Central banks around the world have been raising short-term interest rates aggressively for almost a full year now. All of the tightening has, however, put central banks into a kind of hole.

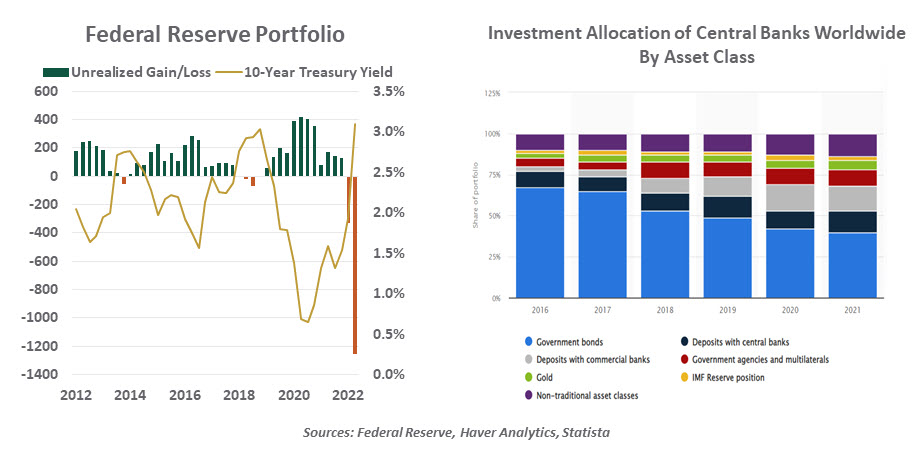

Over the past 15 years, central banks have become some of the largest asset managers in the world. Portfolios accumulated under quantitative easing (QE) now total an estimated $44 trillion worldwide. For the Federal Reserve, the Bank of England (BoE), and the European Central Bank (ECB), holdings are entirely composed of bonds; elsewhere, central banks invest in a range of asset classes. The Bank of Japan, for example, owns more than 60% of the country’s exchange-traded funds.

The interest on central bank portfolios is used to pay the organization’s expenses, with any excess remanded to the host government. Over the last five years, the Federal Reserve has shared an average of $78 billion annually with the U.S. Treasury, while the BoE has forwarded £100 million annually to the British Treasury. Since last March, however, those positives have turned negative.

That’s what’s going on above the surface. In the background, last year’s falling asset prices diminished the market value of central bank portfolios. It is estimated that the Federal Reserve’s holdings are underwater by $1.3 trillion; the ECB’s positions are worth an estimated $800 billion less than their face values.

To be sure, these paper losses will only be realized if securities are sold. (Bond values converge to their face values as maturity approaches.) Many central bank portfolios are in runoff mode now, and the hope is that balance sheets can decline naturally. But if there is a need to accelerate balance sheet reductions, sales will be required. And that will trigger gains or losses.

The Federal Reserve has expressed an intention to maintain a Treasury-only investment portfolio, which would require the Fed to liquidate $1.5 trillion of mortgage backed securities which have very long maturities. Those bonds currently carry an unrealized loss of $431 million.