If I did not have bad luck, I would have no luck at all.

Having prepared thoroughly for two weeks of client visits in England and Ireland, I found my materials rendered nearly irrelevant by the developing banking crisis. Clients were pressing for insight and answers that were difficult to come by. Work related to the evolving stress required a long string of consultations, many of which ran deep into the European evenings.

Further, transit strikes made traveling from place to place in London a challenging guessing game. Getting around Dublin was only marginally easier; I arrived on a long weekend that included St. Patrick’s Day and a major rugby match between England and Ireland. Some key thoroughfares had been taken over by revelers.

Nonetheless, the time spent on the road proved beneficial. As always, the exchanges with clients were illuminating. I thought it would be useful to summarize the content of the conversations for broader consumption.

1. Even though I was more than 5,000 miles away from Northern California, I got a lot of questions about Silicon Valley Bank (SVB), and whether other banks are at risk.

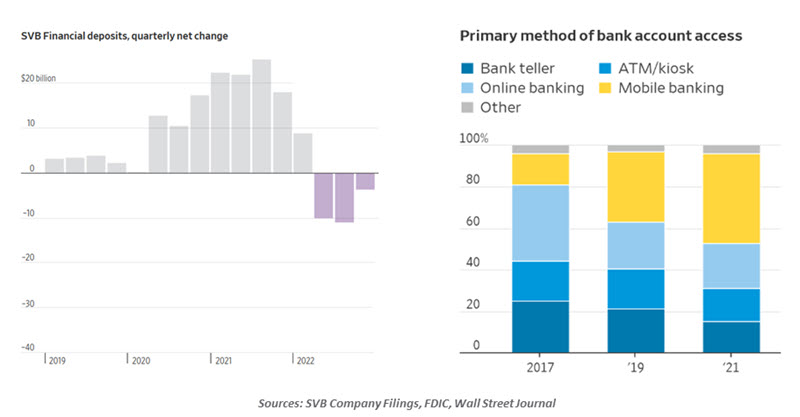

As we discussed a couple of weeks ago, SVB’s troubles began when Fed tightening caused the cost of its funding to rise much more rapidly that the yields it was earning on its assets. A significant contributing factor to the imbalance was the erosion of the SVB deposit base, a trend that began in early 2022. Capital available to technology companies began to diminish last year, leading them to draw down their bank balances. SVB’s concentration to this sector made it particularly vulnerable to funding loss.

By all accounts, SVB miscalculated the longevity of their deposits; when money began to depart, the bank had to sell some of its long-term securities at a loss. The panic that followed was fueled by private communications channels, social media and the prevalence of mobile banking. Ironically, those platforms were created by Silicon Valley firms. SVB’s surroundings, so important to its growth, may have contributed to its downfall.

SVB’s surroundings contributed to both its rise and its fall.

The extent of the Fed’s interest rate increases did come as a surprise to almost everyone last year. But SVB’s concentrations and clientele created unique vulnerabilities, and its strategy failed to respect inherent risks. These failings aren’t entirely unique to SVB, but they are far from ubiquitous. Strong balance sheets and balance sheet management elsewhere in the industry should help limit contagion.

2. That said, it is worth reinforcing that investors and depositors may not be performing the deepest level of analysis as they contemplate the safety of individual firms or the financial system. During the middle weekend of my trip, a marriage between UBS and Credit Suisse was arranged by Swiss authorities. As we noted last week, the circumstances surrounding that situation and the SVB failure are entirely distinct. But the two became married in the minds of many (including some of our clients), forming an impression that the global banking system was at serious risk.

The past two weeks have been a little quieter, but once lost, comfort is difficult to re-establish. We need to remain on guard for the next troubling headline.

