A plunge in pricing power was one of the most notable developments we found in our latest quarterly survey of our credit analysts, who follow more than two dozen industries. The survey results painted a picture of a corporate sector under increasing stress but nowhere near the point of collapse.

The implications of lower pricing power

As we have noted in the past, when companies can’t pass rising expenses on to customers, two things tend to happen. On the minus side, profit margins typically decline and we saw a modest dip in margins in the fourth quarter. On the plus side, inflation generally subsides and that has been happening as well. Both the Consumer Price Index and the Producer Price Index have moved lower in recent months. We are seeing actual deflation in core goods and durable goods. The supply-chain bottlenecks that plagued the economy for so long seem to have loosened considerably. Our credit analysts are seeing cost pressures ease, particularly on the manufacturing side.

Other key observations

The decline in pricing power was not the only important observation from our survey. Also notable were the following:

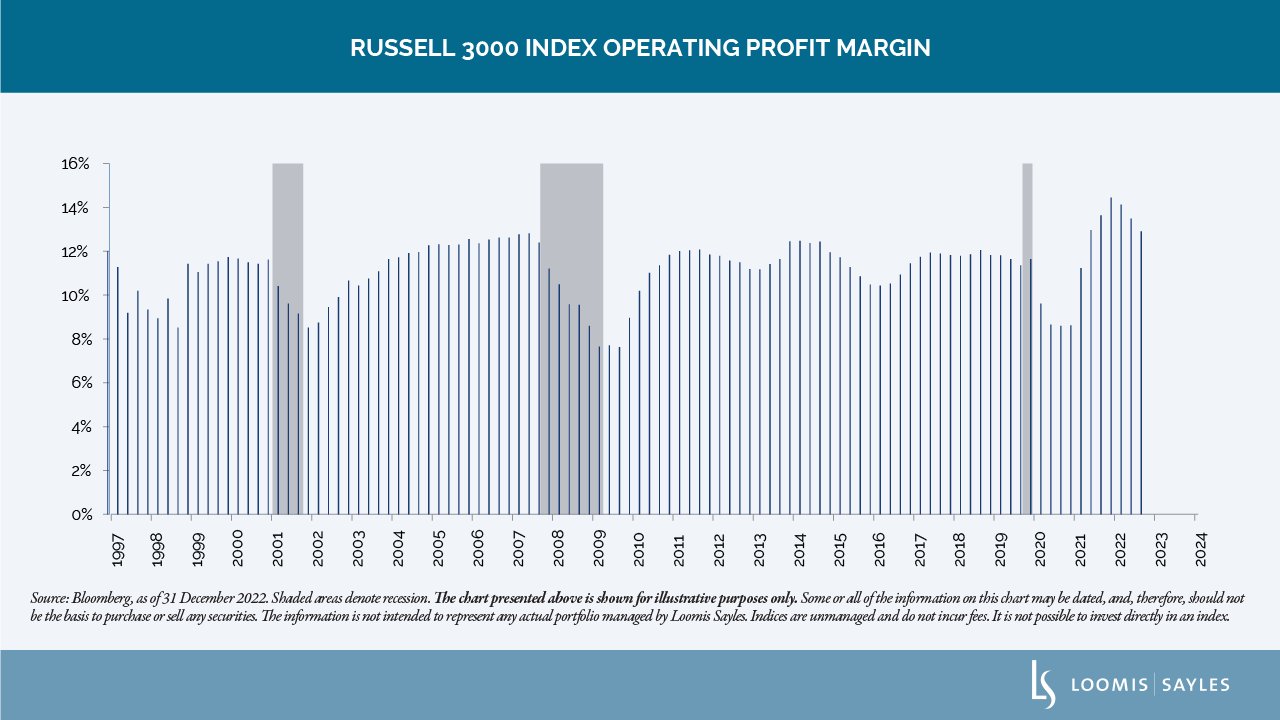

• Profit margins have been falling, but remain high by historical standards. It is worth pointing out where we were at the start of this slowdown. Profit margins for the Russell 3000 Index, which represents 98% of US publicly-traded equities, reached an-all time high in 2021. Though they have declined in recent quarters, margins are still near prior-cycle peaks reached in the expansions of the last 25 years. Put another way, the “cushion” companies have relied on has shrunk, but it has not disappeared entirely. That helps explain why defaults have remained low to date.

• Leverage has been climbing. Leverage, which we define as the ratio of debt to profits, bumped up moderately in the fourth quarter of 2022, particularly in the manufacturing sector. Debt has held steady and profits have started to decline, making leverage metrics look worse. While we view this uptick as concerning, it is important to point out that our credit analysts do not see disaster looming. Asked about the prospects of a crisis in their industries, our analysts believe the likelihood of a crisis has increased in only 2 of 30 industries. That relatively sanguine view squares with credit spreads that have reflected more optimism of late. Debt markets remain open and debt service costs seem to be manageable.