Silicon Valley: The Consequences of a Bank's Failure

Membership required

Membership is now required to use this feature. To learn more:

View Membership BenefitsWe had intended to use this space to share a fulsome preview of next week’s Federal Open Market Committee (FOMC) meeting. But the Federal Reserve has been preoccupied with the fallout from the failure of Silicon Valley Bank (SVB), and so have we.

As of this writing, repercussions of the event are still accumulating. Here is a summary of what we know, what we think and what we will be watching for.

· The bank’s name and locus might lead one to believe that exposure to tech firms led to the bank’s demise. That is correct, but not in the way you might think.

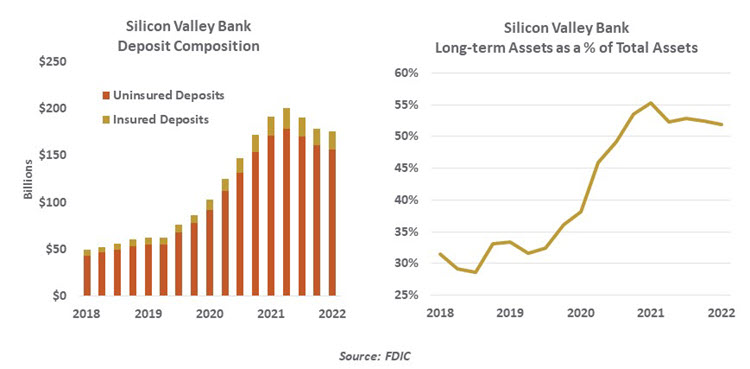

The firm was a noted provider of capital to start-up firms. But lending losses did not lead to its failure. Instead, it was something old-fashioned: a depositor run. For years, SVB’s tech sector clientele benefited from rapid investment and high revenues, which they deposited at SVB. More recently, their fortunes have changed, leading them to run down deposits.

The withdrawals weighed on SVB’s balance sheet and its reputation. Spurred by social media communication, departures accelerated. To raise cash, SVB sold some of its bond holdings at a significant loss. This added to the anxiety surrounding the company.

Many of the depositors that rushed to withdraw were the same firms that SVB had financed when their own balances sheets were less than fully creditworthy. There is apparently no loyalty in liquidity.

· Early accounts suggested that the Federal Reserve broke Silicon Valley Bank. We do not agree. The bank broke the bank.

Ever since the sky-high interest rates and inverted yield curves of the 1980s, banks have been engaged in the practice of asset/liability management. The essence of the exercise is simple: matching the timing of cash flows produced by assets and liabilities. (Or, at very least, not allowing too much of a mismatch between the two.)

SVB invested in long-term Treasury securities, attempting to earn better yields. But their deposit funding proved short-term in nature. When interest rates started rising a year ago, asset values fell and funding departed. The situation is not dissimilar to the plague that spread across the U.S. savings and loan industry forty years ago.

SVB was not the only bank with unrealized losses on its investment portfolios; yield movements over the last year have put most firms in that position. This is not usually cause for alarm: absent a bond default, which is rare, losses are not realized if the notes are held to maturity. The unique aspect of SVB was that, because of deposit withdrawals, it was forced to sell its holdings at a loss, no longer able to hold them for their full terms.

The vulnerability was evident in the company’s quarterly reports, hiding in plain sight. Adding to the risk was the fact that SVB tripled in size during a two-year period. Why the bank’s management, board and supervisors did not raise more strenuous objections will be an important focus of the post mortem.

· Industry observers have pointed out that SVB, with more than $200 billion of assets, was not subject to the highest level of regulatory scrutiny. In an effort to reduce burdens on firms not seen as systemically important, the Federal Reserve introduced a tiering system a few years ago. SVB was not required to perform annual stress testing or comply with the highest level of liquidity reporting.

SVB’s problems were hiding in plain sight

Events over the past week will certainly lead to a fresh look at systemic risk. Clients of SVB faced uncertain futures when access to funds that remained on deposit with the bank were inaccessible. Their clients and vendors might subsequently have been impaired. Some might suggest that the accumulation would still not be enough to topple the financial system, but market movements since March 9 might call that conclusion into question. Systemic problems often start small, and then snowball.

Good supervision is needed to make regulation most effective. Both will likely be reinforced after the dust settles.

There is a lot of finger pointing going on at the moment. Those most responsible will only be identified through thorough investigation. For now, best to fix the problem and not the blame.

