Americans Added $1 Trillion In New Debt Last Year

Membership required

Membership is now required to use this feature. To learn more:

View Membership Benefits1. Consumer Debt Tops A Record $15 Trillion

2. GDP Rose 7% in 4Q, Up 5.7% For All Of Last Year

3. Household Debt Is Now At Highest Level On Record

4. Consumers Added $1 Trillion In New Debt In 2021

5. Personal Debt By Age Group – Excluding Mortgages

Overview – Consumer Debt Tops $15 Trillion, GDP Up 7%

American households took on over $1 trillion in new debt in 2021 for only the second time in history, pushing consumer debt above $15 trillion for the first time ever. The near-record increase in household debt came despite various government stimulus programs last year, including checks directly from the Treasury.

The Federal Reserve, which issued the report on household debt last month, said the large increase was driven in part by soaring prices for homes and automobiles among other big-ticket items. We’ll look at the underlying factors as we go along today.

Following that discussion, we’ll look at outstanding consumer debt by age group – excluding home mortgage debt. I think you’ll be surprised to see how much debt each generation owes even without their mortgages included.

Before we get to our discussion on the spike in household debt, let’s look at the latest report on Gross Domestic Product for the 4Q, which came out last week. The economy grew at an annual rate of 7% in the final three months of last year. For all of 2021, the US economy grew at the fastest pace since 1984 as we rebounded from the brutal COVID recession of 2020.

GDP Rose 7% in 4Q, Up 5.7% For All Of Last Year

The US economy ended 2021 by expanding at a brisk 7% annual pace from October through December, the government reported last week, a slight upgrade from its earlier estimate as businesses stepped up their restocking of supplies.

For all of 2021, the nation’s gross domestic product — its total output of goods and services — jumped by 5.7%, the fastest calendar-year growth since a 7.2% surge in 1984 in the aftermath of a serious recession.

The economy’s growth in the final quarter of 2021 was driven by a 33.5% jump in business investment as companies worked to replenish their inventories. In fact, inventory restocking accounted for 70% of the 4Q GDP growth.

For all of 2021, consumer spending surged 7.9%, the fastest such growth since 1946. But it slowed to an annual pace of just 3.1% in the October-December quarter as an uptick in coronavirus cases, which has now faded, kept more Americans at home and away from restaurants, travel destinations and entertainment venues.

The outlook for 2022 is not nearly as bright, although a survey of economists earlier this month predicts US GDP will expand by 3.4% this year. The International Monetary Fund predicts the US will grow by 4% this year. Either of those would be very respectable.

A lot depends on how much and how fast the Fed raises interest rates and what happens with Russia in Europe. Barring some big unexpected negative surprise, it should be another good year, which is why I expect the stock markets to find their footing and recover relatively soon.

Consumers Took On $1 Trillion In New Debt In 2021

Americans took on more new debt in 2021 than in any year since 2007, just before the 2008-09 financial crisis, which sent the economy into a deep, painful recession we will never forget.

Total household debt rose by $1.02 trillion last year to $15.6 trillion, the highest total ever recorded – boosted in large part by higher balances on home and auto loans, the Federal Reserve Bank of New York reported last month. It was the largest annual increase since a $1.06 trillion jump in 2007 – which was followed by the most severe financial crisis since the Great Depression.

The increase is in large part a function of the unexpected sharp rise in prices for homes and cars last year. The median home price rose between 16% and nearly 20% last year, depending on whose figures you believe. While that was bad news for would be buyers, it was a boon for those who already owned a home.

The National Association of Realtors (NAR) says the median home price last year rose to a record $346,900 – a rise of nearly 17% over 2020. A typical homeowner with a home valued at that level accumulated over $40,000 in new housing wealth last year, but it also priced out many middle-class buyers. Buying a home is now out of reach for millions of Americans.

The Federal Reserve says median home values are even higher than the NAR’s estimate. The Fed says the average (not median) home price rose to $408,100 by the end of 2021, a rise of nearly 20%. Either way, it was a stunning increase in home prices.

