As we expected, Consumer Price Index (CPI) inflation began to moderate in July with the downturn in commodity prices, supply side improvements, and signs of demand destruction in the broader economy. There is still ground to cover to get closer to the Federal Reserve’s (Fed) target, but we expect these trends to continue, which should help support the long end of the yield curve.

Both headline and core CPI cooled in July, with headline CPI down 0.2 percent annualized over the month, and core prices rising at a 3.8 percent annualized monthly pace. Falling energy prices drove most of the outright decline in headline CPI, with gasoline prices down 7.7 percent unannualized over the month. Notably, airfares, hotels, and used vehicles also declined. The continued decline in energy prices and high frequency data suggesting more deflation in airfares and used car prices in August should drive another low headline number next month.

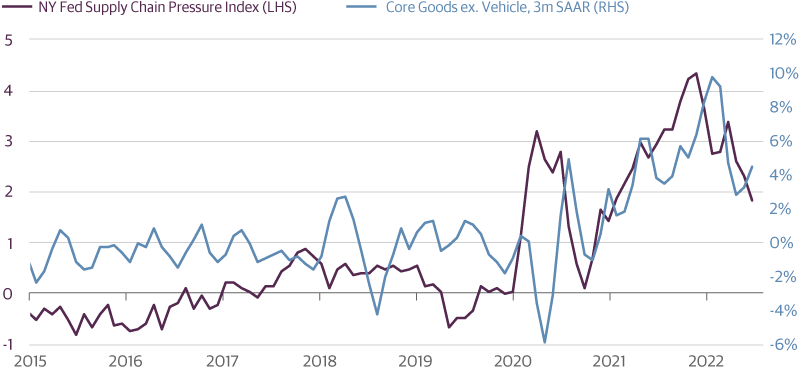

Lower inflation was also driven by a broad-based sequential deceleration in core goods inflation excluding vehicles, which moderated to 3.7 percent annualized after rising 7.1 percent in June. Continued supply chain improvement and lower import prices should continue to drive disinflation in this category.

Easing Supply Chain Stress is Helping Goods Inflation Cool

Source: Guggenheim Investments, Bloomberg, Haver Analytics. Data as of 07/31/2022.

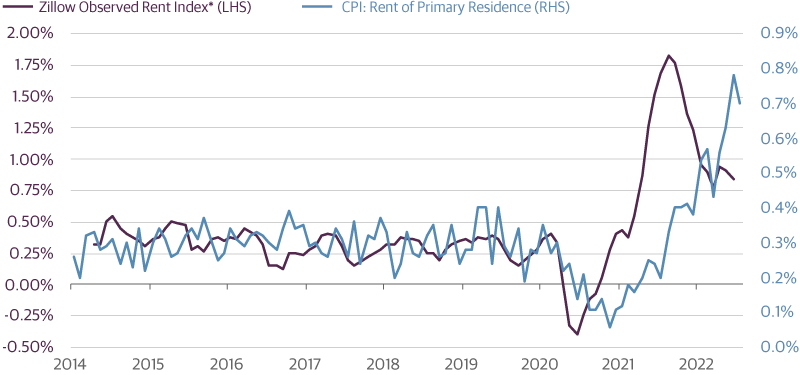

An even more important sign for the medium-term outlook was the moderation in core services inflation. Rent inflation remains red hot but cooled down a bit with rent declining from 9.7 percent annualized to 8.8 percent and owners’ equivalent rent down from 8.7 percent to 7.9 percent. These two categories alone are still contributing 2.5 percentage points to headline CPI so need to slow much more, but more timely measures of market rents (such as Zillow and Apartment List data) point to more moderation in the months ahead. Recent business surveys such as the ISM Services index also point to more slowing in services inflation.

Slowdown in Market Rents Suggest Moderation in Shelter CPI Inflation

Month-Over-Month % Change

Source: Guggenheim Investments, Haver Analytics. Data as of 07/31/2022. *Note: seasonally adjusted and smoothed by Guggenheim.

Reaching the Fed’s inflation target won’t happen without wage growth cooling substantially, and the recent data on that front is not as encouraging (e.g., Employment Cost Index, unit labor costs, average hourly earnings). So while the new CPI report will ease fears about runaway inflation, the Fed will still see a need for substantially more tightening until more labor market weakness emerges.

From the Office of the Global Chief Investment Officer of Guggenheim Partners, Scott Minerd

By the Macroeconomic and Investment Research Group

- Matt Bush, CFA, CBE, U.S. Economist, Macroeconomic and Investment Research

Important Notices and Disclosures

Investing involves risk, including the possible loss of principal. Stock markets can be volatile. Investments in securities of small and medium capitalization companies may involve greater risk of loss and more abrupt fluctuations in market price than investments in larger companies. Investments in fixed-income instruments are subject to the possibility that interest rates could rise, causing their values to decline. High yield and unrated debt securities are at a greater risk of default than investment grade bonds and may be less liquid, which may increase volatility. Investors in asset-backed securities, including mortgage-backed securities and collateralized loan obligations (“CLOs”), generally receive payments that are part interest and part return of principal. These payments may vary based on the rate loans are repaid. Some asset-backed securities may have structures that make their reaction to interest rates and other factors difficult to predict, making their prices volatile and they are subject to liquidity and valuation risk. CLOs bear similar risks to investing in loans directly, such as credit, interest rate, counterparty, prepayment, liquidity, and valuation risks. Loans are often below investment grade, may be unrated, and typically offer a fixed or floating interest rate.

This material is distributed or presented for informational or educational purposes only and should not be considered a recommendation of any particular security, strategy or investment product, or as investing advice of any kind. This material is not provided in a fiduciary capacity, may not be relied upon for or in connection with the making of investment decisions, and does not constitute a solicitation of an offer to buy or sell securities. The content contained herein is not intended to be and should not be construed as legal or tax advice and/or a legal opinion. Always consult a financial, tax and/or legal professional regarding your specific situation.

This material contains opinions of the author, but not necessarily those of Guggenheim Partners or its subsidiaries. The opinions contained herein are subject to change without notice. Forward-looking statements, estimates, and certain information contained herein are based upon proprietary and non-proprietary research and other sources. Information contained herein has been obtained from sources believed to be reliable, but are not assured as to accuracy. No part of this material may be reproduced or referred to in any form, without express written permission of Guggenheim Partners, LLC. There is neither representation nor warranty as to the current accuracy of, nor liability for, decisions based on such information. Past performance is not indicative of future results.

Guggenheim Investments represents the following affiliated investment management businesses of Guggenheim Partners, LLC: Guggenheim Partners Investment Management, LLC, Security Investors, LLC, Guggenheim Funds Distributors, LLC, Guggenheim Funds Investment Advisors, LLC, Guggenheim Partners Advisors, LLC, Guggenheim Corporate Funding, LLC, Guggenheim Partners Europe Limited, Guggenheim Partners Japan Limited, GS GAMMA Advisors, LLC, and Guggenheim Partners India Management.

© 2022 Guggenheim Partners, LLC. All rights reserved.

GPIM 53753

© Guggenheim Investments

Read more commentaries by Guggenheim Investments