Chief Economist Scott Brown discusses current economic conditions.

As was widely expected, the Federal Open Market Committee announced the tapering of its monthly pace of asset purchases. The criteria for the lift-off in short-term interest rates is more stringent, but as Chair Powell admitted in his press conference, reaching full employment by the second half of next year is “certainly within the realm of possibility.”

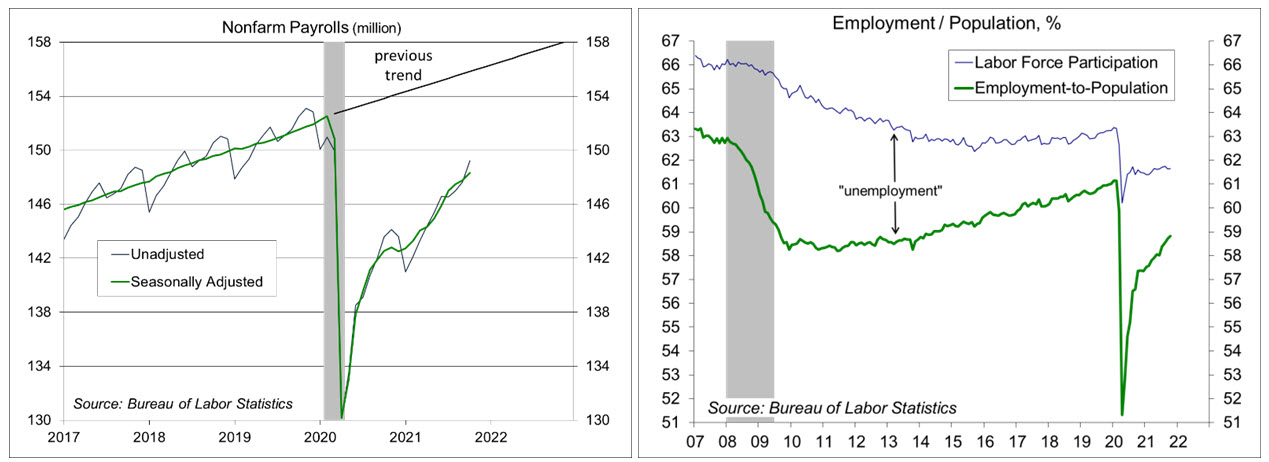

Nonfarm payrolls rose more than expected in October, up +531,000, with a net upward revision of 235,000 to August and September (leaving the three-month average at +443,000). The economy added 1.558 million jobs prior to seasonal adjustment (+579,000 in education, +218,500 in retail trade, +177,600 in temp help, +97,300 in transportation and warehousing). Hiring in education was less than a typical October, which translates to a 48,000 seasonally adjusted decline. Leisure and hospitality added 28,000 before adjustment, up 164,000 after adjustment. In addition, the birth/ death model, which forecasts job gains in new businesses (unobservable to the BLS), added 363,000 to the unadjusted total (same as a year ago). There’s a lot of noise in the adjustment payroll figure (statistic uncertainty, seasonal adjustment issues, etc.), but the underlying trend in payroll growth remains strong (a +666,000 average for the last six months). Note that upward revisions to previous figures are the norm in a recovery.

The unemployment rate fell to 4.6%, from 4.8% in September and 6.9% a year ago. However, labor force participation was unchanged at 61.6%, the same level as a year ago. A tight labor market and higher wages should pull people off the sidelines and back into the workforce. Increased participation may come over time, but there are limited signs of that so far. Early retirees are unlikely to return. Dependent care remains a critical issue (childcare is more limited and more expensive than before the pandemic). One way to increase labor force participation is to offer incentives for workers not to exit.