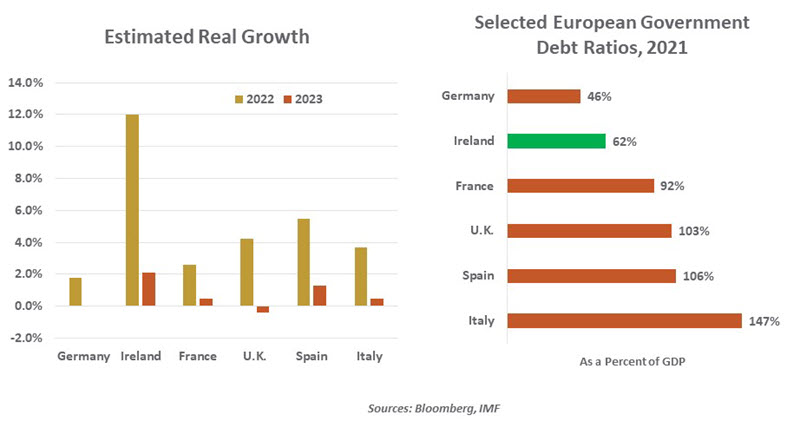

3. The outlook for the United Kingdom is very challenging. Inflation there has been stubbornly high: more than 10% over the course of the last year. British dependence on foodstuffs from eastern Europe, among other factors, has contributed to a 15% increase in grocery prices over the last twelve months. Because mortgages in the U.K. are largely short-term in nature, interest rate increases from the Bank of England have caused monthly payments to double or triple in some cases. Consumer confidence is at rock bottom levels.

The persistent inflation was among the root causes of the strikes I experienced. (Teachers and doctors also walked off while I was there, but I was not in need of their services.) The government had been offering wage increases that would look generous in normal times, but were not keeping pace with costs of living. Labor supply in Britain has been hindered by broadening disability (partly the result of long COVID) and Brexit-related declines in immigration. The possibility of a crippling wage-price spiral seems more proximate in the U.K. than it is anywhere else.

4. Meanwhile, less than 100 miles to the west lies an economic counterpoint. Ireland has been carrying the euro area economy of late; without its contribution to growth, the eurozone might have fallen into recession by now. To be fair, some of Ireland’s gross domestic product (GDP) is attributable to profit shifting by multinational companies aiming to take advantage of Ireland’s low tax rates. But even allowing for this, Ireland’s economy has a number of advantages.

The U.K. and Ireland offer a stark contrast in economic policy and performance.

Ireland is a relatively young and well-educated country, with a labor force that can support inbound industry. Ireland had serious debt issues ten years ago, but unlike some of its European brethren, it accepted the austerity program prescribed to it and emerged earlier and stronger than anticipated. Its ratio of government debt to GDP is one of the lowest in Europe, buffering its finances (to a degree) from recent interest rate increases. Ireland markets its economy very effectively, all over the world. The outlook for the country remains bright…green.

5. Clients in the United Kingdom and Ireland are keen observers of the U.S. Many are very familiar with the debt ceiling drama that will reach a crescendo this summer. As costly as it might be for America, a bad outcome would also ripple through other countries: Treasury yields are the benchmark for the costs of debt all over the world. I promised to do my best to solve the problem.

I’ll be home for a few weeks trying to catch my breath. My next major trip will be to Asia in early May: China and Hong Kong are on the itinerary for the first time in four years. I’m hoping that my departure will not invite another round of banking problems.

Information is not intended to be and should not be construed as an offer, solicitation or recommendation with respect to any transaction and should not be treated as legal advice, investment advice or tax advice. Under no circumstances should you rely upon this information as a substitute for obtaining specific legal or tax advice from your own professional legal or tax advisors. Information is subject to change based on market or other conditions and is not intended to influence your investment decisions.

© 2023 Northern Trust Corporation. Head Office: 50 South La Salle Street, Chicago, Illinois 60603 U.S.A. Incorporated with limited liability in the U.S. Products and services provided by subsidiaries of Northern Trust Corporation may vary in different markets and are offered in accordance with local regulation. For legal and regulatory information about individual market offices, visit northerntrust.com/terms-and-conditions.

© Northern Trust

Read more commentaries by Northern Trust