Chief Economist Scott Brown discusses current economic conditions.

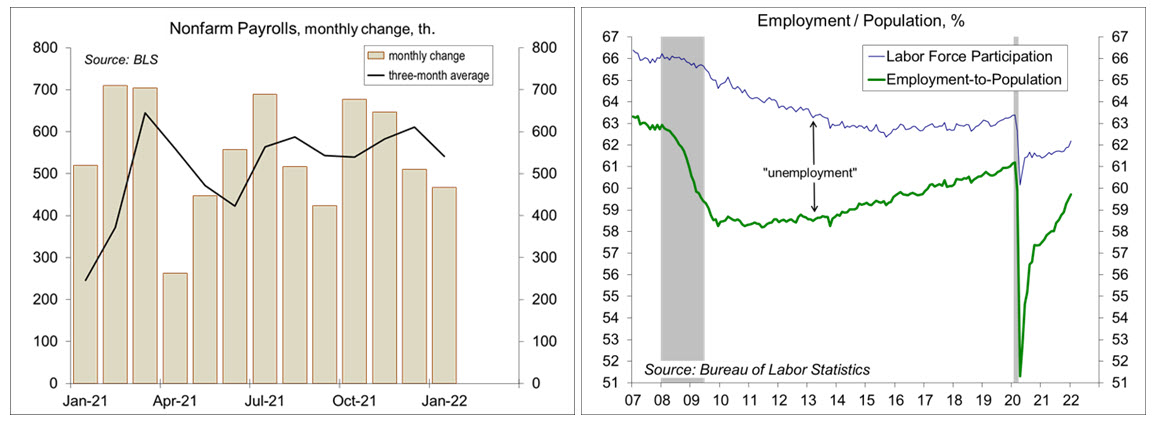

The January job market data were expected to be squirrelly, with the Omicron variant expected to dampen the pace of nonfarm payrolls. Instead, we got an upside surprise. Payrolls rose by 467,000. More importantly, annual benchmark revisions redistributed job growth over the course of last year, showing a much stronger near-term trend. Wage pressures continued. One shouldn’t make too much of any single report, but the January data suggest that a 50-basis-point hike should be on the table at the mid-March FOMC meeting.

Seasonal adjustment is huge in January. We lost 2.82 million jobs before adjustment. That’s less than usual (unadjusted payrolls averaged a 2.94 million decline in the five most recent pre-pandemic Januarys). That makes sense. There is seasonality related to the holiday shopping season (retail, deliveries), the weather (construction), leisure & hospitality, and the school year. One might expect that these seasonal losses would be smaller this year – either because fewer workers were hired last year or because firms would be reluctant to give up workers in a tight job market. Whatever the case, a smaller-than-usual decline in unadjusted jobs translates to a strong gain in adjusted jobs.

The U.S. averaged 800,000 COVID-19 cases per day in mid-January (vs. a peak of a little less than 200,000 during the Delta wave). Omicron surely had an impact on the January labor market figures. We saw a sharp run-up in weekly jobless claims in the first couple of weeks of the month, down more recently (the payroll data are for the pay period that includes the 12th of the month, so the monthly figures are more indicative of the first half of the month). Omicron lowered average weekly hours (34.5, vs. 34.7 in December and 34.8 in November). Details of the Household Survey data (which covers the week that includes the 12th of the month) showed that 2.3% of those with jobs could not work due to illness (in comparison, it was 1.0% in the Delta wave).

Once a year, the Bureau of Labor Statistics benchmarks the figures to payroll tax receipts. The March 2021 level of payrolls was revised down by 166,000 (or -0.1%) – very small. More importantly, the benchmark revision shifted job growth around last year. Instead of a downtrend, with softer numbers in the fourth quarter. The trend now appears flatter – and much stronger in the near term. November and December were revised a net 709,000 higher. Payrolls averaged a 541,000 gain over the last three months.

The unemployment rate edged up to 4.0% in January (from 3.9% in December, reflecting an increase in labor force participation. That increase was concentrated among teenagers and those over 54, which seems like noise. The broad U-6 unemployment rate, which includes discouraged workers and those involuntarily working part time, fell to 7.1% (from 7.3% in December and 11.1% a year ago). It was 6.9% in 4Q19 (before the pandemic). Job openings remain near record highs, far above pre-pandemic levels. The quit rate fell in December, but remains high. Firms continue to report difficulties in hiring workers and retaining current employees.