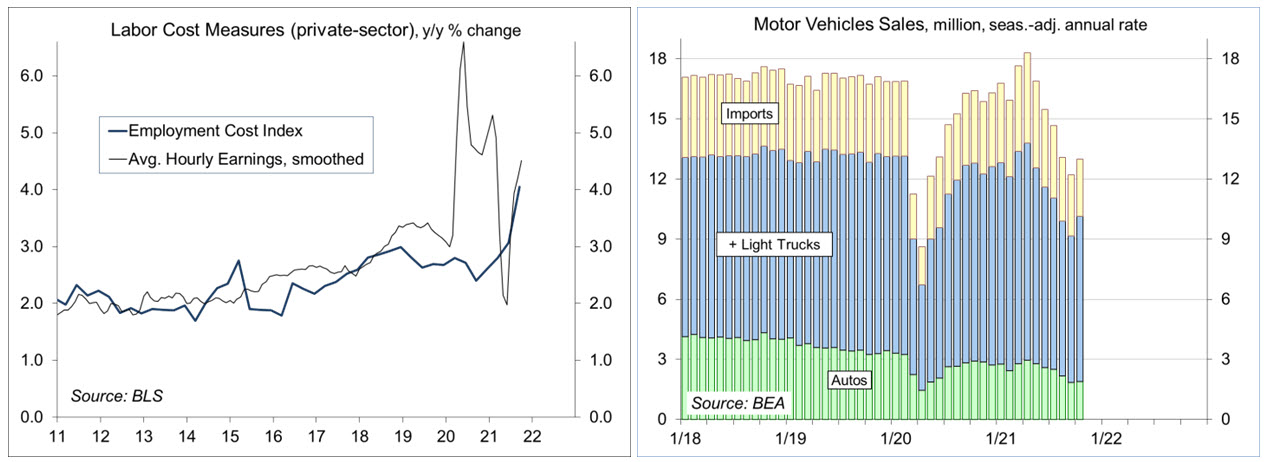

Average hourly earnings rose 0.4% in October, up 4.9% y/y, but these figures are not the best measure of labor costs (the Employment Cost Index for private industry workers, released October 29, accelerated to 4.1% y/y in September). The pandemic was like a splash of cold water in the face to many low-wage workers. They see friends and relations getting better jobs and are more likely to seek (and get) higher wages at new jobs (stay, and you may receive a minimal cost-of-living adjustment).

Is his press conference following the FOMC meeting, Fed Chair Powell said that there is no evidence of a wage-price spiral (higher wages leading to higher prices leading to higher wages, and so on). The increase in inflation this year is primarily due to supply and demand imbalances. “Bottlenecks and supply chain disruptions are limiting how quickly production can respond to the rebound in demand in the near term,” Powell noted, “as a result, inflation is running well above our 2% longer-run goal.” The supply constraints “have been larger and longer lasting than anticipated” and the Fed’s baseline expectation is that “supply bottlenecks and shortages will persist well into next year.” The Fed’s policy tools cannot ease supply constraints. Fed policymakers (and most economic forecasters) believe that the economy will adjust to supply and demand imbalances over time, “and as it does, inflation will decline to levels much closer to 2%.” Still, if the Fed were to see signs that inflation and inflation expectations were moving “materially and persistently” beyond levels consistent with the Fed goal, “we would use our tools to preserve price stability.”

Wage inflation follows price inflation. It does not cause it. That said, faster wage growth, combined with rising inflation expectations, may reinforce a higher inflation trend. This appeared to be the case in the Great Inflation of the 1970s and early 1980s. OPEC oil price shocks lifted consumer price inflation. Wage increases followed and inflation became embedded in the labor market. The Volcker Fed engineered a recession in the early 1980s to wring inflation expectations lower, not without some cost (higher unemployment). The lesson taken was that the Fed should act preemptively (that is, raise short-term interest rates) to head off future inflation before it gets out of control. Last year’s changes to the Fed’s monetary policy strategy has thrown that out.

