Volatility can be challenging but it also creates opportunities. In our view, rotating across sectors within the investment grade market is the most effective way to take advantage of price fluctuations and generate alpha.

The volatility within the investment grade (IG) fixed income universe over the first three months of 2023 has been a blessing for investors like us. Our strategy seeks to capitalize on the behavioral differences between the three major sectors within the investment grade universe – U.S. Treasuries, corporate bonds, and agency mortgage-backed securities (MBS). By rotating across these groups, we attempt to generate alpha and deliver better risk-adjusted returns than the Bloomberg U.S. Aggregate Index (Agg).

One Investment Grade Market, Three Distinct Asset Classes

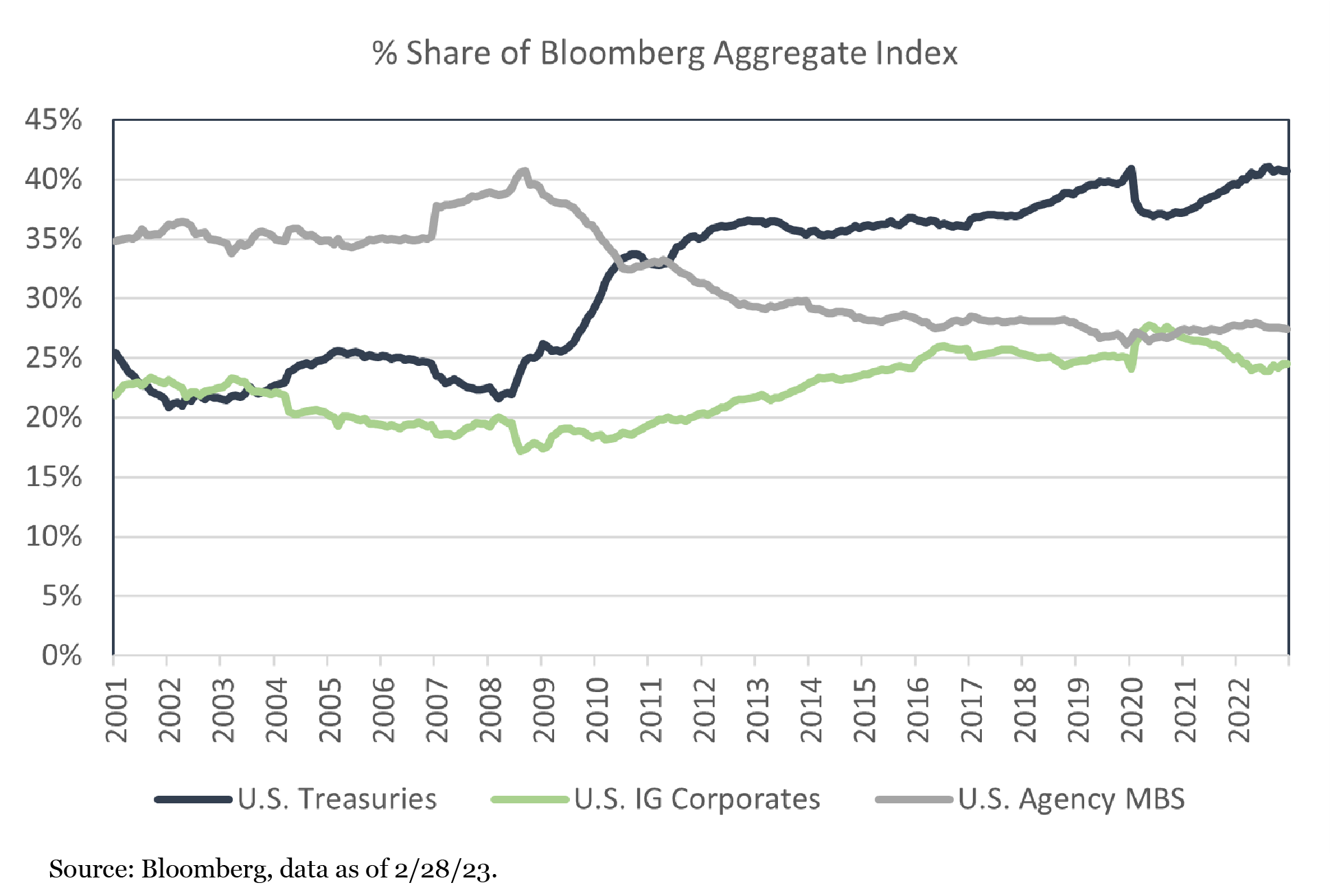

The investment grade bond market is unlike equities or high yield fixed income, as each major sector provides exposure to a unique and differentiated risk/return profile. U.S. Treasuries are considered the ultimate safe haven asset and are typically in high demand during periods of market distress. Performance is driven by moves in interest rates and economic/inflation