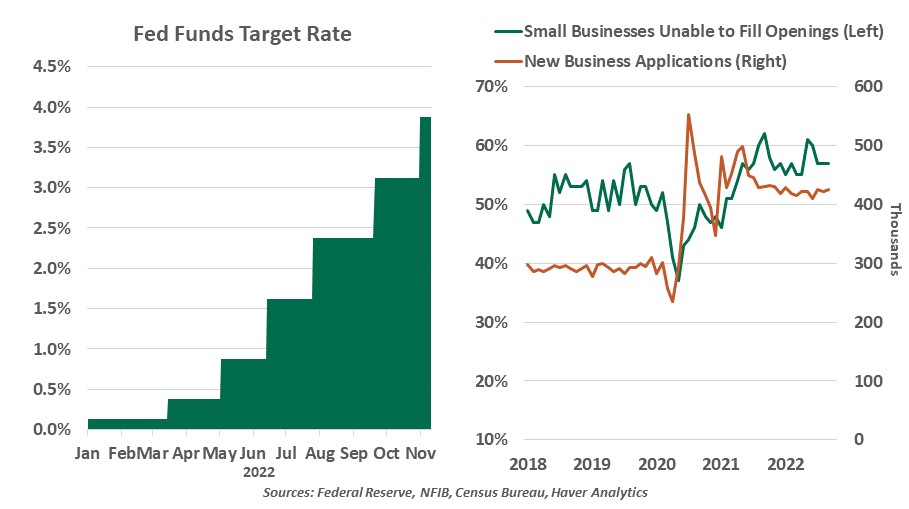

This week, the Federal Open Market Committee (FOMC) delivered another significant rate hike, lifting the Fed Funds Rate by 75 basis points to a range of 3.75%-4.00%. The move was well-signaled, and the meeting was closely watched for any signs that the Fed might soon pivot from this rapid pace of tightening.

Before the meeting, rumors spread that Fed governors were ready to slow down. The FOMC statement opened the door to that path with a new sentence: “In determining the pace of future increases in the target range, the Committee will take into account the cumulative tightening of monetary policy, the lags with which monetary policy affects economic activity and inflation, and economic and financial developments.”

In effect, the FOMC admitted this year’s substantial tightening has not yet shown results. Inflation remains high, and labor markets have scarcely cooled. By emphasizing cumulative tightening and lagged effects, the FOMC set the stage for a more patient posture, allowing themselves time to watch how markets work through tighter conditions.

But this was no dovish meeting. In his press conference, Fed Chair Jerome Powell repeated that it is “premature” to consider pausing hikes. Significantly, he also mentioned that interest rates may need to move higher than was expected as of the September meeting. This upset the relative certainty provided by the September dot plot, which showed consensus that rates would not exceed 5%. We have adjusted our expectations for the Fed upward on the basis of Powell’s remarks.

The Fed Chair also reiterated his view that the risk of too much tightening is less than the risk of doing too little. If the FOMC pushes rates too high, they can then loosen policy; if they move too slowly, they may find it difficult to halt the course of entrenched inflation. In sum, slower tightening is still tightening, and this hiking cycle is not complete.