The Fed’s criterion for raising rates is inflation moderately above 2% (to make up for sub-2% inflation in recent years) and maximum sustainable employment. There is no precise definition of “full employment.” It’s not a specific unemployment rate. It’s a judgement call based on a wide range of labor market indicators. Asked if it’s possible or even likely that full employment could be achieved by the second half of next year, Powell responded that if this year’s pace of improvement were to continue, “then the answer would be yes.” Powell emphasized that “the time for lifting rates and beginning to remove accommodation will depend on the path of the economy,” but “we think we can be patient.”

Recent Economic Data

As expected, the Federal Open Market Committee announced reduction (“tapering”) in its monthly pace of asset purchases (-$15 billion per month beginning in mid-November). The FOMC noted that supply and demand imbalances have contributed to elevated inflation, but these factors are “expected to be transitory.”

The October Employment Report was stronger than anticipated. Nonfarm payrolls rose by 531,000 (+1.56 million before seasonal adjustment), with a net upward revision of +235,000 to August and September.

Click here to enlarge

The unemployment rate fell to 4.6% (from 4.8% in September and 6.9% a year ago). Labor force participation held steady at 61.6%, the same level as a year ago.

Average hourly earnings rose 0.4% (+4.9% y/y). This measure is subject to distortions from the changing composition of employment. However, the ECI, released October 29, showed a pickup in labor costs.

Click here to enlarge

Motor vehicle sales rose to a 13.0 million seasonally adjusted annual rate in October, vs. 12.2 million in September and 16.4 million a year ago. Sales appears to come out of (already lean) inventories.

The ISM Manufacturing Index edged down to 60.8 in October (vs. 61.1 in September). The ISM Services Index rose to a record 66.7 (vs. 61.9). Both reports indicated strong demand and ongoing supply chain issues.

Gauging the Recovery

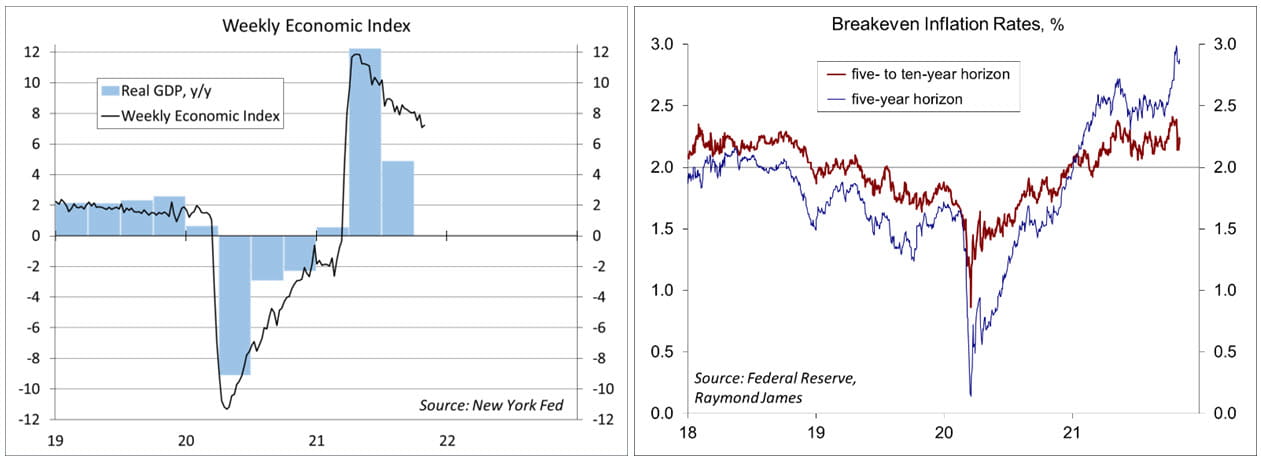

The New York Fed’s Weekly Economic Index edged up to +7.23% for the week ending October 30, vs. +7.07% a week earlier (revised from 6.85%). The WEI is scaled to y/y GDP growth (+4.9% y/y in 3Q21).

