Nearly four years ago, we wrote a market commentary titled “A New Waze of Investing” in which we highlighted the incredible technological innovations that were changing our everyday lives and our perspectives on long-term investing. Following along with those technologies has been a great benefit over the years in all aspects of life. Still, have you ever taken one of those back-road “short-cuts” to get around a car wreck on the highway ahead, and the next thing you know, by trying to save ten minutes on your hours-long journey, you’re now lost on a dirt road with no cellular service? Suffice it to say, we’ve been there. It’s in those moments that you realize the value of having perspective on your ultimate goal, as well as the value of having patience along the journey.

We see a parallel for markets today, where thousands of drivers enter the market’s thoroughfares every day, each with their own destination, navigating at various speeds, often causing chaos, and the occasional wreck along the way. At any moment, the action is hard to explain, and it can be maddening at times. Are people really slowing to a halt because there’s an accident on the other side of the highway?!?! Keeping focus on your destination and on the structural forces that lay the path for you to get there is key. Distractions from the perpetual news alerts pinging your phone can, on the other hand, leave you calling for help. So, what are the forces carving out the clearest paths for 2022? That is the subject at hand.

Nominal GDP growth will still be solid this year

First, nominal GDP growth is likely to be solid this year, albeit not at 2021’s historic levels. The real economy is being driven by powerful consumer demand, catalyzed by a booming labor market with personal incomes growing 10% year-over-year. Generationally high wage gains will support consumption growth, especially in 2021’s supply-constrained sectors, like autos and housing. In addition, inventories still need to be rebuilt, a significant tailwind for overall production. At the same time, corporations’ intentions for capital expenditures (capex) and research and development (R&D) have accelerated, especially for investments in productivity-enhancing technologies. Thus, the backdrop for earnings growth is still impressive. That said, we would also caution that there are some near-term pressures weighing on growth, as both the Omicron Covid variant has kept consumer behavior from normalizing as rapidly as many expected and lack of product availability has been a headwind too.

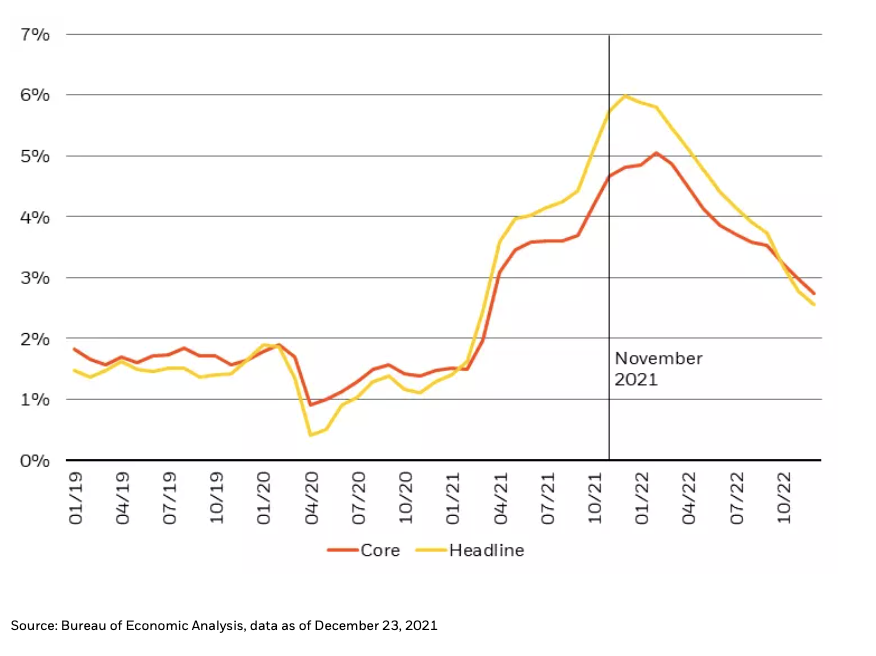

Figure 1: Base effects and some easing of supply chain issues moderate inflation by year end

While we are seeing early signs of moderation in supply-chain stresses, economic velocity is now gaining support from increased commercial and industrial (C&I) and consumer lending, which can keep upward pressure on prices for several more months, in our view. Our projection is for Core PCE inflation to ultimately migrate back to the 2.5% to 3.5% range by year-end, as commodity prices plateau near these elevated levels and as many of the logistical bottlenecks loosen up over time (see Figure 1). However, over the coming months, we are preparing for more headline-grabbing inflation data points that could send the media and some traders into a tailspin. Also, clearly there will be some inflation-stickiness from persistently higher wage levels and a corporate sector that is in the luxurious position of being able to raise prices almost at will.

