Doug Drabik discusses fixed income market conditions and offers insight for bond investors.

Different tools allow you to perform an undertaking easier than others. You may be able to dig a hole in the garden with a screwdriver, but it is a whole lot easier, more effective and result-driven with a hand shovel. Using the right investment tools is equally important to reaching long term financial security. Recent economic and market activity has made this clear. Let’s toss the cheesy metaphor aside and talk reality. Conceptually it is easy to understand - yet fear and greed often impede implementation. Perhaps we can appeal to those natural impediments and use them to your advantage.

Over the previous few years when interest rates were low, we emphasized the importance of staying true to appropriate asset allocation. Growth assets and protective assets are not exchangeable no matter how much we try to convince ourselves otherwise. When interest rates were low, the desire for more return pushed some investors to substitute growth assets (such as stocks) to replace fixed income which lacked attractive yields. What was sacrificed was the primary goal of fixed income assets: protection of principal. This natural tendency to seek better return eventually failed to protect principal as the stock market has dropped over 16% year-to-date. This risk and swing may be an accepted risk for growth assets but not typically acceptable for protective assets.

The tendency is to point out that fixed income asset prices have also fallen and created losses. This is where having or using the right tool comes to play. Funds comprised of bonds are very different products simply because they do not have stated maturities. Individual bonds have stated maturities so the holder has the choice to retain them until they mature. This is a key feature that provides an opportunity to disregard interim holding period price movements. By holding a bond to maturity, an investor is locked into its cash flow, income and point in time (maturity) when the face value is returned. Only two things can alter this for an individual bond: 1) an outright default (which is a minimized risk when buying high quality investment grade bonds) or selling the bond prior to maturity which would activate the market price at the time of sale (could be higher or lower but will affect return).

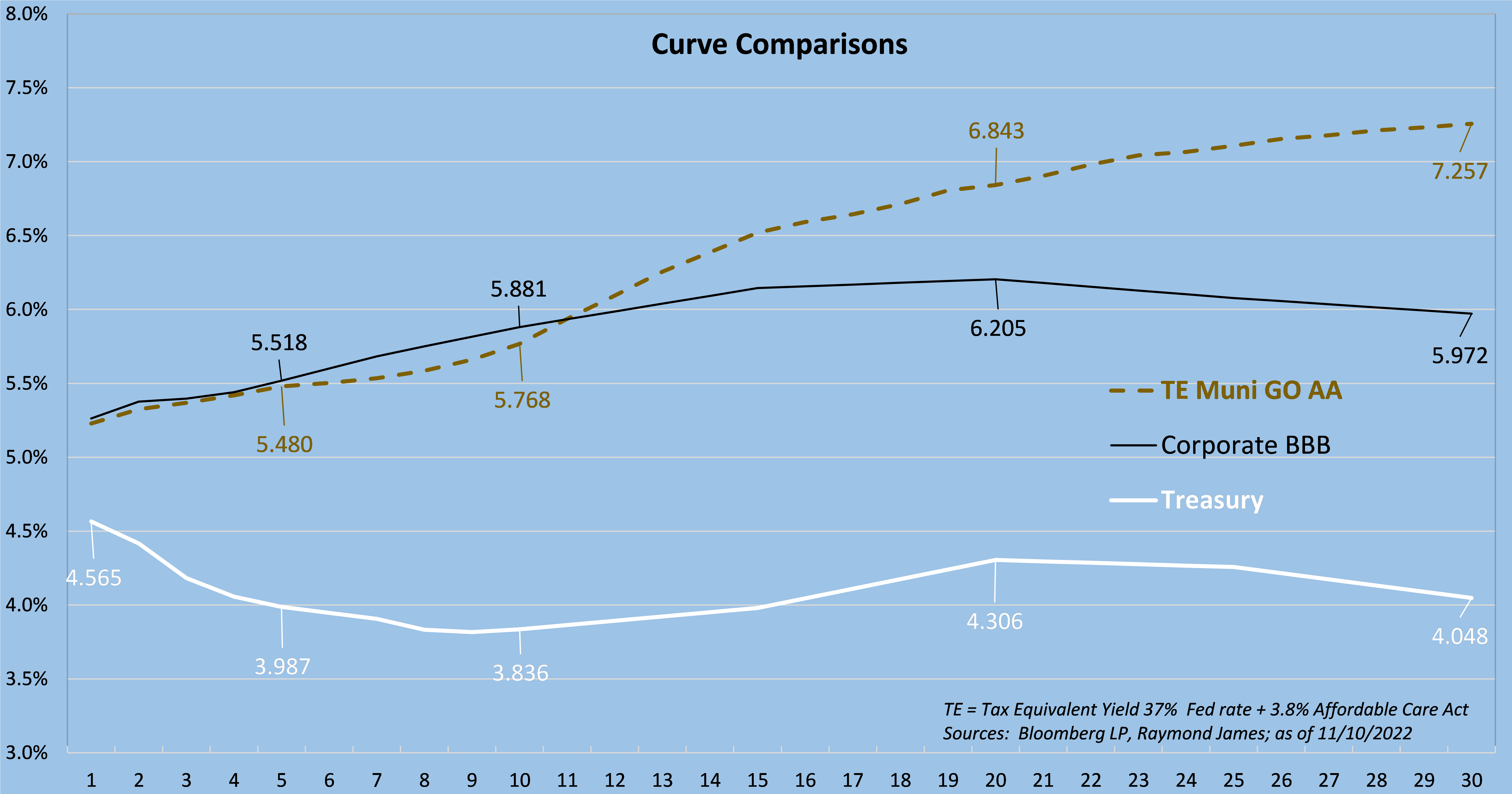

Today, yields are much higher than they have been in years. Resist the temptation to substitute asset allocation in reverse. In other words, growth assets over time should outperform and provide necessary growth of principal. Individual bonds will still provide the primary purpose of protecting principal; however, they now can provide very attractive income benefits. The following graph provides a clear picture of how individual bonds can provide: 1) principal protection; and 2) productive yields for periods investors can define by maturity and product choice. Treasury yields (white line) are attractive. Corporate (black line) and municipal (dashed line) yields are providing even higher rates. Locking into yield and maturity (extending out on the curve) may benefit investors inclined to expand today’s advantage into the future. Choosing individual bonds may provide multiple plusses.