expectations. The agency MBS sector, more specifically agency pass-throughs, is made up of Treasury-like amortizing bonds that allow investors to express views on homeowner prepayment behaviors driven by the level and volatility of interest rates. And finally, the corporate bond sector allows investors to gain exposure to the credit risk of corporations that use leverage to finance their business activities. Because each sector is sensitive to different economic and market factors, the IG market provides investors with diverse sources of return. At the end of February 2023, these three sectors made up over 93% of the Bloomberg Aggregate Index.

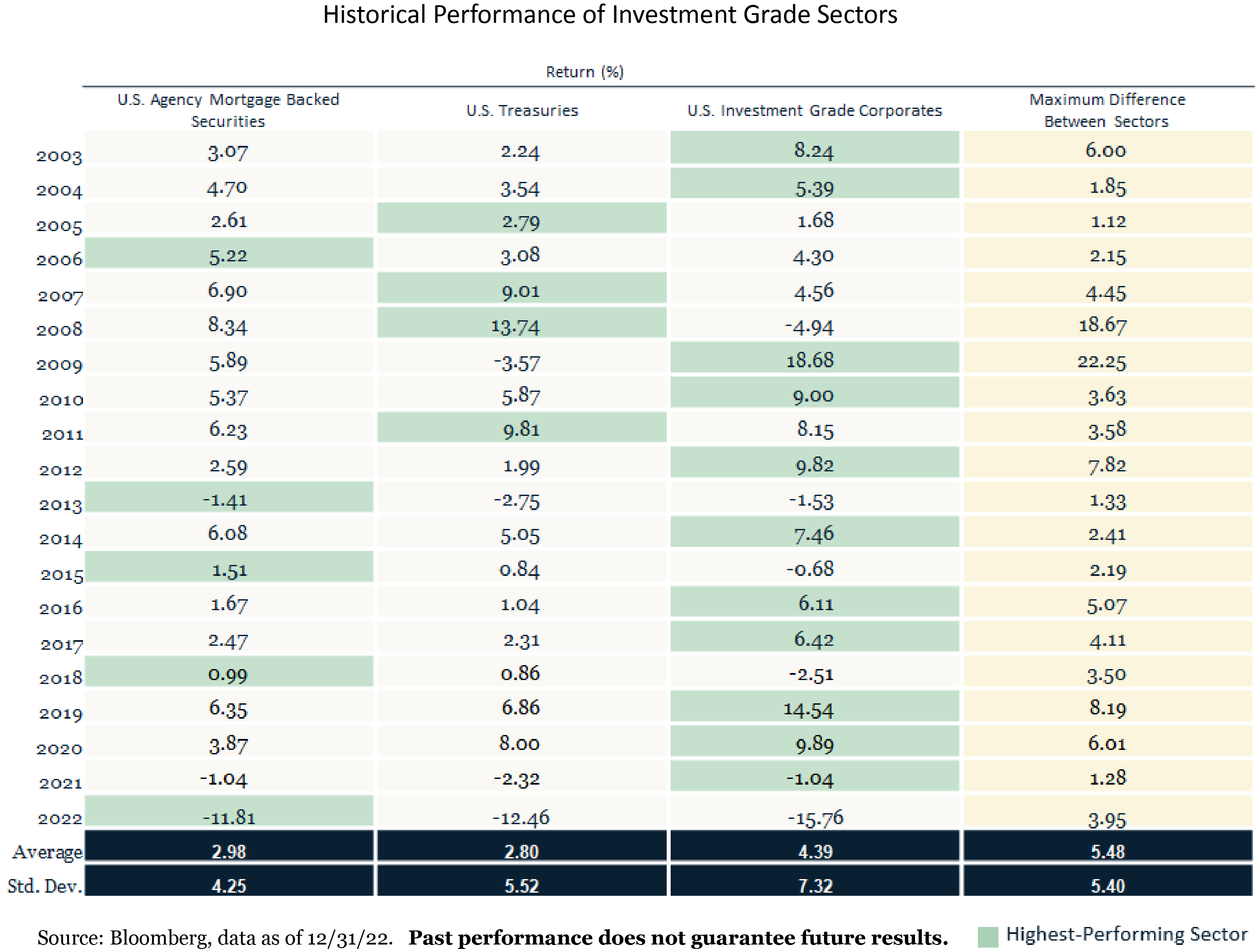

Investors who have not closely followed the investment grade universe tend to think of it as homogenous, but that is rarely the case. Since 2003, the difference between the best and worst performing of the three sectors averaged 5.48%. An extreme example of this was in 2008, during the peak of the Great Financial Crisis, when Treasuries significantly outperformed corporates as investors clamored for safety. That year, the total return of the U.S. Treasury sector was 18.67% greater than the corporate sector.

