Summer at work brings some of my favorite meeting requests: Interns asking to learn more about my role and career journey. I was once an intern, too, and I’m happy to provide mentorship. But as I retell my story lately, I notice one detail that I had never dwelled on before: the entirety of my professional and academic progress has played out in a radius of about one mile, in and around the Chicago Loop. Working at home during the pandemic was a brief hiatus.

Now, I am commuting downtown again, but not five days a week. Many others have not returned at all. Without the same corps of office workers, will central business districts return to their former glory?

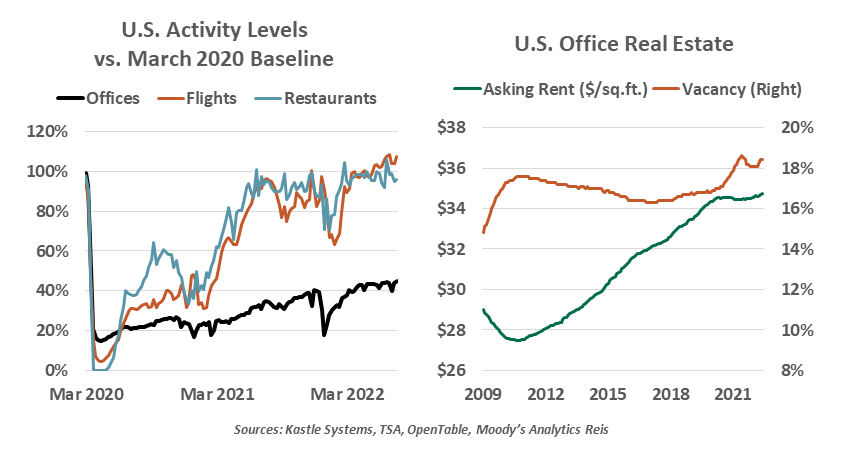

Speculation about reopening led headlines in 2020, and actual reopening made 2021 a boom year. But return-to-office plans encountered many obstacles as new COVID-19 variants raised fear of contagion. After the Omicron surge to start the year, most forms of activity have settled into steady patterns. But while leisure destinations have recovered to their pre-pandemic levels, offices are a far cry from their old levels of activity. This year, we are going everywhere but the office.

Two years of working from home demonstrated that business can carry on with a dispersed workforce. And the benefits of remote work are significant: employees can achieve a better work-life balance by gaining some flexibility over their work hours and reclaiming their commute time. Indeed, commutes are a key differentiator between metropolitan areas where workers are more hesitant to return to office full-time and those where offices are back to their old normal.

Fully in-person professional jobs are no longer the norm. Fully remote roles have gone from niche to more common. In between, for most office workers, hybrid schedules present an optimal balance between personal productivity and interpersonal interaction. But is a part-time in-person workforce sufficient to sustain a commercial district?

At one extreme, in New York City alone, researchers at Columbia and New York Universities estimated a $500 billion “apocalypse” of office real estate value, assuming occupancy stays at the diminished levels seen through 2021. In such a scenario, not only will property investors and lenders incur financial losses, but the restaurants and other ancillary businesses that catered to nearby workers will fail. Leaders from New York to London to Melbourne are pushing for a more complete return to office to support their local economies.

