If two trains are heading towards each other at different speeds, when will they collide?

This grade school arithmetic problem is playing out in the Federal Reserve’s (Fed) execution of monetary policy. In this case, one train is the aggressive tightening plan as telegraphed by the Fed and the other is the U.S. economy which, while still strong, is showing a few signs of cooling. Investors want to know when the collision—a recession—will occur.

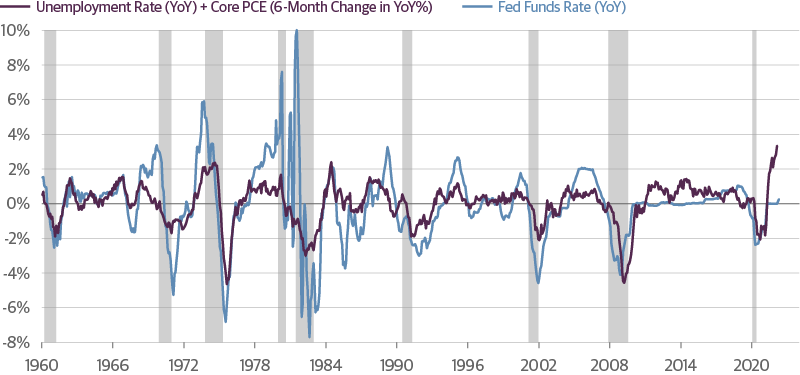

The Fed’s dual mandate calls for full employment and price stability. Historically, the Fed would change the fed funds rate in response to changes in the unemployment rate and changes in inflation (i.e., the second derivative of the price level). Simply adding up these changes (flipping the sign for unemployment) has tracked well with changes in Fed policy. This relationship has held over several decades and through both tightening and loosening of monetary policy.

The Change in the Unemployment Rate and Change in Inflation Historically Track Changes in Fed Policy

Source: Guggenheim Investments, Haver Analytics. Actual data as of 3.31.2022 for core PCE, 4.30.2022 for unemployment rate and fed funds rate. *Note: unemployment rate excludes workers on temporary layoff.

However, over the past year there has been a notable divergence in this relationship. The steep drop in unemployment and sharp acceleration in inflation was met by an unresponsive Fed. This breakdown in the typical reaction of the Fed can be attributed to the unique nature of the pandemic shock, the Fed’s updated policy strategy, and a misreading of the inflation surge as transitory. The result is that the Fed, as it now acknowledges, is badly behind the curve and “expeditiously” moving ahead with 50 basis point hikes to both keep inflation expectations in check and protect its reputation.

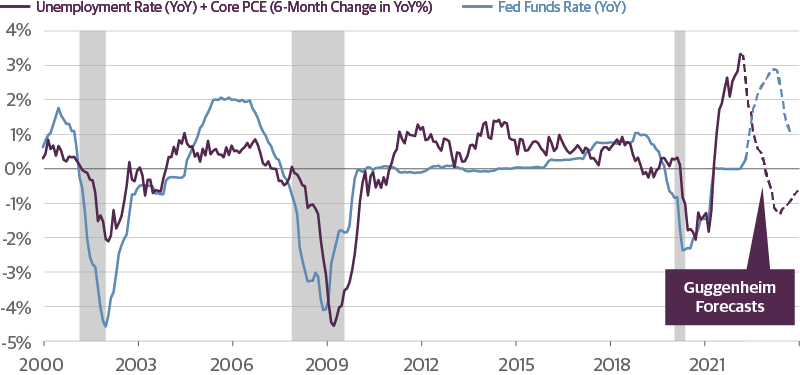

At the same time, however, inflation is now decelerating and the pace of decline in the unemployment rate is slowing. Had the Fed followed the historical pattern in the chart above, the fed funds rate would be around 2.5 percent now and the Fed would be able to start pulling back on rate hikes as the economy cooled. Instead, the Fed looks poised to hike to around 3.5 percent into next year, when inflation will have slowed further and the unemployment rate will have largely leveled off. With the passage of time as the Fed continues to hike, we will likely find ourselves experiencing the effects of increasingly restrictive monetary policy. Well before it reaches this terminal rate the Fed will increase the risk of overshooting, causing a financial accident, and starting a recession. Such an asynchronously tight monetary stance should exacerbate the cyclical slowing of the economy and cause a recession as early as the second half of next year. Given this collision course between the Fed and the cooling economy, long term interest rates are likely near a peak.

