Any student of history or economics can attest to the fact that wars are expensive. True to form, the conflict in Ukraine and resurgent COVID-19 in China are creating inflationary pressures. Prices for a range of items are hitting the roof. This implies that inflation will likely peak at even higher levels than previously anticipated in major economies.

We expect the war to continue, but not snowball into a bigger conflict involving more nations. This has led to some notable adjustments to our growth and inflation outlook. Economic recovery will be dampened, but not derailed, amid erosion of purchasing power. The risks are tilted to the downside, with stagflation a particular threat for Europe.

Against this backdrop, central banks are becoming more active. The Fed and the Bank of England (BoE) delivered interest rate hikes this month.

Here are perspectives on how major economies are poised to perform this year and next.

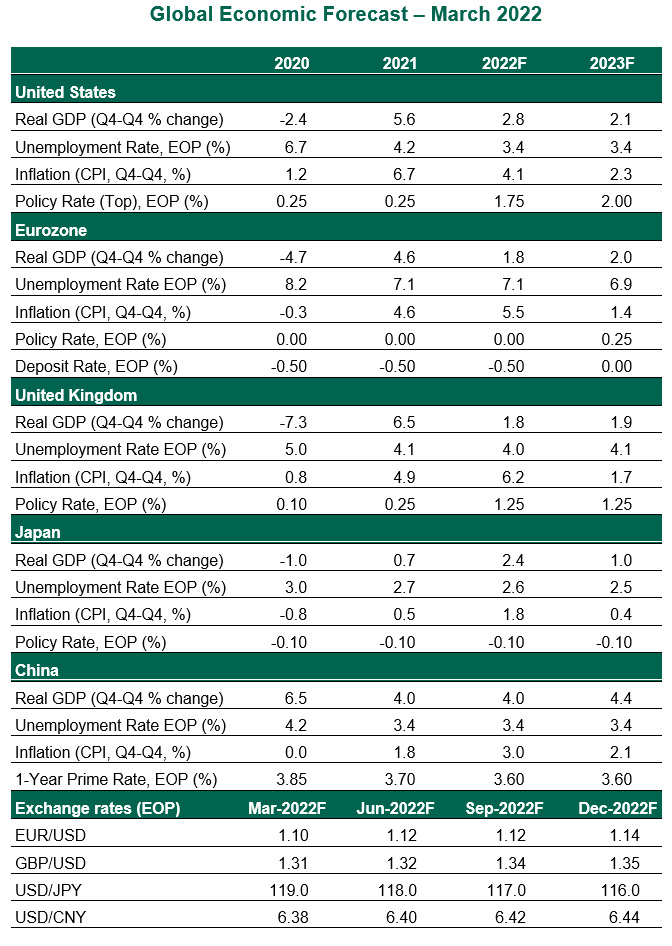

United States

- The Russia-Ukraine war has not changed our baseline U.S. outlook. The American economy is more detached from the conflict, geographically and commercially, owing to limited trade linkages with both nations. We expect positive domestic momentum to allow the economy to keep growing as consumers continue to spend and inventories rebuild. That said, the downside risks are accumulating.

- At its March meeting, the Federal Open Market Committee (FOMC) began an interest rate hiking cycle. The quarter-point increase will be followed by a number of others. We forecast six more hikes, with overnight rates leveling off in a range of 1.75-2.0%. High inflation and strong employment are the signals for a central bank to tighten, and we expect those conditions will persist.

Eurozone

- The impact of the war is starting to become apparent in the eurozone as the ZEW index of investor expectations sentiment experienced the biggest one-month decline in its history amid concerns over the economic outlook. The eurozone has close trade ties with Russia, mostly for energy, leaving the region highly exposed to the risks of the conflict. Inflation climbed to a record high of 5.9% year-over-year in February and is set to rise further in the near term. Household real incomes will be squeezed further, taking some air out of the recovery this year.

- Inflation fears exceeded growth worries as the European Central Bank (ECB) accelerated the tapering of its asset purchases at its meeting this month. The ECB also kept the door open to an interest rate hike later this year. In our view, given the ongoing uncertainty, rate hikes remain off the table this year, with tightening to commence in 2023 if conditions improve.

United Kingdom

- The U.K. economy, despite limited trade ties with Moscow, will also be affected by the commodity price shocks resulting from the war. Just as in 2011, when real income losses stalled household consumption, the rising cost of living this year will weigh on growth. The energy price cap is set to increase from April, which could push inflation to peak above 8% in the second quarter and remain well above the central bank’s target throughout the year. This raises the risks of an abrupt slowdown in growth.

- In line with expectations, the BoE raised the Bank Rate for the third successive meeting, returning the policy rate to its pre-COVID level. The BoE further signaled that more tightening is likely in months ahead. We think the growing downside risks favor a cautious approach to rate hikes. Hence, the BoE is expected to hike twice (25 basis points each) this year, before taking a long pause.

Japan

- Japan will be among the nations least affected by the war, owing to its negligible trade ties with Russia. However, China’s recent COVID surge presents a bigger risk to the near-term prospects of the Japanese economy. Japanese exports are being hindered by supply bottlenecks. As is the case elsewhere, the squeeze on households’ incomes in Japan will keep a lid on consumption, despite fiscal support measures such as petrol subsidies.

- While the other major advanced economy central banks are moving towards policy normalization, the Bank of Japan will continue to maintain status quo. Higher energy and commodity prices are expected to raise headline inflation closer to 2% in the coming months, but there are no real signs of sustained underlying price pressures. Pricing power among corporations remains weak, and wages are stagnant.

China

- China is still struggling to deal with COVID-19. Major hubs in the country are reeling under stringent restrictions. The Chinese economy is off to a disappointing start to 2022 on the back of a real estate downturn and sluggish consumption. Demand for services will remain weak as long as policymakers refuse to adjust their zero-infection approach. Renewed lockdowns will provide an unwelcome additional lift to commodity prices and delay supply chain normalization.

- The Government Work Report to the National People's Congress announced a gross domestic product growth target of "around 5.5%" this year. Though lower than last year's goal of 6%, the target still looks optimistic considering the plethora of domestic and external headwinds. Meeting this target would require substantial policy support, such as easing of property-sector regulations and credit policies, which are likely be delivered through the course of the year.

© Northern Trust

Read more commentaries by Northern Trust