Fed’s Bullard Warns Fed Funds Rate Could Go To 5-7%

Membership required

Membership is now required to use this feature. To learn more:

View Membership BenefitsIN THIS ISSUE:

1. Fed Spokesman Warns Rates Could Go Much Higher

2. Fed’s Bullard Warns Fed Funds Rate Could Go To 5-7%

3. Bullard Is Outspoken, But Does He Have A Point?

4. Can The Fed Pull Off Higher Rates Without A Recession?

5. Another Way To Lower Inflation – Stop Deficit Spending

Overview – Fed Spokesman Warns Rates Could Go Much Higher

A high level Fed official warned last Thursday that the Fed Funds rate might have to go to 5%-7% to get inflation under control. This was a shocker! Markets plunged immediately after he said it. Fortunately, no one else at the Fed seems to agree with him.

While there is widespread agreement that the Fed Funds rate has to go up more to get inflation under control, no one I read thinks the rate will go much above 5%. Today, I’ll talk about what this Fed official said and offer some suggestions why he may have said it.

We’ll also look at some of the latest inflation indicators and how they have declined in recent months. While the declines are welcomed, inflation is still far above the Fed’s 2% target. And interest rates have further to rise, but not likely to anywhere near 7%.

Finally, I want to remind my clients and readers that there is another way to largely eliminate inflation. While this option seems like the obvious solution, virtually no one talks about this anymore. But we should be.

All this should make for an interesting letter. Let’s get started.

Fed’s Bullard Warns Fed Funds Rate Could Go To 5-7%

For most of November, Fed-watchers and investors were working on the assumption that the Fed Funds target range, currently at 3.75%-4.0%, would likely rise by 50 basis points to 4.25%-4.50% at the next Fed Open Market Committee (FOMC) policy meeting on December 13-14.

The thinking was also that the FOMC would probably raise the Fed Funds rate by another 0.25% at its next policy meeting on January 31-February 1 next year. Then, with the Fed Funds target range at 4.50%-4.75%, the widespread expectation was that the Fed would stop hiking rates and pause to see how much inflation comes down in the first half of next year.

This plan is fully priced in by the financial markets, and most investors seemed pretty comfortable with it. We all know the Fed needs to get inflation down, and raising short-term rates is widely acknowledged to be the most effective way to accomplish this task.

The stock markets actually started to rebound last month, and most equity investors were optimistic the uptrend would continue in December and 2023 as well. That was until last Thursday.

On Thursday morning last week, the President of the Federal Reserve Bank of St. Louis, James Bullard, said in a speech that he believes the Fed Funds rate might have to rise to 5%-7% to get inflation down to the Fed’s target of 2%. This came as a shock to the markets! No one has been suggesting the Fed Funds rate will rise above 5% and certainly not 7%. This was a stunner!

Stocks immediately plunged on Thursday morning following Bullard’s comments, with the S&P 500 falling over 1% and the Nasdaq down over 1.5%. You can’t see that in the chart above because the markets recovered much of those early losses by the end of the day. Bullard’s warning that the Fed Funds rate might have to go as high as 7% was largely discounted.

Bullard Is Outspoken, But Does He Have A Point?

As noted above, James Bullard is the President of the St. Louis Fed. He is also a voting member on the Fed Open Market Committee which sets monetary policy. Jim is perhaps the most outspoken member of the FOMC, and he never hesitates to let his views be known, even if it riles the markets from time to time.

No one at the Fed, other than Jim, has suggested the Fed Funds rate might have to go as high as 7%. Several other members of the FOMC were specifically asked about it on Thursday, and none shared Jim’s surprising view on how high the Fed Funds rate might go in the months ahead. This fact helped the stock markets recover their big early losses last Thursday.

While I agree that Mr. Bullard was out of line to suggest the Fed Funds rate might go to 7%, he is probably correct in that it will take more rate hikes to get inflation down to the Fed’s 2% target. Let’s take a look at what several inflation measures have done this year.

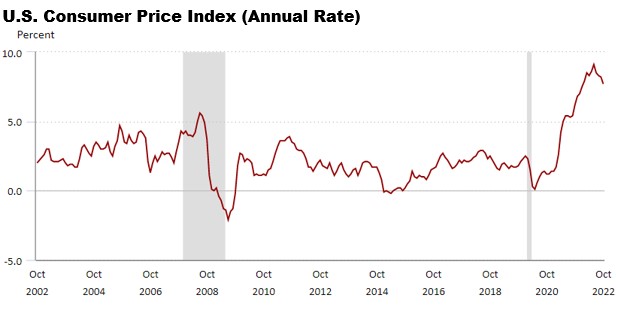

The Consumer Price Index peaked at an annual rate of 9.1% earlier this year. It has since fallen to 7.7% for October. While the decline from 9.1% to 7.7% is a welcome development, we’re still a very long way from the Fed’s CPI target of 2%. It could take a lot more rate hikes to get there.