Fed policy expectations have shifted radically in recent months, and policymakers need to be cautious

Very important to 2022’s market path is how the Federal Reserve responds in the months ahead, especially in the face of these potentially uncomfortable inflation readings. The Fed’s policy response to the pandemic was heroic, and their ongoing accommodation has been instrumental in enabling the real economy to withstand waves of new Covid variants. But with real-economy confidence now sufficiently restored, the Fed needs to migrate monetary policy back toward a neutral stance, before pausing to determine if more restrictive monetary policy is required. In our view, one of the market’s riskiest blind spots for this year will be navigating what sort of portfolio allocation changes, lane shifts if you will, might need to be made as Fed policy evolves.

From our perspective, the Fed’s policy toolkit should consist of policy rate hikes as well as some reduction in its balance sheet. On rates, targeting the pre-Covid level of 1.50% Fed Funds as an initial destination seems prudent, with data dependence setting a high hurdle to adjust to more accommodative, or restrictive, levels. We subscribe to the economic theories that argue that ‘policy works with long and variable lags,’ and that inflation tends to be a lagging indicator. With that perspective, we support the Fed setting a course to an achievable resting place as a good first step on the policy journey.

With regard to the balance sheet, a few observations help set the guardrails. More than 40% of U.S. M2 (a monetary aggregate) is now comprised of injected Fed liquidity, and in turn, U.S. M2 is now 92% of U.S. NGDP, the highest level ever. One can conclude that ebbing or flowing Fed policy liquidity has a direct and immediate impact on real economy activity, and that a liquidity withdrawal that goes beyond the technical adjustment of removing excessive money market liquidity amounts to the Fed demanding remittances back from the private sector, which could be an immense, unintended confidence shock for markets and the real economy. Caution is warranted as the Fed pursues balance sheet normalization, as we suspect the economy can operate with a larger Fed balance sheet with few (if any) negative consequences, other than the possibility of some misguided criticism.

Follow Rick Rieder on Twitter

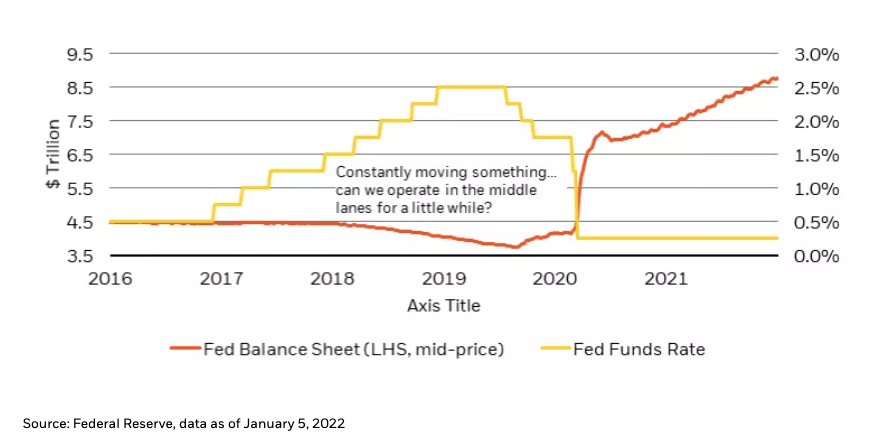

In short, the Fed operates on top of the most dynamic, self-correcting economy in the history of the world. Cushioning the system is critical when a major shock occurs (e.g., a historic and unpredictable global pandemic), but otherwise, the Fed’s stated destination of price, market and economic stability is probably best reached by operating with policy stability, while allowing the vibrant, innovative, and flexible U.S. economy to recalibrate organically. Indeed, Fed policy has been in nearly constant motion in recent years (see Figure 2), but now that the central bank has found itself behind the curve, we think the risk of normalizing policy too abruptly, or too much, weighs as a significant risk for markets.

Figure 2: Fed policy has been in constant motion, so modest moves now make sense

Finally, we expect two other sources of policy mandates to play a major role on the road to investing success in 2022. First, how China responds to the confluence of property market leverage problems, the persistent risk of Omicron spread, higher input prices, and broader credit creation needs could seriously alter the course ahead. We suspect a moderate and economically supportive approach, but we will keep one foot near the brake and one hand on the turn-signal in case more patience is needed. Second, evolving climate-focused policy initiatives will continue to play a very large role in dictating where investment dollars are allocated, with a significant feedback to how and where prices are set, and profits are earned.