· The developments of the past ten days illustrate the powerful role that psychology plays during unsettled intervals. To be sure, rumor often travels faster than fact during periods such as this. But human beings process incoming information very differently under stress.

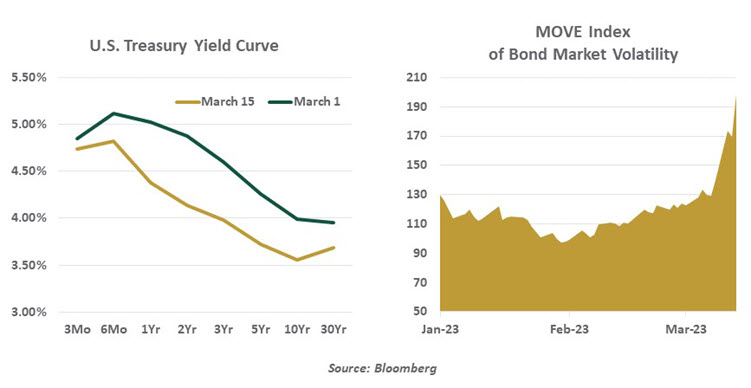

There is a substantial body of literature detailing the extremes of risk aversion that come over investors when they sense that their money is in peril. The recent flight to quality in the Treasury markets illustrates this; government bond yields are substantially lower than they were earlier this month. Trading has been exceptionally volatile, adding to the spreading sense of unease.

In the absence of conclusive information, observers fall back on heuristics: snap judgments that may not be fully informed. This has led to broad pressure on banks, even those with little resemblance to SVB. Late in the week, Credit Suisse found itself under duress, leading some to link its challenges to SVB and predict a global banking crisis. There is data that dissociates the two situations, but belief is overpowering analysis. Rational or not, it must be respected.

· It is much more difficult for policymakers to address crises of confidence than crises of finance. The efforts of American policy makers did not get off to the best start: an initial statement from the FDIC indicated that SVB depositors above the $250,000 insurance ceiling would receive a “dividend” toward their balances, with remaining restitution based on the resolution of the institution. A partial payment would have offered an estimate of salvage value, which would not likely have cheered markets.

Get ready for another round of discussion about moral hazard.

As last weekend wore on, a more intelligent design emerged. The FDIC agreed to cover all of the deposits at SVB and Signature Bank, and stated that monies would be fully available when the doors reopened on Monday. The move was designed to discourage flight and end the frantic search by SVB depositors for fresh sources of credit.

While the FDIC was hoping to be surgical in its support, there have been reports throughout the week that deposits are in motion. Some have reportedly moved from small banks to large ones, in the belief that larger firms would be at least risk in a systemic crisis. Stemming these flows would require making the deposit insurance waiver universal, as it was in 2008.

Critics point to the moral hazard introduced by backstopping large depositors, who (in theory) are supposed to be exerting some discipline over the firms that hold their funds. But there is scant evidence that that oversight is occurring, or having any influence on bank behavior. Universal deposit insurance with commensurate charging would preserve incentives for firms to operate prudently. But it will likely be politically unpopular, and banks will not welcome the higher insurance expense.

I am not sure I would characterize the assistance given SVB and Signature Bank a “bailout.” Depositors are not investors, and deposit insurance is a premium paid by banks, not taxpayers. Shareholders and unsecured debtholders will be lucky to preserve any of the money they had invested in the companies. During the 2008 crisis, then-Fed Chairman Ben Bernanke observed that “There are no atheists in foxholes, and no ideologues in financial crises.” There will be time to sort out how incentives should be realigned. But now is not that time.

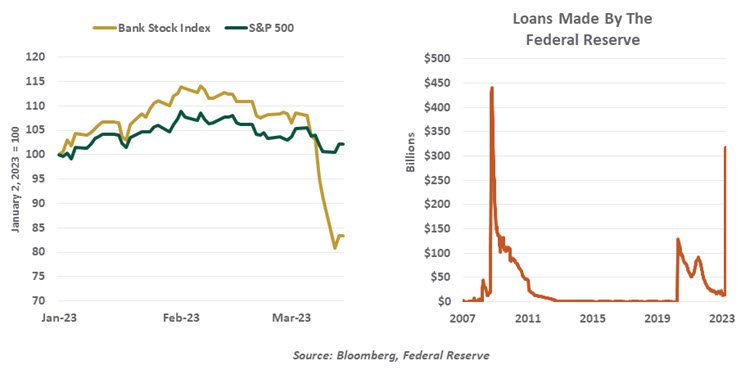

· Speaking of the Federal Reserve: The central bank introduced the Bank Term Funding Program (BTFP) over the weekend, which allows banks to borrow money for up to one year by posting collateral as security. Importantly, credit is extended at the face value, not market value of the securities. The BTFP is designed to allow banks that might have otherwise had to sell holdings to raise cash to satisfy deposit withdrawals.

