We are now engaged in the difficult exercise of determining how quickly inflation will recede. The endeavor has forced us to delve deeply into the details.

A good example is our analysis of the U.S. labor market. As we wrote recently, it is difficult to reconcile all of the data: we have strong job growth, a plethora of job openings and yet wage gains have weakened over the past few months.

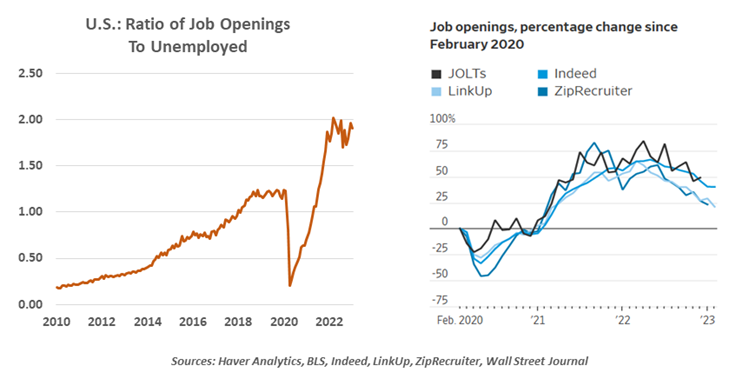

Some suggest, though, that demand for labor isn’t what it appears on the surface. Updated readings from the Bureau of Labor Statistics this week showed 10.8 million available posts, which compares to just over five and a half million people who are looking for work. The ratio of 1.9 between the two remains very high by historical standards.

The near-record number of job openings may be somewhat misleading.

Alternative measures of job openings, however, are not showing the same number and breadth of vacancies. Indexes kept by job sites like Indeed and LinkUp show much slower growth in postings. These series are based on actual counts, while the Labor Department’s job opening series is based on a survey. Response rates to that survey have been running at 32%, half the level seen prior to the pandemic. That diminishes the value of the series.

It is also hard from the aggregates to determine the intensity of demand. Some listings are opportunistic; matches will be made only under the right terms. Situations like these are less likely to add to wage inflation.

As further illustration of the contradictory data we have been getting, more than 300,000 new jobs were created in February, but average hourly earnings increased a scant 0.2%. These are hardly the signs of a weak labor market, but neither are they indicative of one that is overheating. As the Federal Reserve considers what to do next, it would be advised to look closely at the want ads.

Information is not intended to be and should not be construed as an offer, solicitation or recommendation with respect to any transaction and should not be treated as legal advice, investment advice or tax advice. Under no circumstances should you rely upon this information as a substitute for obtaining specific legal or tax advice from your own professional legal or tax advisors. Information is subject to change based on market or other conditions and is not intended to influence your investment decisions.

© 2023 Northern Trust Corporation. Head Office: 50 South La Salle Street, Chicago, Illinois 60603 U.S.A. Incorporated with limited liability in the U.S. Products and services provided by subsidiaries of Northern Trust Corporation may vary in different markets and are offered in accordance with local regulation. For legal and regulatory information about individual market offices, visit northerntrust.com/terms-and-conditions.

© Northern Trust

Read more commentaries by Northern Trust