to inflation will keep the Fed on course to cut rates next year; a resurgence in tensions could pull that date forward.

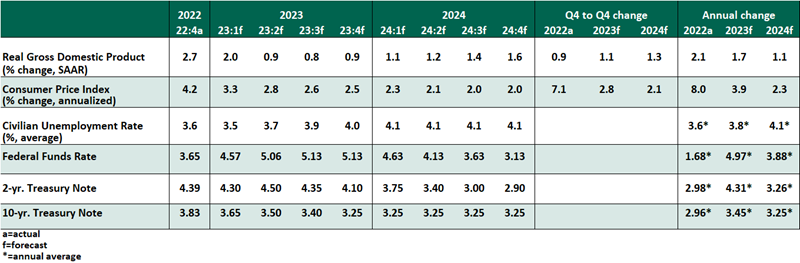

Key Economic Indicators

Influences on the Forecast

- The March consumer price index (CPI) improved to a rate of 5.0% year over year, driven by lower prices of utilities and food at home. Excluding food and energy, core inflation was less encouraging, ticking up slightly to 5.6% over the past twelve months. The price correction in durable goods has run its course, while services inflation remains elevated. The increase in shelter costs has started to slow and will likely contribute to disinflation in months to come. Meanwhile, more moderate food and energy prices will help consumers withstand higher costs in other categories.

- The prolonged labor market recovery continues at a less fervent pace. March saw a gain of 236,000 jobs. While that is the slowest monthly pace of job creation since 2020, it is still supportive of growth. Few workers remain sidelined: the unemployment rate fell to 3.5%, and the employment-population ratio for prime-aged (25-54) workers reached a 20-year high of 80.6%. Average hourly earnings continue to calm, growing 4.2% year over year, a positive omen for inflation.

- Routine annual revisions to the seasonal factors in weekly jobless claims data raised the level of claims. They have shifted from exceedingly small to merely low, now holding in a range last seen in 2018-19. However, continuing unemployment claims are trending upward; those who lose jobs are having a harder time finding work.

- Job openings in February fell below 10 million for the first time since 2021, though they remain elevated relative to their pre-pandemic norm. Rates of hiring and quits are normalizing, suggesting a modest cooling of the overheated labor market.

- With inflation still elevated and labor markets showing little slack, we expect the Fed to issue another 25 basis point rate hike at its May 3 meeting. The preponderance of the evidence suggests that will be the end of the hiking cycle. The Fed’s March Summary of Economic Projections showed a consensus of only a further increase of 25 basis points in 2023, followed by a pause lasting the balance of the year.

- Fallout from recent uncertainty has turned attention to credit conditions, with an expectation that banks will be less willing to extend credit. However, banks are not the only lenders in the economy, and even prior to the crisis, lending standards were tightening and loan demand was falling amid higher rates. Credit extension may fall cyclically.

- Uncertainty has driven a reallocation of cash away from deposits and into money markets. The reminder of insurance limits made large depositors worried about their cash; high yields on safe assets have added to the appeal of money market funds. Overall liquidity is ample, but its shift out of the banking sector raises the risk of further episodes of bank stress.

- The Fed’s short-term funding facilities have seen quick adoption. Combined use of the Fed’s standing discount window funding facility and new Bank Term Funding Program (BTFP) rose to over $168 billion within three weeks of BTFP’s launch. Their fall in the following week adds to hope that the stress is rapidly subsiding.

- While equity markets have calmed, volatility remains elevated in fixed income markets. After a rapid repricing during SVB tensions, the yield on the 2-year U.S. Treasury note has entered a near-daily whipsaw pattern. The MOVE index of bond market volatility is holding at levels seen through most of 2022. While we came into the year expecting a gradual decline in yields, these quick changes are adding to feelings of unease.

Carl R. Tannenbaum

Executive Vice President and Chief Economist

Ryan James Boyle

Vice President, Senior Economist

Vaibhav Tandon

Vice President, Economist

Information is not intended to be and should not be construed as an offer, solicitation or recommendation with respect to any transaction and should not be treated as legal advice, investment advice or tax advice. Under no circumstances should you rely upon this information as a substitute for obtaining specific legal or tax advice from your own professional legal or tax advisors. Information is subject to change based on market or other conditions and is not intended to influence your investment decisions.

© 2023 Northern Trust Corporation. Head Office: 50 South La Salle Street, Chicago, Illinois 60603 U.S.A. Incorporated with limited liability in the U.S. Products and services provided by subsidiaries of Northern Trust Corporation may vary in different markets and are offered in accordance with local regulation. For legal and regulatory information about individual market offices, visit northerntrust.com/terms-and-conditions.

© Northern Trust

Read more commentaries by Northern Trust