British diplomat T.E. Lawrence once quipped: “The printing press is the greatest weapon in the armory of the modern commander.” But its value extends far beyond conflict. Central banks’ monetary printing presses allowed a decisive set of stimulus packages to be funded during the pandemic. Now, the printers are helping central banks sustain their operations.

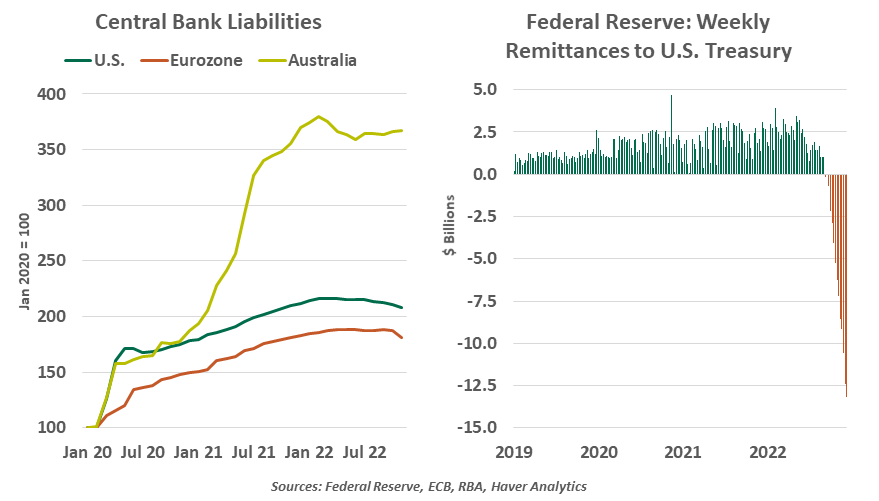

Faced with a crisis, central banks around the world turned to quantitative easing: buying a great number of assets to ensure sufficient liquidity, especially in the market for government debt. As the banks loaded up on those sovereign bonds, they earned more and more interest income.

When most central banks earn a profit, it is paid back to their country’s treasury. The European Central Bank is an exception, paying its profits out to its members’ national banks. In 2021, the Federal Reserve had residual earnings of $107.8 billion, an increase of $19.3 billion from 2020. The amounts remanded to the Treasury reduced annual fiscal deficits.

The good times quickly came to an end this year as central banks curtailed their asset purchases, holding fewer interest-earning securities. Programs like the Federal Reserve’s reverse repo facility have been needed to absorb extra liquidity in markets, and their high utilization has led to higher interest expenses. And none of these fluctuations have any bearing on banks’ costs of operations.

The tide turned quickly. After remitting an average of $1.6 billion annually in the past decade, the Fed has fallen into negative earnings. Income for central banks around the world will keep falling as they exit their bond-buying programs and react to ongoing volatility in foreign exchange markets.

These losses do not include the effect of marking the central banks’ balance sheets to market. Bonds fall in value as prevailing interest rates rise. As of the third quarter, the Fed estimated its unrealized portfolio losses had exceeded $1.1 trillion—and rates have only risen since. Estimates for the Bank of England’s paper losses are £200 billion and counting. But as these banks hold most securities to maturity, these losses will not be realized.

Fortunately for national treasuries, while central banks’ income is paid in as a positive cash flow, losses do not need to be paid out. Most nations have a system of sharing or deferring these obligations. For instance, the Fed’s net losses are accrued as a “deferred asset” on its balance sheet. The deferred asset is the amount of net earnings that the Fed will need to realize before remittances to the U.S. Treasury resume.

The printing press is central banks’ saving grace. They have a monopoly on the creation of new money and can print whatever they need to cover shortfalls. These deficits are small relative to the overall money supply, and the quantity of new money is too minor to be inflationary. But that is not to say the printing presses can run unfettered. Excessive printing devalues a currency, and a prolonged negative capital position will erode trust. Central banks need credibility to execute monetary policy, and a loss of it could spark a financial crisis. Emerging markets have been at the greatest risk, but contagion is a risk for every bank.

|

A central bank is a rare entity that cannot go bankrupt.

|

While the net income or losses of central banks are worth monitoring, they should be kept in context. No central bank is chartered to earn a profit nor to prevent a loss. These positions do not interfere with bank’s core missions of executing monetary policy and regulating the financial system. As excess liquidity falls and interest rates normalize, central banks will end their deficits. The printing press will soon take a well-earned respite back in the arsenal.

Information is not intended to be and should not be construed as an offer, solicitation or recommendation with respect to any transaction and should not be treated as legal advice, investment advice or tax advice. Under no circumstances should you rely upon this information as a substitute for obtaining specific legal or tax advice from your own professional legal or tax advisors. Information is subject to change based on market or other conditions and is not intended to influence your investment decisions.

© 2022 Northern Trust Corporation. Head Office: 50 South La Salle Street, Chicago, Illinois 60603 U.S.A. Incorporated with limited liability in the U.S. Products and services provided by subsidiaries of Northern Trust Corporation may vary in different markets and are offered in accordance with local regulation. For legal and regulatory information about individual market offices, visit northerntrust.com/terms-and-conditions.

© Northern Trust

Read more commentaries by Northern Trust