Emergency asset sales are among the most prominent accelerants during financial crises. They add to the downward pressure on both markets and confidence and can cause problems in one sector to jump over to others.

The BTFP draws on a multitude of 2008-era programs. Some generated a lot of activity; the mere presence of others settled conditions without a single dollar being drawn. Early evidence suggests that the BTFP, along with the Fed’s normal discount window operations, have been used extensively over the past week.

Banking stress greatly complicates central bank decisions.

Some are worried that the monies that might be injected into the system under the BTFP represent an easing of monetary policy, but any liquidity provided will be temporary.

· The issues that have emerged over the past ten days have complicated the practice of central banking.

For more than a year, post-pandemic inflation has challenged monetary policy. Finding themselves behind the curve, central banks have tightening credit aggressively. Their efforts put a ceiling on inflation, but the pace of price increases remains well above target in a number of major economies. As long as that is the case, interest rates will head higher.

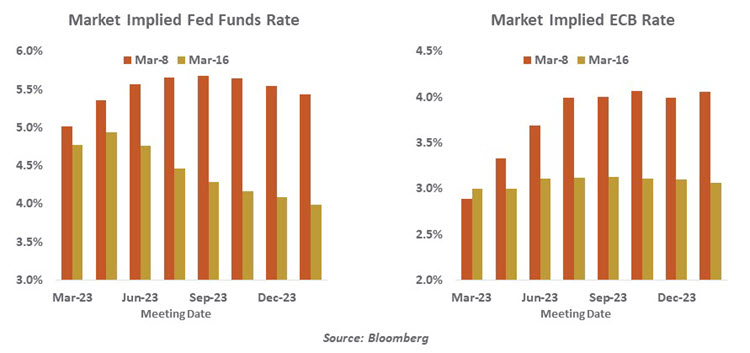

But an unstated mandate for all central banks is the maintenance of financial stability. Normally that is addressed through supervision (an example of “macroprudential” policy). In times like this, that responsibility crowds its way into interest rate discussions. Markets are clearly anticipating that systemic problems will take precedence. Expectations for the paths of overnight interest rates have been upended since March 8.

During periods where risk aversion is most powerful, market signals like those shown above might become less reliable. But it would be dangerous to dismiss this signal. While it remains a very low probability, a scenario where central banks have to do a significant U-turn cannot be ruled out.

The European Central Bank (ECB) was the first to meet since banking turmoil appeared, deciding to increase interest rates by 50 basis points this week while acknowledging the potential for financial dislocation. The Bank of England and the Federal Reserve will follow suit next week. In the latter case, we are still expecting a quarter-point increase, but much could change between now and next Wednesday.

Over the past few days, we’ve often been asked what the impact of recent events will be on economic activity. It is difficult to say, at this early stage. If the troubles of SVB, Signature Bank and Credit Suisse can be contained and market order is restored, then the outlook would not be significantly affected. If not, the flow of capital to households and firms could be impaired, placing the economy at some risk. Deeply indebted governments would not be in the best position to offer sufficient stimulus. Recession would be almost assured.

It’s somewhat too early to say how the economy will react to what’s just happened.

We’ve deferred our forecast review cycle by a bit to allow time for conditions to (hopefully) clear. We won’t get any major economic data for a while, and upcoming numbers will probably not reflect the impact of recent market movements. Whatever we decide, the potential error band around the outcome may be large.

Even in the best case scenario of no further contagion, recent events may cast a lingering shadow over the financial sector. Banks will guard their capital to maintain their customers’ confidence, and the fear of enhanced regulation may add to their caution. More broadly, banks cannot function without the confidence of their clients and investors. Talk of bailouts, uninsured deposits and unrealized losses can snowball into broader suspicion of the entire sector.

Fortunately or unfortunately, we have quite a few recent experiences to draw on as we try to diagnose the current affliction. We’ll be following the health of markets and the economy closely over the coming weeks, and will endeavor to provide you the vitals.

Membership required

Membership is now required to use this feature. To learn more:

View Membership BenefitsSponsored Content

Upcoming Virtual Events View All