Musicians in an orchestra are arranged to have a clear view of the conductor, who sets the pace of each song. All eyes in the marketplace are now fixed on the maestros leading the Federal Reserve, looking for cues indicating whether the pace of asset purchase tapering might increase.

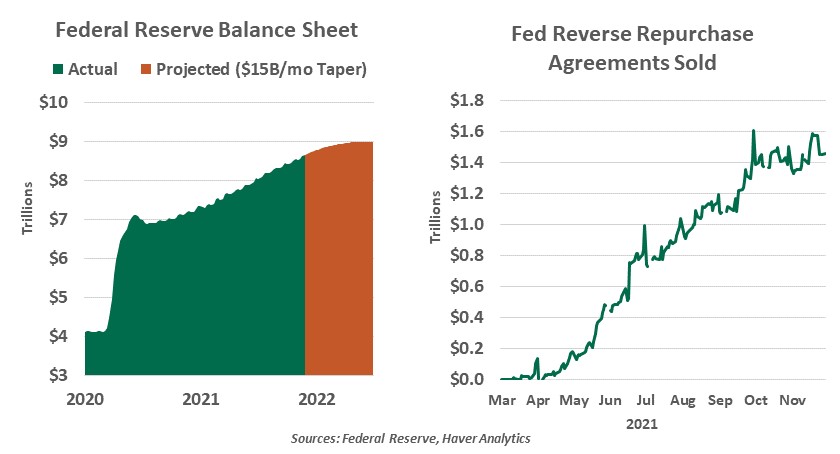

In November, the Fed made its long-awaited taper announcement. However, its scope was limited. Asset purchases would be curtailed by $15 billion per month in November and December, with no indication of the pace that would be followed thereafter.

If the Fed maintains the current taper rate, asset purchases would conclude in June 2021. The open-ended scheduling statement gave the Fed an option to speed up or slow down the process if market conditions require. One month after the announcement, acceleration may be in order.

Economic measures are coming in strong. Despite supply chain challenges, consumer spending and corporate profits are elevated, and initial jobless claims have fallen even lower than their pre-pandemic levels. Inflation remains too high. These circumstances suggest that the Fed should plan for rate hikes. Completing the taper is a prerequisite for raising rates, so as to avoid easing with one policy tool while tightening with another.

|

A faster taper should not cause disruption. |

Testimony by Fed Chair Jerome Powell this week made this a less speculative matter, as he acknowledged inflation has not been transitory and told the Senate Banking Committee that tapering may finish “a few months sooner” than the original June target date. Other Fed governors made similar allusions in speeches over the past two weeks. We can be sure this will be a leading topic of discussion at the December 14-15 meeting of the Federal Open Market Committee.