On the Threshold of Recession

Sad to say, we think the likelihood of a recession starting in 2023 is increasing. While the Federal Reserve has not explicitly forecast a recession, the unemployment rate projected in the Fed’s quarterly Survey of Economic Projections[i] is consistent with a recession forecast.

While GDP rose in Q3 2022[1] and seems likely to rise mildly in Q4 2022, we have been seeing signs of weakness in the economic data. Recent data shows housing sector activity is plunging with sliding house prices; nonresidential construction is falling across the board; business equipment investment is slowing; exports have started to fall; consumer spending is slowing with absolute declines in durable and nondurable goods; and a situation of excess inventories is likely to lead to a period of declining inventory investment. The pace of job gains has been slowing and the unemployment rate rose in October.

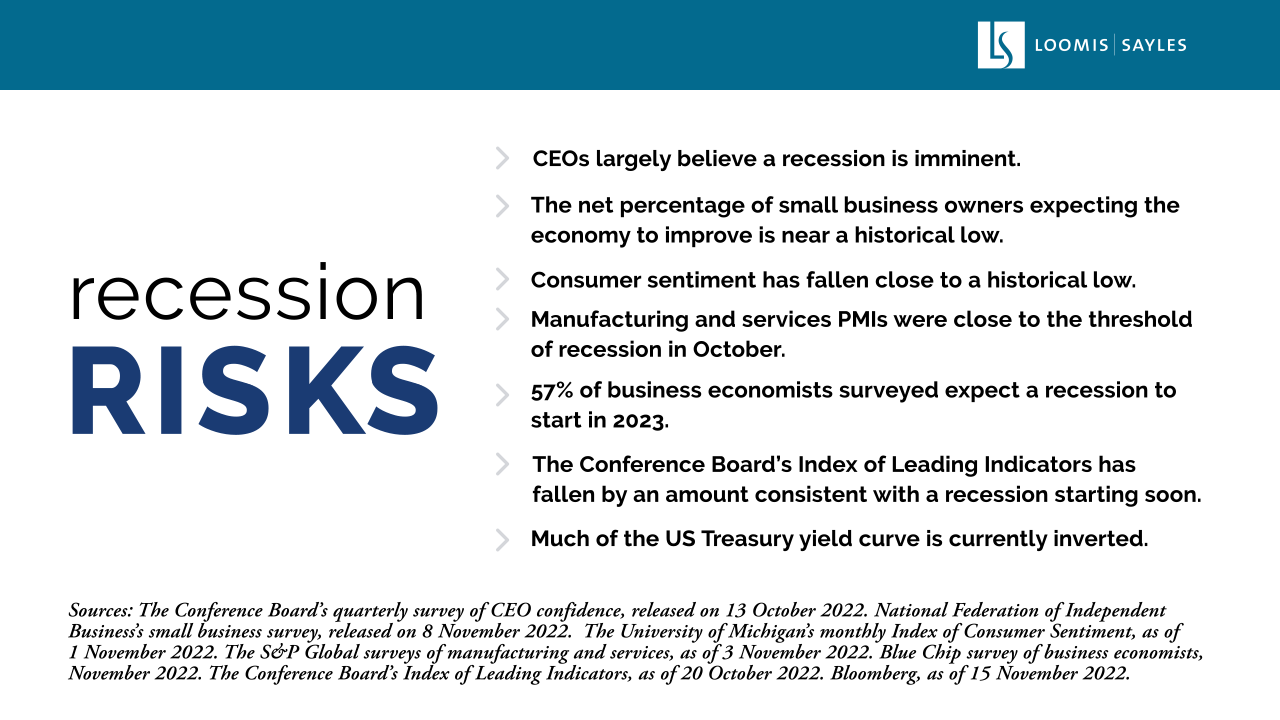

A variety of surveys and indicators have been sending a message that recession risks have risen.

We think these data could get worse as the New Year starts.

How bad could it get?