As Scrooge asked in Charles Dickens’ A Christmas Carol, “Are these the shadows of the things that Will be, or are they shadows of the things that May be only?” Only time will tell.

The Fed is Swinging from Delayed Lift Off to Overtightening

Source: Guggenheim Investments, Haver Analytics. Actual data as of 3.31.2022 for core PCE, 4.30.2022 for unemployment rate and fed funds rate. *Note: unemployment rate excludes workers on temporary layoff.

From the Office of the Global Chief Investment Officer of Guggenheim Partners, Scott Minerd

By the Macroeconomic and Investment Research Group

- Brian Smedley, Chief Economist and Head of Macroeconomic and Investment Research

- Matt Bush, CFA, CBE, U.S. Economist, Macroeconomic and Investment Research

Important Notices and Disclosures

Investing involves risk, including the possible loss of principal. Stock markets can be volatile. Investments in securities of small and medium capitalization companies may involve greater risk of loss and more abrupt fluctuations in market price than investments in larger companies. Investments in fixed-income instruments are subject to the possibility that interest rates could rise, causing their values to decline. High yield and unrated debt securities are at a greater risk of default than investment grade bonds and may be less liquid, which may increase volatility. Investors in asset-backed securities, including mortgage-backed securities and collateralized loan obligations (“CLOs”), generally receive payments that are part interest and part return of principal. These payments may vary based on the rate loans are repaid. Some asset-backed securities may have structures that make their reaction to interest rates and other factors difficult to predict, making their prices volatile and they are subject to liquidity and valuation risk. CLOs bear similar risks to investing in loans directly, such as credit, interest rate, counterparty, prepayment, liquidity, and valuation risks. Loans are often below investment grade, may be unrated, and typically offer a fixed or floating interest rate.

This material is distributed or presented for informational or educational purposes only and should not be considered a recommendation of any particular security, strategy or investment product, or as investing advice of any kind. This material is not provided in a fiduciary capacity, may not be relied upon for or in connection with the making of investment decisions, and does not constitute a solicitation of an offer to buy or sell securities. The content contained herein is not intended to be and should not be construed as legal or tax advice and/or a legal opinion. Always consult a financial, tax and/or legal professional regarding your specific situation.

This material contains opinions of the author, but not necessarily those of Guggenheim Partners or its subsidiaries. The opinions contained herein are subject to change without notice. Forward looking statements, estimates, and certain information contained herein are based upon proprietary and non-proprietary research and other sources. Information contained herein has been obtained from sources believed to be reliable, but are not assured as to accuracy. No part of this material may be reproduced or referred to in any form, without express written permission of Guggenheim Partners, LLC. There is neither representation nor warranty as to the current accuracy of, nor liability for, decisions based on such information. Past performance is not indicative of future results.

Guggenheim Investments represents the following affiliated investment management businesses of Guggenheim Partners, LLC: Guggenheim Partners Investment Management, LLC, Security Investors, LLC, Guggenheim Funds Distributors, LLC, Guggenheim Funds Investment Advisors, LLC, Guggenheim Partners Advisors, LLC, Guggenheim Corporate Funding, LLC, Guggenheim Partners Europe Limited, Guggenheim Partners Fund Management (Europe) Limited, Guggenheim Partners Japan Limited, GS GAMMA Advisors, LLC, and Guggenheim Partners India Management.

© 2022 Guggenheim Partners, LLC. All rights reserved.

GPIM 52711

© Guggenheim Investments

Read more commentaries by Guggenheim Investments