Click here to enlarge

Breakeven inflation rates (the spread between inflation-adjusted and fixed-rate Treasuries) continue to suggest an elevated near-term inflation outlook. The 5- to 10-year outlook remains receded in the latest week, reflecting the belief that the Fed will raise rates sooner to keep inflation in check.

Click here to enlarge

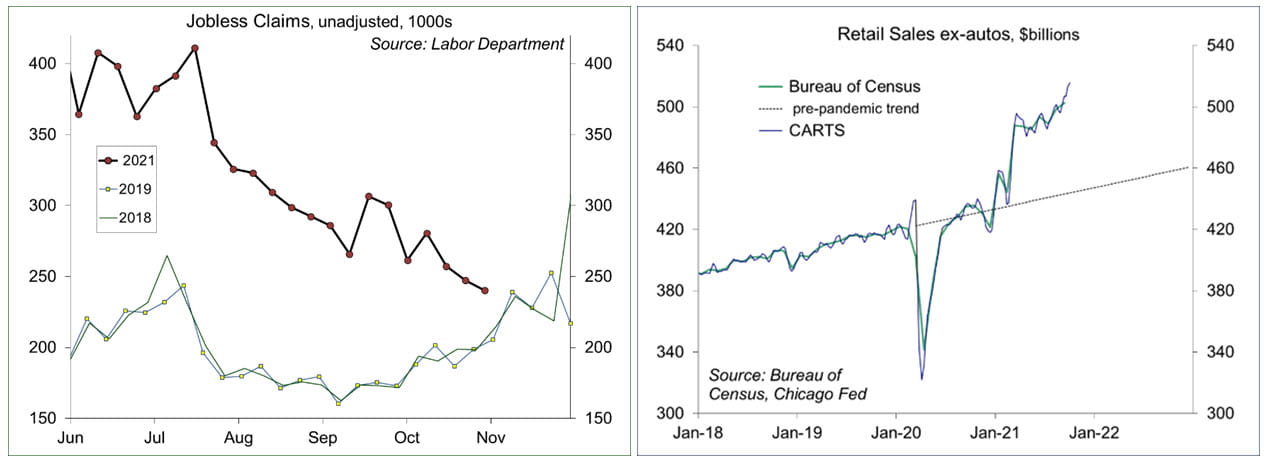

Chicago Fed Advance Retail Trade Summary (CARTS): up 0.2% in the second week of October, following a 1.2% gain in the previous week. October retail sales (ex-autos) were projected to rise 2.3% from September. Jobless claims fell by 14,000, to 269,000 (another pandemic low) in the week ending October 30. Unadjusted claims are quickly approaching pre-pandemic level, consistent with a tight labor market.

The University of Michigan’s Consumer Sentiment Index edged up to 71.7 in the mid-month assessment for September (vs. 71.4 at mid-month and 72.8 in August). Inflation expectations rose. The report noted that “the positive impact of higher income expectations and the receding coronavirus has been offset by higher rates of inflation and falling confidence in government economic policies.”

The opinions offered by Dr. Brown are provided as of the date above and subject to change. For more information about this report – to discuss how this outlook may affect your personal situation and/or to learn how this insight may be incorporated into your investment strategy – please contact your financial advisor or use the convenient Office Locator to find our office(s) nearest you today.

This material is being provided for informational purposes only. Any information should not be deemed a recommendation to buy, hold or sell any security. Certain information has been obtained from third-party sources we consider reliable, but we do not guarantee that such information is accurate or complete. This report is not a complete description of the securities, markets, or developments referred to in this material and does not include all available data necessary for making an investment decision. Prior to making an investment decision, please consult with your financial advisor about your individual situation. Investing involves risk and you may incur a profit or loss regardless of strategy selected. There is no guarantee that the statements, opinions or forecasts provided herein will prove to be correct.

© Raymond James

Read more commentaries by Raymond James