We’re fielding a lot of questions lately asking for a description of how the current cycle might end. Do we hold out hope for a soft landing, with no significant economic damage, or a soft-ish landing, with limited pain? Could we see no landing at all, with activity never slowing and unemployment never rising? These visions feel optimistic after digesting a paper presented at last week’s Chicago Booth Monetary Policy Conference, showing ample precedents for a recessionary hard landing.

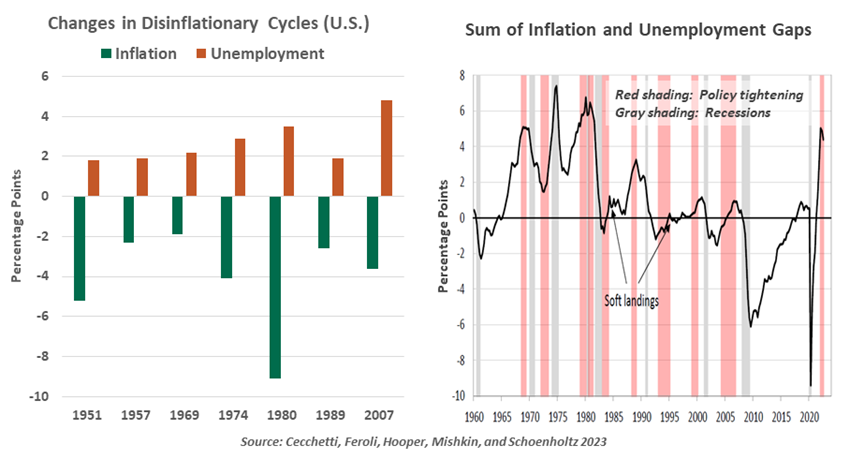

The authors, including a former Fed governor, surveyed 16 disinflationary cycles since World War II across the U.S., Canada, the U.K. and Germany. They computed a sacrifice ratio for each interval: the economic cost associated with a one percentage point decline of trend inflation. Every episode showed a consistent story of sacrifice accompanying lower inflation.

Whenever a central bank acted decisively to arrest inflation, a recession ensued. Rare soft landings, like in the mid-1990s, did not fit the authors’ criteria: central banks acted preemptively to prevent inflation in that instance, as opposed to reacting to high inflation.

When central banks fight inflation, economies can expect to suffer.

Despite their conclusions, the authors go on to reject calls to adjust central banks’ inflation targets. A higher target would require less tightening and economic damage. However, higher inflation brings greater uncertainty and higher costs, borne especially by lower-income households. The pain today does not compare to the long-run risks of persistently high inflation. We agree.

The study rests on the assumption that past is prologue, and events to come will match the experiences of past cycles. History is important, but new experiences are still possible, too. A response by Federal Reserve governor Philip Jefferson noted that today’s challenges are driven by pandemic disruptions not seen in the historical data. Jefferson highlighted today’s supply chain disruption, lower labor force participation rates and central bank crisis responses that are not comparable to the postwar episodes studied.

A recent survey of market participants concluded that we should stop envisioning a landing, with more apropos analogies including a drifting balloon. The analogy is comforting: a balloon is naturally buoyant and can make multiple attempts at landing. But as recent events have reminded us, the risks of a crash can never be entirely ruled out.

© Northern Trust

Read more commentaries by Northern Trust