Chief Economist Scott Brown discusses current economic conditions.

Treasury reported a federal budget deficit of about $2.8 trillion (about 12% of GDP) for FY21. Barring a major unforeseen event, the deficit will fall considerably next year. By itself, that will be a negative for GDP growth, but a further strengthening in private- sector demand should more than offset that. Meanwhile, production bottlenecks, supply chain issues, and tight labor market conditions have continued to add to inflation pressure, altering the intermediate-term outlook for Fed policy. On Thursday, the Bureau of Economic Analysis will report the advance estimate of 3Q21 GDP growth. Details of that report will help to gauge the strength of the economy in the near term.

The budget deficit for FY21 (which ended in September) was $2.772 trillion (12% of GDP), down from $3.1 trillion (15% of GDP) in FY20. In July, the Congressional Budget Office projected that the budget deficit would fall to $1.1 trillion in FY22 (about 4.6% of GDP, which is about where we were before the pandemic). That doesn’t include the infrastructure bill, although additional spending would be spread out over time. As with the response to the 2008 financial crisis (when the deficit rose to 10% of GDP), the deficit will fall as the economy recovers.

At the end of September, the national debt stood at $28.4 trillion, about 120% of Gross Domestic Product. Debt is what economists call a stock ($), while GDP is a flow ($ per time), so there’s not much meaning in that comparison (other than as a benchmark). Of the national debt, $22.3 trillion (about 98% of GDP) is marketable debt (debt held by the public), while $6.1 trillion is debt that the government owes itself (Social Security and Medicare Trust and government retirement funds). Over the next few decades, much of the intergovernmental holdings will become marketable debt as the government taps into the Trust funds.

The government is not like a household or business. The federal debt does not need to be paid off by our kids and grandkids. In fact, since Treasuries are the benchmark for the global bond market, we wouldn’t want to have zero government debt. We only need to be able to roll over debt and make interest payments. No problem there. The last time borrowing was a concern was in the late 1980s and early 1990s (Japan was a big buyer of U.S. debt and started to balk, sending bond yields higher -- Presidents Bush the first and Bill Clinton signed legislation to reduce the budget deficit and bond yields fell). Economists’ attitudes toward the deficit have evolved. The current view is that there is a lot more leeway in running deficits. The budget deficit and federal debt do not cause inflation. However, fiscal stimulus adds to demand and supply is currently constrained.

On November 3, the Federal Open Market Committee is expected to announce a tapering of the monthly pace of asset purchases (currently $120 billion per month), although there is a small chance that the decision could be delayed until the December 14-15 policy meeting. Tapering (a $15 billion reduction in asset purchases each month) would last until the middle of next year, after which the size of the balance sheet would be held steady.

The federal debt and the Fed’s balance sheet are nothing to lose sleep over. However, lawmakers should eventually work to get the deficit on a more even keel. It was on an unsustainable trajectory before the pandemic, but there is no rush.

Supply chain issues have been more significant and appear likely to linger into 2022. While millions remain out of work, labor market conditions are tight, adding to cost pressures. A shift in demand from services to goods has contributed to these strains. Inflation expectations are rising

– a key concern for the Fed. Raising short-term interest rates now would not help to relieve supply chain issues, but the financial markets have continued to price in an earlier lift-off in short-term rates down the road. The federal funds futures market is now pricing in a rate hike next year and more than a 50% chance of a rate hike by June.

The advance estimate of 3Q21 GDP growth is expected to show a moderation in growth relative to the first half of the year, reflecting impacts from the Delta variant and the semiconductor shortage. Inventories are a key uncertainty and could have a large impact on the headline figures. The contribution from the change in inventories is confusing to most people. Inventories are a stock ($), while GDP is a flow ($/time). The change in inventories contributes to the level of GDP. The change in the change in inventories contributes to GDP growth. In other words, inventories will add to GDP growth if they fall at a slower pace. At this point, the change in inventories would add more than three percentage points to GDP growth if they simply stop falling. They likely fell further in 3Q21, but at a slower pace. Looking ahead, supply constraints may continue to restrain GDP growth over the near term.

Recent Economic Data

The Fed’s Beige Book described growth as “modest to moderate,” constrained by “supply chain disruptions, labor shortages, and uncertainty around the Delta variant.” Labor growth was dampened by “a low supply of workers” and firms reported high turnover (as workers left for other jobs or retired). Most Fed districts reported “significantly elevated prices, fueled by rising demand for goods and raw materials,” while more firms indicated a greater ability to pass higher costs along.

