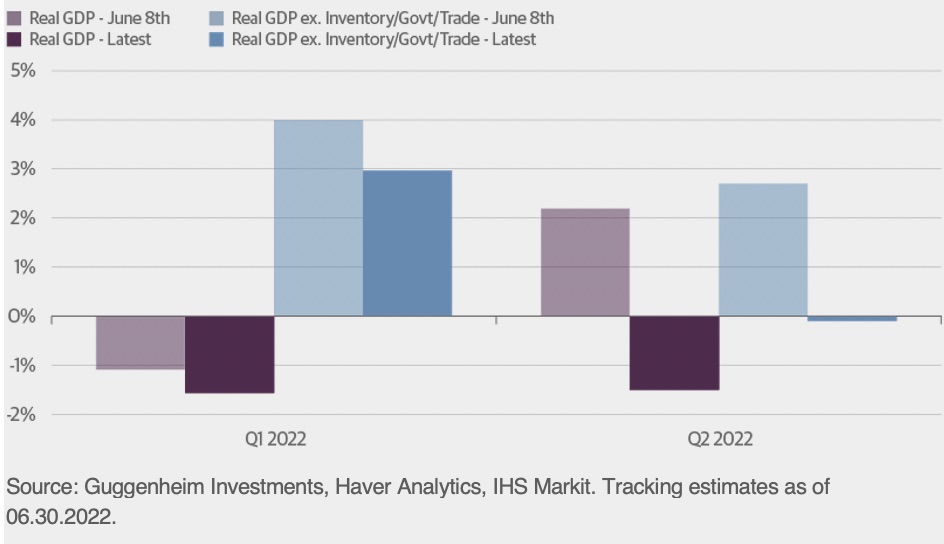

The outlook for gross domestic product (GDP) growth has weakened considerably over the past few weeks. The negative first quarter real GDP figure initially looked to be largely reflective of temporary drags from trade and inventories, but the recent revision showed a less robust gain in GDP excluding these categories (from 4 percent to 3 percent). Additionally, recent data releases, most notably this morning’s personal consumption numbers, mean that second quarter real GDP is now tracking negative. Domestic demand has slowed considerably, as tracking for real GDP excluding inventories, government, and trade has fallen from 2.7 percent a few weeks ago to -0.1 percent in the latest estimate. These developments raise the risk of two straight quarters of negative real GDP growth, which is conventionally regarded as the definition of recession.

Economic Growth Picture Has Deteriorated in Just a Few Weeks

Real GDP Tracking, QoQ% Annualized Changes

The GDP figures are not the only area of concern. The more forward-looking Leading Economic Index (LEI) has declined for the last three months through May, and there is a high likelihood that June will also be negative based on the drop in stock prices, a flatter yield curve, rising jobless claims, and falling consumer expectations. Historically, four consecutive monthly declines in the LEI have always foretold a recession.

Four Negative Months of Leading Indicators Has Reliably Signalled Recession

Consecutive Negative MoM% Readings for the Leading Economic Index

While the National Bureau of Economic Research—the official arbiter of recession dating—probably won’t make it official yet, and other economic drivers such as employment are still expanding, the negative signals from the GDP and LEI data show economic momentum is fading quickly even as the Fed continues its plan to aggressively hike rates. This dynamic of tightening into an economic slowdown explains the ongoing decline in long term interest rates, a decline that will continue as it becomes clearer that a recession is not far away, if it has not already begun.

From the Office of the Global Chief Investment Officer of Guggenheim Partners, Scott Minerd By the Macroeconomic and Investment Research Group

- Matt Bush, CFA, CBE, U.S. Economist, Macroeconomic and Investment Research

Important Notices and Disclosures

Investing involves risk, including the possible loss of principal. Stock markets can be volatile. Investments in securities of small and medium capitalization companies may involve greater risk of loss and more abrupt fluctuations in market price than investments in larger companies. Investments in fixed-income instruments are subject to the possibility that interest rates could rise, causing their values to decline. High yield and unrated debt securities are at a greater risk of default than investment grade bonds and may be less liquid, which may increase volatility. Investors in asset-backed securities, including mortgage-backed securities and collateralized loan obligations (“CLOs”), generally receive payments that are part interest and part return of principal. These payments may vary based on the rate loans are repaid. Some asset-backed securities may have structures that make their reaction to interest rates and other factors difficult to predict, making their prices volatile and they are subject to liquidity and valuation risk. CLOs bear similar risks to investing in loans directly, such as credit, interest rate, counterparty, prepayment, liquidity, and valuation risks. Loans are often below investment grade, may be unrated, and typically offer a fixed or floating interest rate.

This material is distributed or presented for informational or educational purposes only and should not be considered a recommendation of any particular security, strategy or investment product, or as investing advice of any kind. This material is not provided in a fiduciary capacity, may not be relied upon for or in connection with the making of investment decisions, and does not constitute a solicitation of an offer to buy or sell securities. The content contained herein is not intended to be and should not be construed as legal or tax advice and/or a legal opinion. Always consult a financial, tax and/or legal professional regarding your specific situation.

This material contains opinions of the author, but not necessarily those of Guggenheim Partners or its subsidiaries. The opinions contained herein are subject to change without notice. Forward looking statements, estimates, and certain information contained herein are based upon proprietary and non-proprietary research and other sources. Information contained herein has been obtained from sources believed to be reliable, but are not assured as to accuracy. No part of this material may be reproduced or referred to in any form, without express written permission of Guggenheim Partners, LLC. There is neither representation nor warranty as to the current accuracy of, nor liability for, decisions based on such information. Past performance is not indicative of future results.

Guggenheim Investments represents the following affiliated investment management businesses of Guggenheim Partners, LLC: Guggenheim Partners Investment Management, LLC, Security Investors, LLC, Guggenheim Funds Distributors, LLC, Guggenheim Funds Investment Advisors, LLC, Guggenheim Partners Advisors, LLC, Guggenheim Corporate Funding, LLC, Guggenheim Partners Europe Limited, Guggenheim Partners Fund Management (Europe) Limited, Guggenheim Partners Japan Limited, GS GAMMA Advisors, LLC, and Guggenheim Partners India Management.

© 2022 Guggenheim Partners, LLC. All rights reserved.

GPIM 53177

© Guggenheim Investments

Read more commentaries by Guggenheim Investments