Bonds have started slowly in 2022 due to persistent inflation, a looming Fed tightening cycle, and the Russia/Ukraine conflict. We believe the Osterweis Strategic Income Fund is well-positioned to address these challenges, as its flexible mandate and defensive approach help to protect against rising rates and market volatility.

The new year has not been kind to fixed income investors. Persistent inflation has motivated the Fed to reverse its easy monetary policy, while the war between Russia and Ukraine has created additional volatility. Thus far, bonds (as well as stocks) have delivered negative returns in 2022.

The Fed has a tough job, trying to cool inflation without causing the economy to slow down too much. We expect they’ll succeed, but even if they do, rising rates are likely to dampen fixed income returns for at least the near term. (Recall that as rates go up, existing bonds lose value.) Furthermore, weakness in the stock market is impacting credit quality, causing spreads to widen and putting additional downward pressure on bond prices.

Despite these headwinds, we believe the Strategic Income Fund (OSTIX) is well-positioned, thanks to our flexible mandate and defensive approach. Our shorter duration profile and tactical cash allocation effectively act as shock absorbers, allowing us to outperform during periods of both rising rates and elevated market volatility and to recover more quickly after major drawdowns. In addition, our management team has been through multiple boom/bust cycles over the past twenty years, so we have considerable experience navigating difficult markets.

Low Duration Protects Against Rising Rates

Managing interest rate risk is central to our investment strategy so we typically maintain a low duration profile, which helps mitigate losses during rising rate environments. (Of course, it has the opposite effect when rates fall, but we prefer to sacrifice some upside to increase our downside protection.) Our duration is currently lower than our peers’ as well as the investment grade Bloomberg Aggregate (the Agg) and the ICE BofA High Yield (ICE HY) indices, as it has been historically.

Additionally, most of our portfolio is invested in non-investment grade bonds, which are generally less sensitive to changes in interest rates than their investment grade (IG) counterparts. We further reduce our duration by investing primarily in issues with shorter maturity dates, reserving our investments in longer maturities for only the most attractive positions.

Our healthy allocation to cash also lowers our overall duration, as does our exposure to convertible bonds, which are less sensitive to rising rates than other types of fixed income securities.

Tactical Cash Allocation Limits Volatility

Our tactical cash allocation does more than reduce our duration – it also dampens our volatility. Bond prices are typically more stable than stock prices, but sudden changes in market sentiment still occur, particularly in non-investment grade debt. Our cash buffer can partly offset fluctuations in the invested portion of the portfolio.

Perhaps more importantly, our cash also provides us with the flexibility to take advantage of market selloffs in real-time without disrupting our portfolio. We like to keep an ample supply of “dry powder” on hand, as it allows us to purchase attractive bonds (including convertibles) at discounted prices. Historically, some of our best performing positions have been acquired during periods of market distress. An added benefit of this approach is that it accelerates the fund’s recovery timeline once the market begins to stabilize.