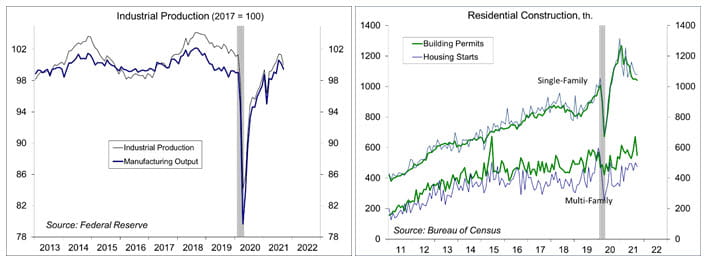

Industrial production fell 1.3% in September, reflecting lingering effects of Hurricane Ida and ongoing supply constraints (especially in autos). Manufacturing output fell 0.8% (+5.1% y/y), with motor vehicle production down 7.2% (-13.7% y/y). Ex-autos, factory output slipped 0.3%, with mixed results across industry.

Click here to enlarge

Building permits fell 7.7% in September to a 1.589 million seasonally adjusted annual rate (unchanged from a year ago), reflecting the usual volatility in multi-family activity. Single-family permits, the key figure in the report, slipped 0.9% (-7.1% y/y). Housing starts fell 1.6% (single-family starts were unchanged).

Despite supply bottlenecks, increased prices of materials, and affordability concerns, homebuilder sentiment (the National Association of Home Builders’ Housing Market index) rose four points to 80 in October.

Click here to enlarge

Existing home sales rose 7.1% in September, to a 6.29 million seasonally adjusted annual rate (-2.3% y/y). The increase was in line with the 8.1% surge in the Pending Home Sales Index. The supply of available homes for sale had ticked up in July and August (although still very tight).

Gauging the Recovery

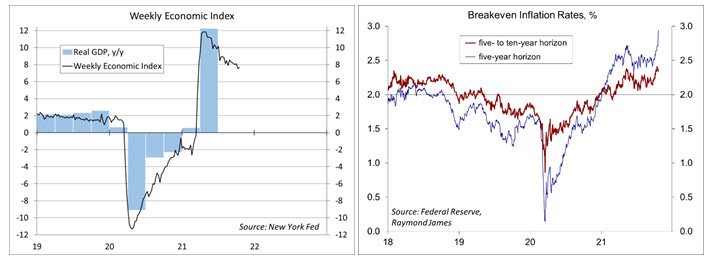

The New York Fed’s Weekly Economic Index edged up to +7.67% for the week ending October 16, vs. +7.54% a week earlier (unrevised). The WEI is scaled to y/y GDP growth (- 2.9% y/y in 3Q20).

Click here to enlarge

Breakeven inflation rates (the spread between inflation-adjusted and fixed-rate Treasuries) continue to suggest an elevated near-term inflation outlook. The 5- to 10-year outlook remains consistent with the Fed’s long-term goal of 2%, but the level is near the top of its recent range.

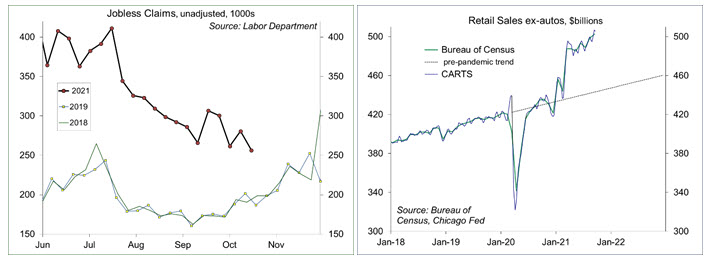

Jobless claims fell by 6,000, to 290,000 (a pandemic low) in the week ending October 16. Unadjusted claims are approaching the pre-pandemic levels of 2018 and 2019, consistent with a tight labor market.

Click here to enlarge

Chicago Fed Advance Retail Trade Summary (CARTS): down 0.2% in the fourth week of September, following a 1.4% gain in the previous week. September retail sales (ex-autos) were projected to rise 0.9% from August (the government reported a 0.8% increase).

The University of Michigan’s Consumer Sentiment Index fell to 71.4 in the mid-month assessment for September (vs. 72.8 in August and 70.3 in July). The report noted declining confidence in economic policies (budget process, debt ceiling), with decline across income, age, and political affiliations.

The opinions offered by Dr. Brown are provided as of the date above and subject to change. For more information about this report – to discuss how this outlook may affect your personal situation and/or to learn how this insight may be incorporated into your investment strategy – please contact your financial advisor or use the convenient Office Locator to find our office(s) nearest you today.

This material is being provided for informational purposes only. Any information should not be deemed a recommendation to buy, hold or sell any security. Certain information has been obtained from third-party sources we consider reliable, but we do not guarantee that such information is accurate or complete. This report is not a complete description of the securities, markets, or developments referred to in this material and does not include all available data necessary for making an investment decision. Prior to making an investment decision, please consult with your financial advisor about your individual situation. Investing involves risk and you may incur a profit or loss regardless of strategy selected. There is no guarantee that the statements, opinions or forecasts provided herein will prove to be correct.

© Raymond James

Read more commentaries by Raymond James