Taking advantage of these divergent returns is the cornerstone of our investment strategy. We are constantly monitoring the investment grade market, looking for opportunities to increase exposure to sectors that present compelling relative value.

Q1 2023: A Textbook Example Of Our Strategy In Action

The year began with heightened market volatility driven by drastic changes in expectations of the Federal Reserve rate hiking path. Yet, we observed that investment grade corporate credit spreads were quite tight, even as the Fed aggressively increased the federal funds rate. Demand for corporate credit remained strong, as investors expressed optimism that the Fed would successfully tame inflation, which kept spreads from increasing. In the agency MBS pass-through sector, on the other hand, we noticed almost the exact opposite behavior, as nominal spreads remained at historically wide levels with spreads continuing to widen. This presented an attractive opportunity to rotate away from corporates and into mortgages, as the expected returns were more favorable and the trade was aligned with our overall macro outlook. (Recall that as a bond owner, it is beneficial for spreads to tighten during your holding period and vice-versa. Thus, all else equal, we prefer selling bonds with relatively tight spreads and replacing them with bonds with wider spreads.)

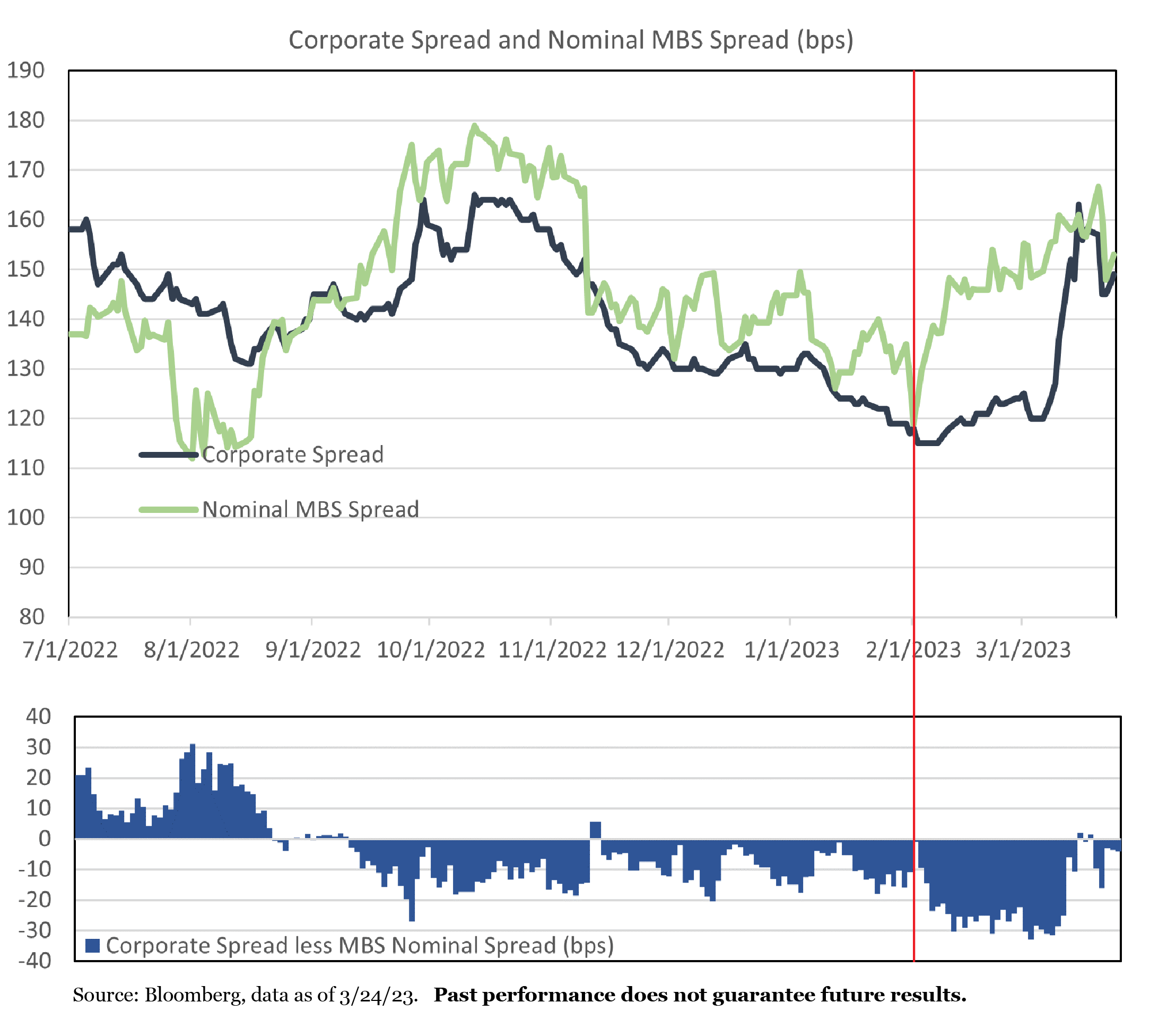

Our fundamental outlook for corporates has remained guarded for some time, and we continue to believe the aggressive Federal Reserve rate increases will negatively impact the corporate credit sector and will eventually benefit both the agency MBS and U.S. Treasury sectors at different points in the future. Even in the face of the aggressive tightening, spreads on the Bloomberg U.S. Corporate Investment Grade Index tightened 50 basis points (bps) from mid-October 2022, their most recent peak, to mid-February 2023. The chart below shows spreads on both the corporate and agency MBS sectors (top chart) and shows the differential (corporate less agency MBS spreads) on the bottom.

From the beginning of February (notated by the red line), we noticed that investment grade corporate spreads began to diverge from their agency MBS counterparts. The spread on the corporate sector was approximately 25 bps tighter than agency mortgages by mid-February. For some perspective, over the last two years, the corporate sector traded approximately 8 bps wider than agency MBS on average. This is exactly the type of opportunity we look for, particularly when it is supported by our macro view. Not only did we like the return potential of this trade, but it allowed us to reduce our exposure to the corporate sector, which is made up of almost 50% BBB rated credits (the lowest rung of the investment grade rating scale). Given our cautious view about corporate credit, this was a compelling opportunity, as it allowed us to increase our exposure to the higher quality agency MBS sector, which is made up of Treasury-like assets.