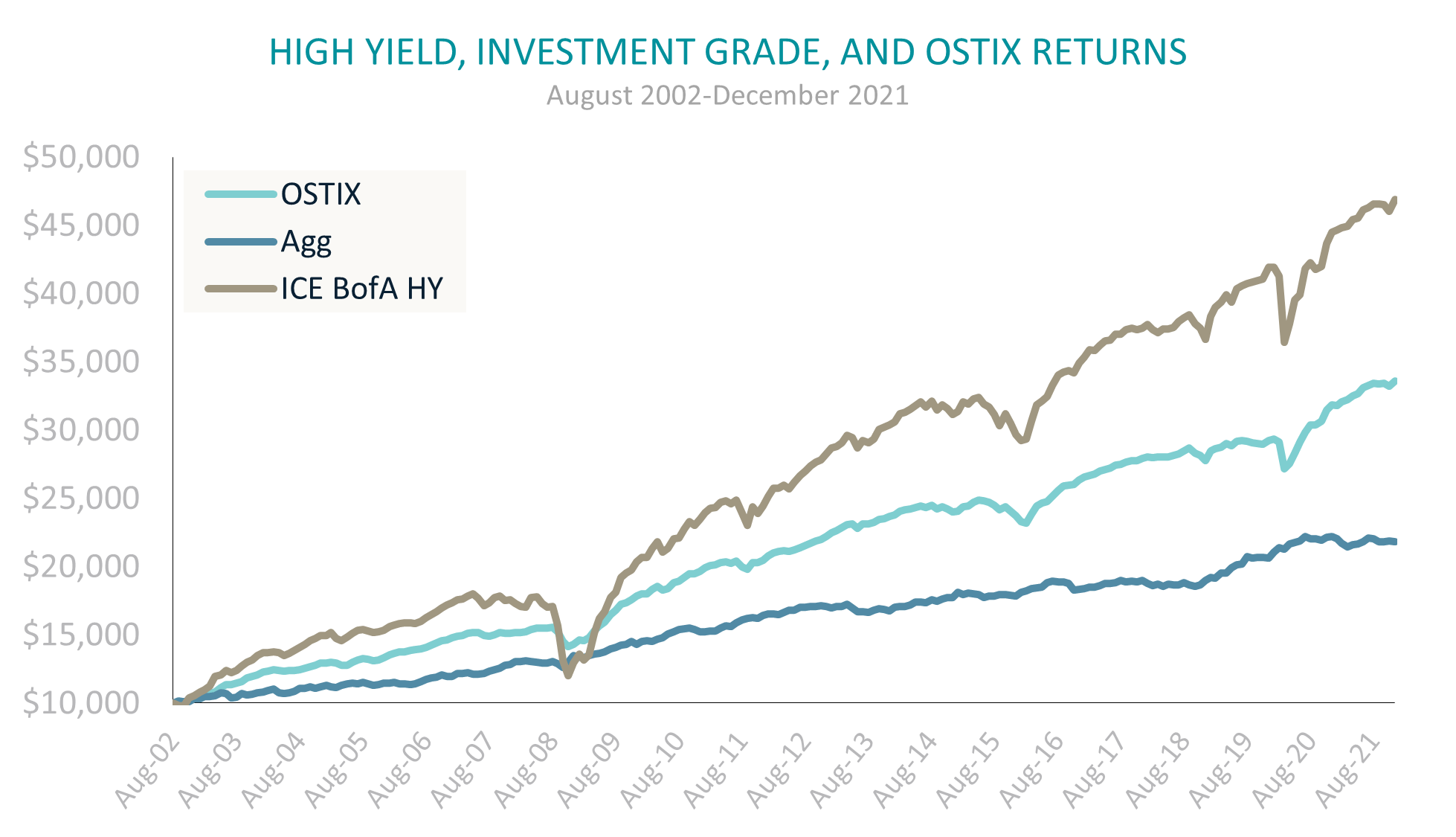

Consistent Long-Term Performance

Since its inception nearly 20 years ago, our mutual fund has delivered relatively consistent results. As you can see below, we have solidly outperformed the investment grade index, while we have lagged the non-investment grade index. We developed the Strategic Income Fund to provide clients with a fixed income solution that could outperform the Agg over the long term without taking on excessive risk. Based on our track record, we feel we are succeeding.

Source: Bloomberg Indices, ICE Indices, Osterweis. Past performance does not guarantee future results.

The following table shows our standard deviation versus the same indices. Unlike our returns, which are roughly halfway between the two, our standard deviation is much closer to the investment grade index in every period. (Note that the fund had lower volatility than both indices in the past year.)

| YEARS |

OSTIX |

AGG |

ICE BOFA HY |

| 1 |

2.0 |

2.7 |

2.5 |

| 3 |

5.5 |

3.4 |

9.1 |

| 5 |

4.5 |

3.0 |

7.4 |

| 10 |

3.9 |

3.0 |

6.5 |

| 15 |

4.2 |

3.2 |

9.7 |

Figures are in percent and are annualized. Source: eVestment, data as of 12/31/2021

Beyond the obvious benefits of limiting drawdowns and generating more predictable returns, the fund’s lower standard deviation gives investors more flexibility when managing their risk budgets. Essentially, the fund gives investors the option to deploy risk elsewhere and/or increase fixed income returns without substantially raising overall portfolio risk.