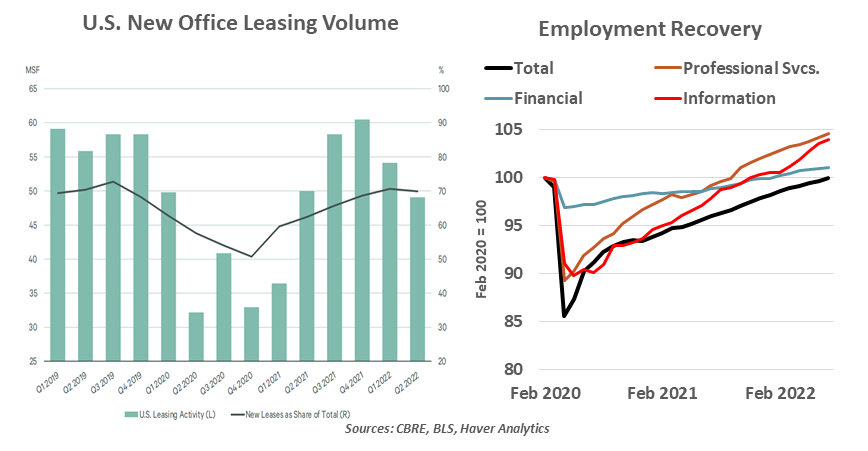

Despite these worries, commercial real estate (CRE) markets for office spaces have not entered a correction. Defaults on bank CRE loans and delinquencies on commercial mortgage-backed securities have not yet risen. Office leases can have terms of up to ten years; many of today’s occupied offices predate the pandemic. The employers who signed those leases maintained their cash flows, allowing them to keep making their lease payments, even as their space is no longer utilized as it once was. A retrospective by Moody’s found the downturn in major U.S. office markets is benign compared to past economic cycles.

Key metrics to gauge the health of the office CRE market are vacancies, rents and capitalization rates (or “cap rates,” the ratio of a property’s income to its market value). Vacancies can result from tenants leaving or downsizing their leased space; CBRE noted that vacancies edged to a new pandemic-era high in the second quarter as more new construction was completed without enough new tenants to occupy it.

|

Hybrid work is causing an adaptation of office spaces.

|

To attract and retain tenants, property managers will need to compete on rents, and rent growth has stopped. Through the first half of 2022, data from Moody’s shows asking rents have held steady throughout the pandemic era, despite high inflation throughout the economy. Higher vacancies and lower rents will weigh on valuations and cap rates, a key consideration for future investments in the sector. Subletting is also on the rise; CBRE estimates sublease availability grew from 2.5% of leases to 4% since the pandemic began. Current tenants offloading their space, often at a discount, is another competitive force on rents.

Real estate remains valuable, even if offices are no longer its highest and best use. Though at no small cost, office buildings can be converted to other purposes, like residential spaces. Dense cities offer a variety of lifestyle amenities beyond just living near the office, and apartment vacancy rates are holding low in most markets.

Calling for the downfall of the office CRE market would be premature. Companies still need headquarters, especially those that have any form of in-person contact with clients. Live interaction with coworkers enables knowledge sharing, builds relationships and reinforces culture. Earlier-career employees benefit the most from these interactions; employer review firm Glassdoor found that interns were generally dissatisfied with remote work experiences, as they missed so many valuable opportunities to connect. Offices may not be used for heads-down, nine-to-five work as much as they once were, but they will still be used.

|

Long lease terms mean the office real estate cycle will play out for several years ahead.

|

The details of the labor recovery offer another hint. While much attention has been paid to the incomplete recovery in the service sector, professional and financial payrolls have exceeded their pre-pandemic levels. The need for office workers is as strong as ever, supporting demand for physical space.

We now understand that professional jobs can be done anywhere. But we are more than our résumés: The coffees, lunches, happy hours, offsites and late nights were essential to our growth. Central business districts have been the background to countless successful career journeys. Office demand will endure an adjustment for many years to come, but their story is far from finished.

Information is not intended to be and should not be construed as an offer, solicitation or recommendation with respect to any transaction and should not be treated as legal advice, investment advice or tax advice. Under no circumstances should you rely upon this information as a substitute for obtaining specific legal or tax advice from your own professional legal or tax advisors. Information is subject to change based on market or other conditions and is not intended to influence your investment decisions.

© 2022 Northern Trust Corporation. Head Office: 50 South La Salle Street, Chicago, Illinois 60603 U.S.A. Incorporated with limited liability in the U.S. Products and services provided by subsidiaries of Northern Trust Corporation may vary in different markets and are offered in accordance with local regulation. For legal and regulatory information about individual market offices, visit northerntrust.com/terms-and-conditions.

© Northern Trust

Read more commentaries by Northern Trust