2022 Investment Grade Credit Outlook: Views on Risk Appetite, Rising Stars and Trends

By the Investment Grade Credit Sector Team

1) With market volatility on the rise, how concerned are you about the potential for spreads to widen significantly and dent risk appetite?

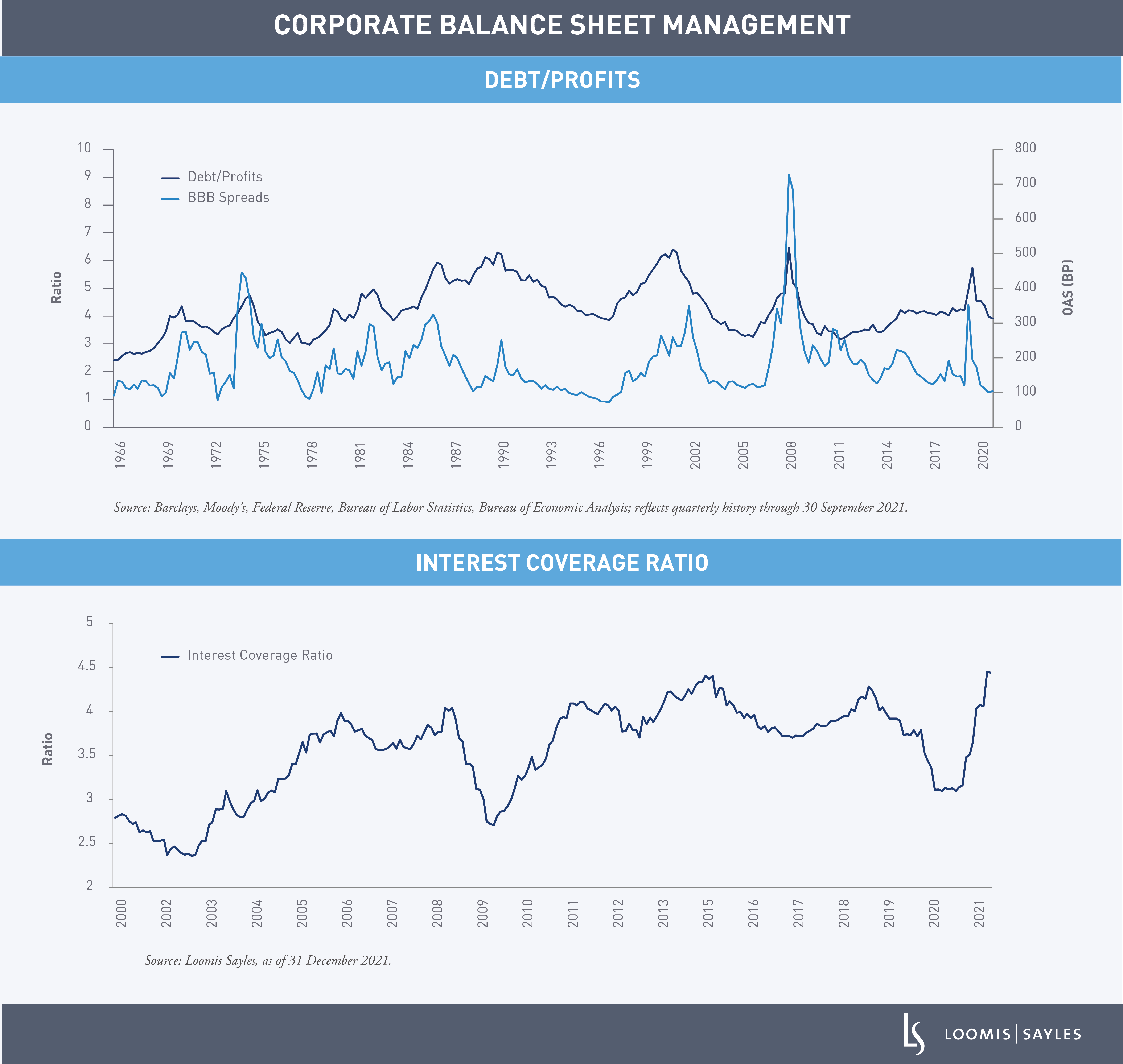

We may see some more market indigestion if the Treasury market continues to reprice Federal Reserve rate hike expectations, but we believe the environment is still positive for investment grade (IG) credit. Before the pandemic, the corporate sector was exhibiting late-cycle behavior. Corporate health was the weakening link then, and we believe we are a long way away from that today. The majority of industries appear to be in the expansion phase of the credit cycle, which we believe should support risk appetite.

Our views are anchored by bottom-up fundamentals, which look favorable for IG credit. Loomis Sayles credit research analysts have stable to improving outlooks for all but the electrics industry. Corporate health and earnings remain very positive. Margins and free cash flow have improved. Leverage has returned to pre-pandemic levels, or a hair better. Supply chain issues have been persistent, but consumers appear willing to spend more amid very strong pent-up demand.

We will be closely monitoring companies’ financial policies. Management teams have started behaving more aggressively with respect to shareholder returns, which will likely limit rating upside in certain industries.

2) Some market participants have speculated that more than $200 billion of high yield debt could be upgraded to the investment grade market this year (these issuers are known as rising stars). Do you agree with this view? What impact could it have on the market?

Loomis Sayles has a proprietary credit rating upgrade/downgrade model, which we update quarterly. In December, our model projected $284 billion in potential rising star volume in 2022, which is slightly higher than JP Morgan’s most recent $277 billion estimate for fiscal year ending 2023.[i] We believe rising stars will add a significant amount of supply back to the IG market, particularly in the BBB space. We think there will be a number of interesting opportunities as bonds move from high yield sellers to IG investors.