The U.S. higher education system has much to its credit, from countless academic breakthroughs to equipping millions of students with the skills to advance their stations in life. But along the way, it has developed an unsound and unworkable means of financing. The Biden administration’s recent announcement of partial debt forgiveness only served to reinforce how difficult the challenge of reforming education finance will be.

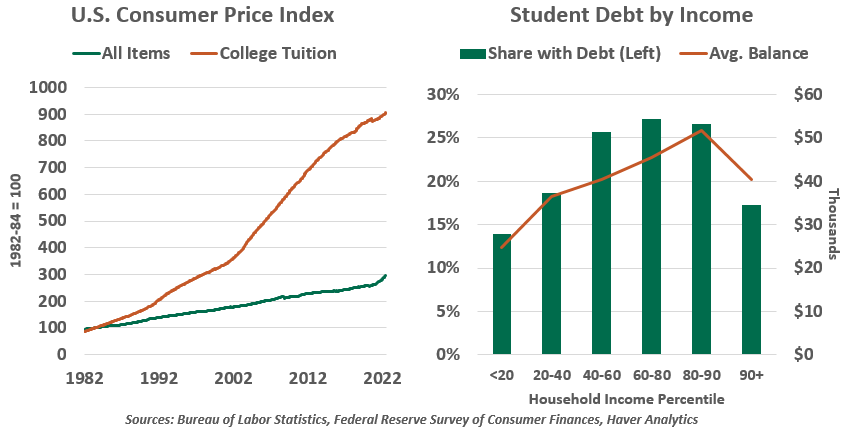

The high cost of higher education has been well-covered across many outlets. Since the early 1980s, college tuition has increased at triple the overall rate of inflation. Working one’s way through college is increasingly out of reach for most students, and taking out loans is routine. Student debt averages $37,113 per borrower; new graduates start their working lives with an average monthly payment due of $391.

Obtaining a degree is still a worthy investment for most students. Holders of a college degree enjoy lower unemployment rates and wage premiums that accumulate to $450,000 over the course of a career—certainly enough to justify taking on a loan. This opportunity for upward mobility should be available to all, and student loans make it possible.

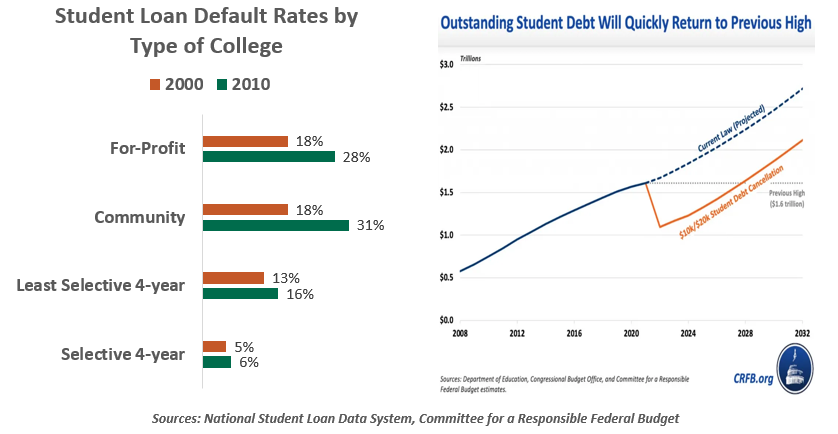

But not everyone graduates. A 2016 Department of Education study found that three years after enrollment, 44% of students at two-year colleges and 20% of freshmen at four-year colleges had dropped out. They paid tuition but realized no upside for employment or earnings; these are the borrowers most likely to default on their loans.

Student loans are unique among consumer debts. Most involve no underwriting: students are eligible to borrow simply by enrolling in courses. With no ability to assess or price a borrower’s risk, private lenders have little interest in this market, leaving the federal government as the dominant lender. If the borrower does not repay, the debt is never written off. It cannot be discharged in bankruptcy; borrowers who fall behind, or never make any payments, will find their credit record impaired indefinitely. This limits their ability to take certain jobs, rent apartments and make other major purchases.