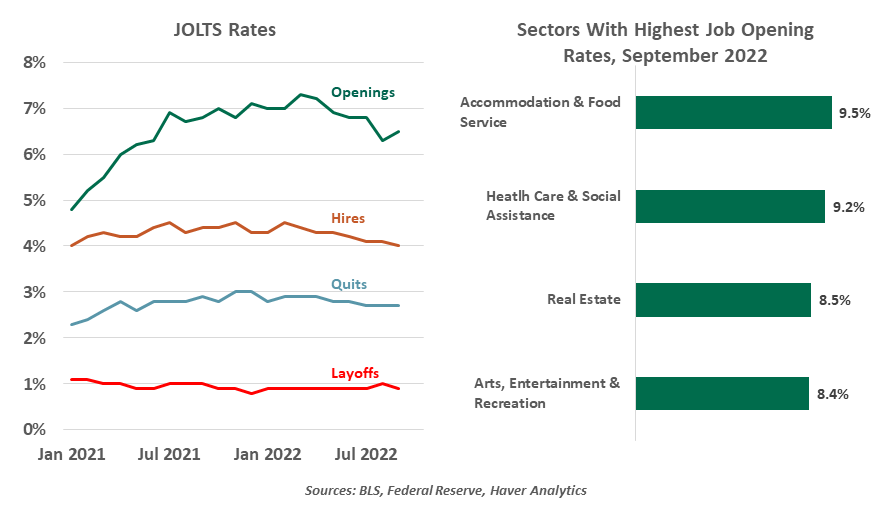

The Fed’s turn away from a pivot was not the only about-face in this week’s economic news. The Bureau of Labor Statistics reported the results of its Job Openings and Labor Turnover Survey (JOLTS) for September. The report called into question the early evidence of a softening labor market. The August reading showed a surprising decline of over one million jobs available from a month before; September’s reading revised up the August estimate, and then showed further growth to 10.7 million openings.

|

The Fed will continue raising rates, in smaller increments.

|

JOLTS measurements have been frequently cited in the Fed’s communications. The increased attention to this source calls for a closer look into this data and its limitations. JOLTS is a monthly survey of labor activity: openings, hires, quits and involuntary termination are presented, both in absolute levels and rates (the ratio of each activity to the total number of jobs).

Job openings can be thought of as a measure of labor market imbalance. A high rate of openings indicates excess labor demand, just as a high unemployment rate suggests excess labor supply. Low unemployment and steady openings reflect equilibrium, as was seen before the pandemic.

The JOLTS series is relatively new. Whereas most modern economic measurements can trace their histories to at least the 1950s, JOLTS only launched in 2001. Analysts therefore have less of a base of comparison when digesting the information. Unfortunately, we cannot see how today’s job market compares to the maximum-employment market of the 1990s; perhaps today’s record high job openings would not be as impressive.

The JOLTS polls 20,700 business and government establishments, stratified by region, sector and size. While statistically representative, even the best sampling may not reflect the full population. The JOLTS methodology will not immediately include new businesses, which have been formed at a faster pace since the COVID shutdowns. If new hiring or job losses are concentrated in new firms, they are likely being overlooked.

Job openings could also be estimated by looking at job boards. But while the trends of job postings are informative, these counts can be misleading. Employers are likely to post vacancies on multiple sites, so adding across platforms would double-count them. Surveying establishments directly gets around this challenge.

When employers respond to the JOLTS inquiry, they must report true opportunities for hiring. By the BLS’ definition, these must be vacancies for which work could start within 30 days, and the employer is actively recruiting to fill the position. Jobs are not counted if they will be filled with temporary workers or are projected to start more than a month in the future, like staffing up for new projects or seasonal hires. But the count does not capture intentions: stale positions can be left open even after companies adapt to working with that role vacant, or listings may be “fishing” for exceptional candidates. The count is not only volatile, but is potentially overstated.

|

Elevated openings show that demand for labor exceeds supply.

|

Well before the Fed took up its current challenge of fighting inflation, the central bank had committed to being more data dependent. When setting policy, they committed to looking first at actual results rather than relying on models and projections. But between persistent high inflation and the labor market maintaining its strength, evidence of the effects of tighter policy has been scarce. The shift to acknowledging the lagged effects of policy provides some hope that an overcorrection can be avoided.

The Fed’s effort to engineer a soft landing was never going to be easy. The swings in the JOLTS figures illustrate the underlying difficulty: Every data point matters, but one encouraging data print does not always mean a trend has changed. In total, this week’s news jolted us toward expecting monetary policy to grow even tighter.

Information is not intended to be and should not be construed as an offer, solicitation or recommendation with respect to any transaction and should not be treated as legal advice, investment advice or tax advice. Under no circumstances should you rely upon this information as a substitute for obtaining specific legal or tax advice from your own professional legal or tax advisors. Information is subject to change based on market or other conditions and is not intended to influence your investment decisions.

© 2022 Northern Trust Corporation. Head Office: 50 South La Salle Street, Chicago, Illinois 60603 U.S.A. Incorporated with limited liability in the U.S. Products and services provided by subsidiaries of Northern Trust Corporation may vary in different markets and are offered in accordance with local regulation. For legal and regulatory information about individual market offices, visit northerntrust.com/terms-and-conditions.

© Northern Trust

Read more commentaries by Northern Trust