Doug Drabik discusses fixed income market conditions and offers insight for bond investors.

I didn’t want to turn this message into a dispute about a recession. After all, it’s just a word, and, as we’ve experienced, words and definitions can be changed to meet an agenda. What is more important is that every time you put gas in your car or buy groceries for the table, you are likely feeling the pains of inflation. Inflation and its effects touch nearly all consumers with no prejudice to economic standing or asset selection. It impacts bonds, stocks, cash, homes, cars… all assets. The strategic actions we have been advocating for the last couple of months address the existing inflationary environment and may better position fixed income assets to endure an officially acknowledged recession.

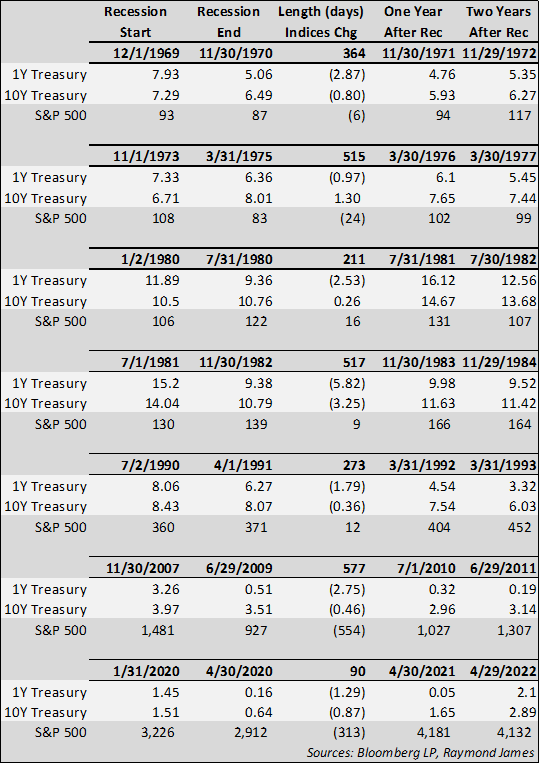

Don’t get lost in the data, after all, past occurrences are not exact predictors of the future. However, the trends or tendencies may provide insights that help to divulge strategic biases. This chart reveals data points from the last seven recessions. Some observations:

- In all 7 occurrences, 1-year Treasury yields were lower at the end versus start of the recession.

- In all 7 occurrences, the 10-year Treasury yield had less nominal and percentage moves versus the 1-year Treasury (the short end of the Treasury yield curve displays more change than the long end of the Treasury curve)

- In 5 of the 7 recessions, the 1-year Treasury yield was still lower one year after the end of the recession.

- In 4 of the 7 recessions, the 10-year Treasury yield was still lower one year after the recession ended.

- In all 7 occurrences, the S&P Index was higher one year after the recession ended.

Excluding the last 3 month recession in 2020, the rest have lasted between 7 months and 1 year & 7 months. Couple this with leanings toward lower rates one and even two years beyond the recession, and it becomes clearer why extending out on the yield curve now while rates are elevated may work to an investor’s advantage. Locking into higher yields may posture the fixed income allocation for higher yields for longer. Laddered structures may add the benefit of mitigating uncertainties in the less apparent and less consistent curve behaviors.