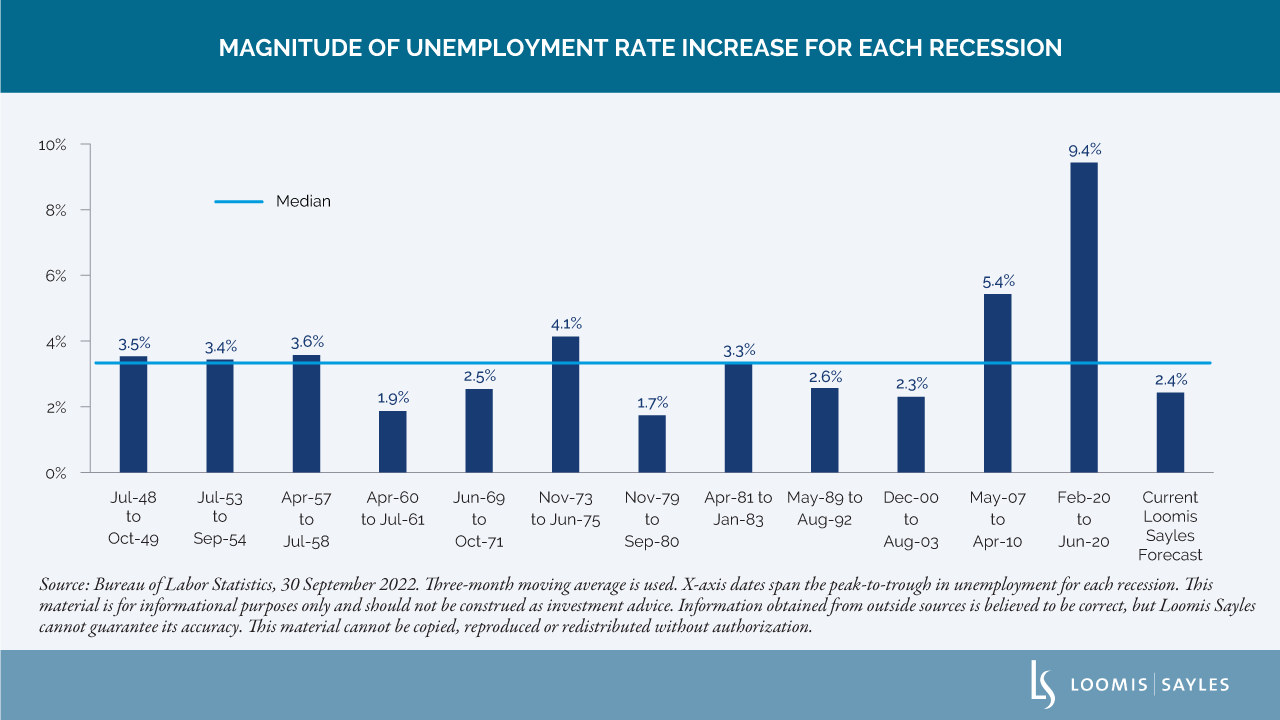

The US has had 12 recessions since 1945.[2] The two most recent—the 2007-2009 global financial crisis and the 2020 pandemic-induced downturn—were considered dramatic, traumatic and highly memorable. They were also, in many ways, atypical.

Memories of the past two recessions have investors concerned there will be another severe recession with what could be a very large rise in unemployment. As we contemplate the potential for unlucky #13, we don’t have a strong conviction on how pronounced a 2023 recession could be, but we do think it should be closer to a typical recession in terms of severity.

The chart below shows the rise in the unemployment rate associated with each recession after 1945. The 2.4% rise that we currently forecast for the recession of 2023 is in line with a typical recession during the past seven decades. The chart shows just how abnormal the last two recessions were.

It is possible that the anticipated recession could be deeper and longer than we expect. In our view, there is much that could go wrong in this troubled world. For example, the Russia-Ukraine war could escalate in ways that would put far more strain on the global economy. Or US inflation could be far more stubborn than we think, forcing the Fed to tighten even more aggressively and to hold rates higher for longer. Or a new and dangerous variant of COVID-19 could surprise us, restarting the pandemic.

But until we have data to the contrary, we think the odds currently lean toward a fairly typical recession.

How did we get here?

We think the following shocks have pushed the economy to the threshold of recession.

- The US endured its biggest surge in inflation in four decades in 2022. At the same time, federal income support from the pandemic period has faded away. The one-two punch of high inflation and lower income support eroded real household incomes and real household savings, thereby compromising household spending, which appears to be slowing.

- Commodity prices (including energy and food prices) have surged. After rising following the pandemic lockdowns ended, they were sent higher by the Russia-Ukraine war. In addition to Russia being a major exporter of oil and natural gas, both countries are major food exporters. The shocks to energy and food prices have stressed consumers around the world, including in the US but particularly in Europe and emerging economies.

- The surprise and shock from the Russian invasion of Ukraine in our view damaged consumer and business confidence, created uncertainty and contributed to global “risk off” pricing in financial markets.

- The worst of the COVID pandemic may be behind us, nearly three years after it began, but its legacy is still with us. As the economy recovered from the COVID recession, businesses found a labor shortage even as demand rose. The result was strong wage inflation, which fed into higher service-sector inflation. Major transportation bottlenecks and a compromised global supply chain also weighed on growth and helped increase prices.

- High inflation led the Fed to pivot from easy monetary policy at the start of 2022 to the most aggressive pace of tightening since Paul Volcker’s time running the Fed in the early 1980s. The fed funds rate target increased by what we consider to be a stunning 3.75 percentage points in fewer than eight months, and we believe further increases are likely. Nor did the Fed act alone; central banks throughout the world have tightened rapidly this year.

Financial conditions have turned much tighter as well as more volatile: the stock market turned bearish, the US dollar is currently the strongest since 1985, credit spreads have widened, bond yields have surged, mortgage rates have more than doubled in less than a year and banks have been tightening their lending standards on all types of loans.

Wrap-up

Recessions can be painful with lower growth and employment taking a toll across an economy. We believe this time around will be no different. As we have discussed, we believe the next downturn is likely to be more “typical” than an extreme recession.

MALR030010

Commodity, interest and derivative trading involves substantial risk of loss.

Markets are extremely fluid and change frequently.

Past market experience is no guarantee of future results.

This blog post is provided for informational purposes only and should not be construed as investment advice. Any opinions or forecasts contained herein reflect the subjective judgments and assumptions of the authors only and do not necessarily reflect the views of Loomis, Sayles & Company, L.P. This information is subject to change at any time without notice. Information obtained from outside sources is believed to be correct, but Loomis Sayles cannot guarantee its accuracy. This material cannot be copied, reproduced or redistributed without authorization

[1] Source: Bureau for Economic Analysis, 27 October 2022

[2] Source: National Bureau of Economic Research

[i] Federal Open Market Committee, Summary of Economic Projections, 21 September 2022.

© Loomis, Sayles & Co.

Read more commentaries by Loomis, Sayles & Co.