On another front, the shortage of computer chips for cars caused automakers around the country to cut back on production. With inventories of new cars low, dealerships jacked up prices accordingly, not only on new cars but pre-owned vehicles as well. Used car prices skyrocketed nearly 30% last year alone. The Department of Labor reported earlier this month that used car prices jumped 29.7% last year alone.

The question is, will new and used car prices come down later this year as automakers hopefully get back to full production. This is a very interesting discussion with several complicated variables at play. I’ll have more to say on whether car prices are likely to come down just ahead.

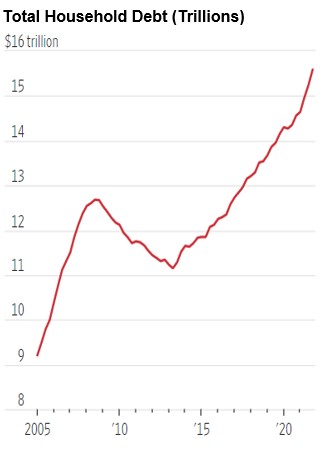

Household Debt Is Now At Highest Level On Record

The question is, why are Americans taking on so much new debt? American families sharply reduced spending during the coronavirus recession in 2020 when people cut way back on going out to eat, entertainment, traveling and other discretionary spending.

Now that the economy has rebounded rather strongly, people are in the mood to spend again. Pent-up demand for entertainment, eating out, travel and other purchases consumers were unable or unwilling to make earlier in the pandemic boosted credit-card balances significantly in the final three months of last year.

Americans added $52 billion to their credit-card balances in the 4Q of 2021 alone, the largest quarterly jump ever recorded, the New York Fed said in its latest report on household debt and credit earlier this month.

As noted above total consumer debt now sits at an estimated $15.6 trillion, compared with $14.6 trillion a year earlier. This is the highest level of household debt ever recorded. As the chart above illustrates, household debt has been rising exponentially since 2014. The question, of course, is: How long can this continue?

Now here is an interesting take on the record rise in consumer debt: The Fed tells us the rise in consumer borrowing isn’t cause for alarm. How can that be? The New York Fed economists say it’s because household wealth increased across all income levels during the pandemic, since most people saved a considerable amount of money – though much of the gains accrued to the richest Americans.

Furthermore, the Fed says “subprime” borrowers accounted for just 2% of the mortgage debt originated in the 4Q of 2021, down from an average of 12% in the years before the financial crisis. If true, that is very encouraging. Subprime mortgages are those granted to individuals with credit scores of 640 or lower (often below 600) who would not qualify for a conventional mortgage.

What’s more, they say, is some 87% of the new debt last year was tied to homes which typically appreciate over time, allowing borrowers to build wealth despite taking on more debt (depending on how much, of course). Today’s homeowners are therefore in better financial shape, they tell us. If true, that is also encouraging.

Personal Debt By Age Group – Excluding Mortgages

The Fed’s latest report indicating household debt reached a record $15.6 trillion last year includes outstanding home mortgage debt. Let’s look at outstanding debt balances excluding mortgage balances. Let’s also look at it broken down by age groups. I think these numbers, not including mortgage debt, will surprise you.

The average outstanding debt figures above include student loans, auto loans, credit card debt, personal loans, etc. – but not mortgage balances. The average across all age groups is $92,727.

I was most surprised to see Generation Xrs (age 40-55) have average debt of $140,643 plus their mortgage on top of that. A contributing factor is that many of these Americans are sending their kids to college for the first time and are borrowing money to do so – even though some are still carrying student loan debt from when they went to college.

In closing, I continue to worry there is a limit to how much debt we can take on, both at the household level and the federal government level. But American consumers and politicians on both sides of the aisle continue to prove me wrong.

The question, as always, is: How long can it last? Your guess is as good as mine.

Membership required

Membership is now required to use this feature. To learn more:

View Membership BenefitsSponsored Content

Upcoming Virtual Events View All