Asset allocation considerations

With all of this in mind, our conclusions on asset allocation very much depend on where you are going and how fast you’re trying to get there. The best road for day traders is often a long way from the course charted out by retirement planners or reserve managers. Following the latest headline can save you two minutes, or it can get you lost for a while. For our portfolios, we consider more the path of an investor with a medium-term time horizon, who would like to take advantage of sudden changes ahead, but not at the risk of missing the destination.

Through that lens, we see decent value in the short end to belly of the U.S. Treasury market, which we think is fairly pricing anticipated policy tightening, and where yields offer some protection against downside for the first time since the onset of Covid. Clearly, though, some overly aggressive Fed overshooting on policy could press these yields still moderately higher. The very back-end of the U.S. Treasury curve, while it can be a more volatile trading vehicle, can provide a decent entry point to defease liabilities for long-term managers.

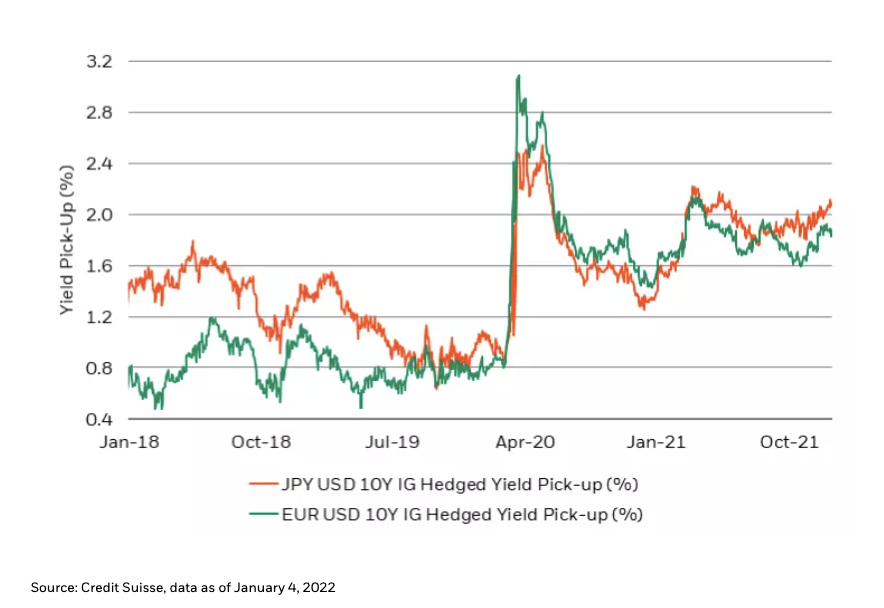

In credit, while we argued for a barbell of cash and high yield bonds in 2021, investors can now deploy that cash into investment grade issues for a reasonable contribution to the 3% to 5% fixed income portfolio goal, especially as buying from foreign reserve managers picks up (see Figure 3). And while emerging markets (EM) were best avoided last year (excluding China), the proactive increases in policy rates from EM central banks, to fend off inflation, have now created an attractive opportunity set of real rates to buy in 2022, albeit with patience and tactical entry points needed as noise from Fed tightening can cloud the vision here.

Figure 3: Currency hedge-adjusted yields continue to look attractive to foreign investors

Bank loans can also perform well with a strong economy and modestly higher rates and bespoke securitized assets in commercial real estate, consumer credit, and CLOs should round out investors’ fixed income portfolios. These securitized sectors are likely to witness meaningful support from vibrant economic cash flows and an enormous pool of cash that needs attractive returns in a still low-yielding world.

Finally, equities will be hard pressed to match last year’s gains, but with nominal GDP approaching or exceeding 7% helping to fuel top-line growth, and with the benefits of operating leverage still contributing to the bottom-line, we think it’s reasonable to possibly see 15% earnings growth in 2022. Multiples may contract a bit as the Fed normalizes policy, but a 9% to 10% equity return strikes us as risk worth taking for most investors focused on their longer-term objectives. Still, we are also respectful of the uncertainty of near- and intermediate-term Fed policy, which could keep down the cap structure and place credit markets on edge for a while, and thus potentially provide better entry points over the coming weeks. The “Waze” ahead for 2022 should be centered along these major lanes of investment influence, but as always, and perhaps more so than last year, we need both hands on the wheel, and clear eyes on the action in front of us, to avoid any accidents on what will likely be a bumpy road.

© BlackRock

Read more commentaries by BlackRock