Since reducing our exposure to corporate bonds, troubles in the banking industry have caused corporate spreads to widen substantially. Of course, we did not predict that a banking crisis would occur, but our decision was driven by our views on the corporate sector, and the negative scenario we were concerned about is what ultimately unfolded.

Final Thoughts

Sector rotation, a key part of our investment strategy, is based on our assessment of macro trends and implemented in conjunction with in-depth analysis of the underlying securities. Recent volatility has created attractive entry points for us, including the example discussed above. We will continue to lean on sector rotation, as we are confident that the investment grade market will provide compelling relative value opportunities for the foreseeable future.

Daniel Oh

Vice President & Portfolio Manager

For more information about this strategy, please send us an email or call us at (800) 700-3316.

The Osterweis Funds are available by prospectus only. The Funds’ investment objectives, risks, charges, and expenses must be considered carefully before investing. The summary and statutory prospectuses contain this and other important information about the Funds. You may obtain a summary or statutory prospectus by calling toll free at (866) 236-0050, or by visiting www.osterweis.com. Please read the prospectus carefully before investing to ensure the Fund is appropriate for your goals and risk tolerance.

The Osterweis Total Return Fund may invest in fixed income securities which are subject to credit, default, extension, interest rate and prepayment risks. It may also make investments in derivatives that may involve certain costs and risks such as liquidity, interest rate, market, credit, management and the risk that a position could not be closed when most advantageous. The Fund may invest in in debt securities that are un-rated or rated below investment grade. Lower-rated securities may present an increased possibility of default, price volatility or illiquidity compared to higher-rated securities. Investments in foreign and emerging market securities involve greater volatility and political, economic and currency risks and differences in accounting methods. These risks may increase for emerging markets. Leverage may cause the effect of an increase or decrease in the value of the portfolio securities to be magnified and the fund to be more volatile than if leverage was not used. Investments in preferred securities have an inverse relationship with changes in the prevailing interest rate. Investments in Asset Backed and Mortgage Backed Securities include additional risks that investors should be aware of such as credit risk, prepayment risk, possible illiquidity and default, as well as increased susceptibility to adverse economic developments. It may also make investments in derivatives that may involve certain costs and risks such as liquidity, interest rate, market, credit, management and the risk that a position could not be closed when most advantageous. The Fund may invest in municipal securities which are subject to the risk of default.