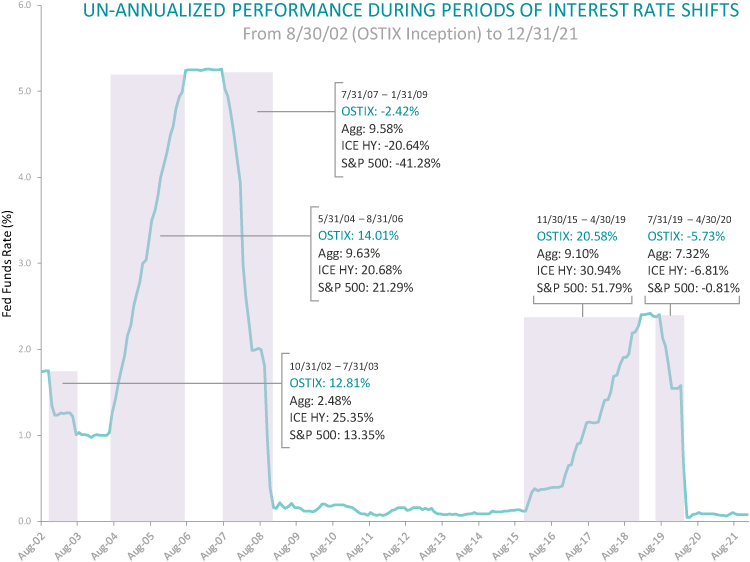

Resilient During Selloffs

In addition to delivering relatively consistent performance over the long run, the fund has been particularly resilient in periods of market distress. The chart below shows how the fund held up during the previous two Fed tightening cycles and the subsequent market corrections. Fed policy tends to have a bit of a lag effect, as they’re usually raising rates during the late stage of an economic expansion, so most markets were rising during both tightening cycles. As expected, in each period (2004-2006 and 2015-2019) the fund underperformed the HY index and outperformed the IG index. Conversely, when the Fed decided to cut rates following the market correction, the fund outperformed HY but lagged IG. Again, this is the expected outcome, as the fund carries less risk than HY but more than IG.

Source: Bloomberg and RIMES. Past performance does not guarantee future results.

Final Thoughts

The current conditions are challenging for fixed income investors, but we believe our fund is well-positioned to handle them. Moreover, we believe our fund is an excellent long-term investment. Our consistent track record and favorable risk/return profile demonstrate our ability to continually adapt to changing markets, and our two decades of experience have taught us much about navigating volatile market cycles.

For more information about this strategy, please send us an email or call us at (800) 700-3316.

Opinions expressed are those of the author, are subject to change at any time, are not guaranteed and should not be considered investment advice.

Standardized performance is available here. This document is available in electronic format only.

Performance data quoted represent past performance; past performance does not guarantee future results. The investment return and principal value of an investment will fluctuate so that an investor’s shares, when redeemed, may be worth more or less than their original cost. Current performance of the Fund may be higher or lower than the performance quoted. Performance data current to the most recent month end may be obtained by calling (866) 236-0050. An investment should not be made solely on returns. The Fund’s gross expense ratio was 0.88% as of March 31, 2021.

Mutual fund investing involves risk. Principal loss is possible. The Osterweis Strategic Income Fund may invest in debt securities that are un-rated or rated below investment grade. Lower-rated securities may present an increased possibility of default, price volatility or illiquidity compared to higher-rated securities. The Fund may invest in foreign and emerging market securities, which involve greater volatility and political, economic and currency risks and differences in accounting methods. These risks may increase for emerging markets. Investments in debt securities typically decrease in value when interest rates rise. This risk is usually greater for longer-term debt securities. Small- and mid-capitalization companies tend to have limited liquidity and greater price volatility than large-capitalization companies. Higher turnover rates may result in increased transaction costs, which could impact performance. From time to time, the Fund may have concentrated positions in one or more sectors subjecting the Fund to sector emphasis risk. The Fund may invest in municipal securities which are subject to the risk of default.

The Bloomberg U.S. Aggregate Bond Index (BC Agg) is an unmanaged index that is widely regarded as a standard for measuring U.S. investment grade bond market performance.

ICE BofA U.S. High Yield Index tracks the performance of U.S. dollar denominated below investment grade corporate debt publicly issued in the U.S. domestic market.

Indices cited do not incur expenses and are not available for investment. These indices reflect the reinvestment of dividends and/or interest. Historical fixed income index data is provided for informational purposes only, not as an indication of future Fund performance.

Duration measures the sensitivity of a fixed income security’s price (or the aggregate market value of a portfolio of fixed income securities) to changes in interest rates. Fixed income securities with longer durations generally have more volatile prices than those of comparable quality with shorter durations

The Osterweis Funds are available by prospectus only. The Funds’ investment objectives, risks, charges and expenses must be considered carefully before investing. The summary and statutory prospectuses contain this and other important information about the Funds. You may obtain a summary or statutory prospectus by calling toll free at (866) 236-0050, or by visiting www.osterweis.com/statpro. Please read the prospectus carefully before investing to ensure the Fund is appropriate for your goals and risk tolerance.

Osterweis Capital Management is the adviser to the Osterweis Funds, which are distributed by Quasar Distributors, LLC. [OSTE-20220302-0456]

© Osterweis Capital Management

Read more commentaries by Osterweis Capital Management