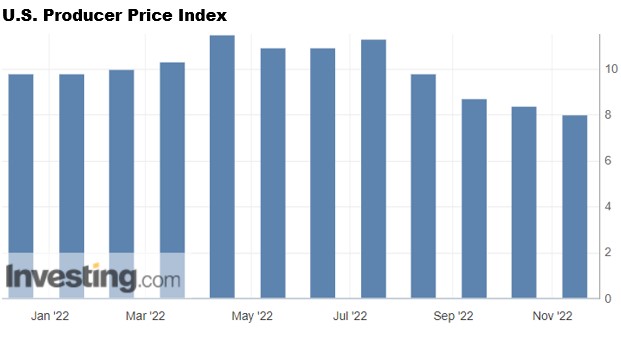

On another front, the US Producer Price Index, which is a proxy for wholesale prices, has fallen from just over 11% earlier this year to 8% today. Also,it is still a long way from the Fed’s target of 2% inflation.

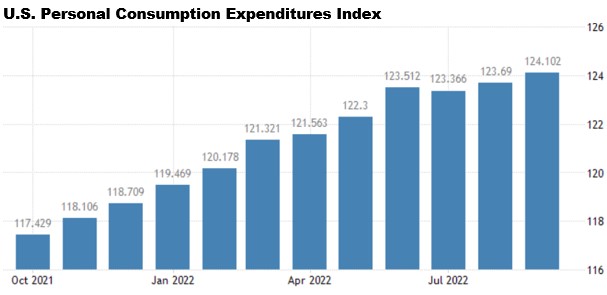

The two previous inflation indicators are the good news. Now here is the not-so-good news. The US Personal Consumption Expenditures Index (PCE), which is the Fed’s favorite indicator of inflation, has not started to fall yet, as you can see below. The Fed prefers this index because it includes more comprehensive coverage of the prices of goods and services Americans pay, and it can be revised more often than the CPI.

Since the PCE has not fallen yet, and the Fed uses it as its main inflation indicator, the Fed may have to raise interest rates more than the market is currently expecting. There was a lot of talk last week that the Fed would raise the Fed Funds rate by only 0.50% at the December 13-14 FOMC meeting and maybe stop raising rates beyond that.

I don’t believe that assumption is correct. I believe the Fed will have to raise rates more in 2023. The question is how much more. No one knows the answer to that question. Chairman Powell will hold a press conference after the FOMC meeting on December 14, and he will no doubt get questions on whether the Fed will raise rates more in 2023. I believe his answer will be yes.

I think most members of the FOMC want to see the Fed Funds rate at 4.75%-5.0% or maybe 5.0%-5.25%. Either way, that means at least one more rate hike in 2023, if not more. The financial markets are not priced for this, in my opinion.

We’ll have to see how this shakes out in the weeks ahead.

Can The Fed Pull Off Higher Rates Without A Recession?

Ever since the Fed began its rate hiking cycle, Chairman Powell and other Fed officials have repeatedly said their goal is to get inflation under control without causing a recession. Just a few weeks ago, that looked like a tall order for the Fed, since the US economy actually contracted by just over 1% in the first half of this year.

However, the Commerce Department announced that Gross Domestic Product rose at an annual rate of 2.6% in the 3Q. While this was welcome news, it was the first of three estimates of 3Q economic growth. This number could be revised higher or lower later this month and in December. So, we’ll just have to wait and see.

As I reported in my Between The Lines column last Thursday, the US Census Bureau reported earlier this month that applications to start new businesses continue to run near the highest levels in decades. I also reported that new business start-ups in the last year have been dominated by minorities, which is also very good news.

Another Way To Lower Inflation – Stop Deficit Spending

As everyone reading this knows, the US has been running annual budget deficits for years. The last budget surplus was in 2001 when Bill Clinton was president. I think most Americans are so conditioned to seeing annual budget deficits, they just view it as a normal thing.

The US budget deficit for fiscal year 2022 was $1.38 trillion following $2.8 trillion in FY 2021. The deficits have been record-large the last few years, largely due to massive COVID-19 spending to prop-up the economy and avoid a nasty recession. However, most COVID spending has ended, and the budget deficits are expected to fall significantly going forward. But the deficits will still be very large, just not in the trillions, hopefully.

However, most economists agree that if we were to balance our federal budget and eliminate budget deficits, inflation would largely disappear. I know no one talks about this anymore because, as I noted above, annual budget deficits and some level of inflation are taken for granted.

They are taken for granted because almost no one believes it would be possible to balance the budget. Most politicians want to spend more every year, and it is a given that the federal budget goes up every year. Even though the budget deficits are expected to fall, hopefully significantly in the next several years, the federal budget will continue getting larger and larger.

I just wanted to point out today that inflation would largely disappear if we were to balance our budget. While this is very unlikely to happen, I wanted to remind my clients and readers of this fact. You can read more about this option in the second link below.

Best holiday regards,

Membership required

Membership is now required to use this feature. To learn more:

View Membership BenefitsSponsored Content

Upcoming Virtual Events View All