Investing involves risk. Principal loss is possible.

Diversification does not assure a profit, nor does it protect against a loss in a declining market.

Complete holdings of the Osterweis Total Return Fund are generally available ten business days following quarter end and may be viewed at https://www.osterweis.com/mutual_funds/total_return/portfolio.

Holdings and sector allocations may change at any time due to ongoing portfolio management and should not be considered a recommendation to buy or sell any security.

A corporate bond is a debt security issued by a corporation and sold to investors. The backing for the bond is usually the payment ability of the company, which typically depends on money to be earned from future operations. In some cases, the company’s physical assets may be used as collateral for bonds.

Treasuries (including bonds, notes, and bills) are securities sold by the federal government to consumers and investors to fund its operations. They are all backed by “the full faith and credit of the United States government” and thus are considered free of default risk.

A safe haven is an investment that is expected to retain its value, or even increase in value, during times of market turbulence.

A mortgage-backed security (MBS) is a type of asset-backed security that is secured by a mortgage or collection of mortgages. Agency MBS securities are issued by quasi-government entities and carry an implied guarantee by the federal government.

The Bloomberg U.S. Corporate Bond Index measures the investment grade, fixed-rate, taxable corporate bond market. It includes U.S.D denominated securities publicly issued by U.S. and non-U.S. industrial, utility and financial issuers.

The Bloomberg U.S. Treasury Index consists of public obligations of the U.S. Treasury with a remaining maturity of one year or more.

The Bloomberg U.S. Aggregate Bond Index is an unmanaged index which is widely regarded as the standard for measuring U.S. investment grade bond market performance.

The Bloomberg U.S. Mortgage Backed Securities (MBS) Index tracks agency mortgage backed pass-through securities (both fixed-rate and hybrid ARM) guaranteed by Ginnie Mae (GNMA), Fannie Mae (FNMA), and Freddie Mac (FHLMC). The index is constructed by grouping individual TBA-deliverable MBS pools into aggregates or generics based on program, coupon and vintage.

These indices do not incur expenses and are not available for investment. These indices reflect the reinvestment of dividends and/or interest. Historical fixed income index data is provided for informational purposes only, not as an indication of future Fund performance. Source: Bloomberg Indices. It is not possible to invest directly in an index.

Absolute return strategies are not intended to outperform stocks and bonds during strong market rallies and may underperform during strong positive market performance.

A basis point is a unit that is equal to 1/100th of 1%.

Alpha is a measure of the difference between the portfolio’s actual return versus its expected performance, given its level of risk as measured by Beta. It is a measure of the historical movement of a portfolio’s performance not explained by movements of the market. It is also referred to as a portfolio’s non-systematic return.

Spread is the difference in yield between a risk-free asset such as a Treasury bond and another security with the same maturity but of lesser quality.

Investment grade bonds are those with high and medium credit quality as determined by ratings agencies.

The fed funds rate is the rate at which depository institutions (banks) lend their reserve balances to other banks on an overnight basis.

Standard Deviation is a measure of dispersion that represents the degree to which an investment’s returns vary around a mean. The greater the Standard Deviation, the more volatile an investment’s returns were during the period measured. This statistic is calculated using the population standard deviation formula: Standard Deviation = Square root of [(Sum of squared deviations from mean)/(Number of returns in the period measured)] If the return periodicity is less than one year, the standard deviation is multiplied by the square root of the number of periods in one year in order to arrive at an annualized measure.

Credit Quality weights by rating were derived from the most recent data available as determined by Standard and Poor’s. Grades are assigned to bonds by private independent rating services such as Standard & Poor’s and these grades represent their credit quality. The issues are evaluated based on such factors as the bond issuer’s financial strength, or its ability to pay a bond’s principal and interest in a timely fashion. Ratings are expressed as letters ranging from ‘AAA’, which is the highest grade, to ‘D’, which is the lowest grade. In situations where Standard & Poor’s has not issued a formal rating, the security is classified as not rated (NR). Additionally, common stocks, if any, are classified as NR.

Osterweis Capital Management is the adviser to the Osterweis Funds, which are distributed by Quasar. [OSTE-20230331-0825]

© Osterweis Capital Management

Read more commentaries by Osterweis Capital Management