Average hourly earnings rose 0.7% in January (up 5.7% y/y). For production workers, average hourly earnings rose 0.6% (+6.9% y/y). Average hourly earnings are not the most reliable gauge of labor costs. Compositional changes (such as faster or slower growth in lower paying industries) can bias the figures one way or the other – but clearly the direction is higher. The Employment Cost Index for the private sector (which compensates for compositional changes and includes benefit costs) rose 4.4% in the 12 months ending in December (vs. +2.6% for the 12 months ending December 2020). Higher wages could lure many of those on the sidelines back into the workforce, but even if that were the case, it would take some time.

So, we have a strong trend in job growth, a tight labor market, and rising wage pressures. That’s good for workers, but demand is outpacing supply. Higher inflation eats away at consumer purchasing power and the Fed risks a more painful adjustment if it doesn’t act to keep inflation in check.

The January Employment Report puts a 50-basis-point rate hike in March on the table. Federal funds futures are factoring in about a 35% change of a 50-bp move. We’ll get a lot more data between now and the mid-March FOMC meeting, including another employment report, two CPI reports, and two retail sales reports. The CPI figures have the most potential to shift the Fed policy outlook. January figures are due on February 10. An upside surprise would put more pressure on the Fed to act aggressively.

Recent Economic Data

Nonfarm payrolls rose by 467,000 in the initial estimate for January (down 2.82 million before seasonal adjustment). Annual benchmark revisions shifted job growth in 2021 – now a stronger near-term trend (vs. a downtrend in the previous data).

Click here to enlarge

The unemployment rate edged up to 4.0% in January (vs. 3.9% in December), as labor force participation picked up (mostly for teenagers and those over 50, which seems like noise). The employment/population ratio is trending higher (59.7% in January, vs. 57.5 a year ago and 61.0% in 4Q19.

The ADP estimate of private-sector payrolls fell by 301,000 in the initial estimate for January, following a revised 776,000 gain in December.

Job openings rebounded to 10.9 million in December (9.9 million for the private sector) – still elevated.

Click here to enlarge

Unit Motor Vehicle Sales rose to a 15.0 million seasonally adjusted annual rate in January, vs. a 12.5 million pace in December. However, seasonal adjustment likely exaggerated the improvement (January is the low point for unadjusted sales). Sales were 25% lower than in January 2021.

The ISM Manufacturing Index fell to 57.6 in the January (following 58.8 in December). The ISM Services Index slipped to 59.9 (vs. 62.3). Both reports were consistent with moderately strong growth in the overall economy, but the Omicron variant, supply chain issues, and labor shortages were restraints.

Nonfarm productivity rose at a 6.6% annual rate in the preliminary estimate for 4Q21 (+2.0% y/y). Unit labor costs, the key measure of inflation pressure from the labor market, rose at a 0.3% pace (+3.1% y/y).

Factory orders fell 0.4% in December (+13.3% y/y), reflecting a 14.4% drop in civilian aircraft orders. Orders for nondefense capital goods ex-aircraft rose 0.3% (+10.6% y/y), with shipments up 1.3% (+10.4% y/y).

Click here to enlarge

COVID-19 cases remain high, but are trending lower, following a sharp spike into mid-January. More than 16,000 Americans are dying per week from the virus.

Jobless claims fell by 23,000 in the week ending January 29, to 238,000 (a 255,000 average for January, up from 204,000 in December), reflecting a fading impact from the Omicron variant.

Click here to enlarge

The Bank of England’s Monetary Policy Committee voted 5-4 to raise the Bank Rate by 25 basis points (to 0.5%). The four no votes wanted a 50-basis-point increase.

The opinions offered by Dr. Brown are provided as of the date above and subject to change. For more information about this report – to discuss how this outlook may affect your personal situation and/or to learn how this insight may be incorporated into your investment strategy – please contact your financial advisor or use the convenient Office Locator to find our office(s) nearest you today.

This material is being provided for informational purposes only. Any information should not be deemed a recommendation to buy, hold or sell any security. Certain information has been obtained from third-party sources we consider reliable, but we do not guarantee that such information is accurate or complete. This report is not a complete description of the securities, markets, or developments referred to in this material and does not include all available data necessary for making an investment decision. Prior to making an investment decision, please consult with your financial advisor about your individual situation. Investing involves risk and you may incur a profit or loss regardless of strategy selected. There is no guarantee that the statements, opinions or forecasts provided herein will prove to be correct.

© Raymond James

Read more commentaries by Raymond James