With education in high demand and loans freely available, student debt has grown immensely. Debt outstanding has reached $1.6 trillion, the largest class of U.S. consumer credit after mortgages. So much debt has distortive effects on the economy. Graduates may defer life events like owning a home or starting a family until they pay down their student loans. Meanwhile, universities enjoy an implicit subsidy that enables steady tuition inflation, and which does not require them to demonstrate results.

The Biden administration jumped into this complex fray with support for a subset of student loan holders. Borrowers with incomes less than $125,000 (doubled for married households) will see $10,000 of their loan principal forgiven (or $20,000 for lower-income Pell grant recipients).

|

Does debt forgiveness favor those who least need support?

|

Criticisms of the plan abound: Those who chose a lower-cost option or who responsibly repaid their loans feel slighted; why reward those who borrowed the most? Forgiveness undermines the contractual agreement of taking on debt. The estimated cost of $500 billion is hard to justify against other fiscal priorities and negates recent progress toward deficit reduction. Legality remains an open question; this sort of relief has little precedent, and recent high court decisions have skewed toward limiting executive authority.

Worries have also arisen that this support for consumers will add to inflationary pressures, but we are skeptical. Federal loan payments have been suspended since March 2020 (for all borrowers, regardless of income). Biden’s announcement made it clear this last vestige of COVID relief will expire at the end of the year. Resuming payments will be a shock to borrowers, reducing their capacity for other purchases and lowering inflation.

Critics should not overlook the material help conveyed to millions of struggling consumers, most of whom are not well-paid college graduates. Up to 20 million borrowers will see their debt fully eliminated. Hundreds of thousands of borrowers are projected to move from negative to positive net worth with this one measure. Those who benefit the most will be those who cannot afford to repay a loan of $20,000 or less—certainly not high earners.

The administration’s plan also contains a provision to make income-based repayment (IBR) simpler and more widely available, with no more than 5% of a borrower’s income to be used to repay undergraduate loans. IBR programs exist today in the U.S. but place a high burden on the borrower to qualify and apply.

|

There is no simple reform for higher education costs.

|

Our primary concern with the proposal is that it offers no cure for the fundamental problems facing higher education. Institutions still have an incentive to recruit as many students and charge as high a tuition as possible. The Committee for a Responsible Federal Budget estimates the measure will be a brief blip on the ever-growing ledger of student debt, returning to today’s level in six years. Expanding IBR will make students less sensitive to the cost of tuition; if a loan will never claim more than 5% of future income, then the size of the principal becomes irrelevant to the borrower.

A more comprehensive reform would put more onus on the students, institutions and employers to pursue better outcomes. Some penalty for institutions turning out students unable to pay could lead to more rigorous vetting of applications and counseling for students. A cultural emphasis on attaining a degree has inflated college demand, while important technical roles like trades and manufacturing struggle to fill vacancies. Employers may find greater success by recruiting more applicants without degrees and offering more on-the-job training.

The jubilee has not yet begun. The administration has not released implementation details, and loan servicers have not reduced any balances yet. And though it is far from a durable solution, this proposal will offer one lasting benefit to educators: a new mainstay of case studies in public policy programs, sure to spark lively conversations for generations to come.

Information is not intended to be and should not be construed as an offer, solicitation or recommendation with respect to any transaction and should not be treated as legal advice, investment advice or tax advice. Under no circumstances should you rely upon this information as a substitute for obtaining specific legal or tax advice from your own professional legal or tax advisors. Information is subject to change based on market or other conditions and is not intended to influence your investment decisions.

© 2022 Northern Trust Corporation. Head Office: 50 South La Salle Street, Chicago, Illinois 60603 U.S.A. Incorporated with limited liability in the U.S. Products and services provided by subsidiaries of Northern Trust Corporation may vary in different markets and are offered in accordance with local regulation. For legal and regulatory information about individual market offices, visit northerntrust.com/terms-and-conditions.

© Northern Trust

Read more commentaries by Northern Trust