Editor’s note: Carl Tannenbaum and the Northern Trust Economics Team were recently honored with the Lawrence Klein Award for forecasting. The recognition, co-sponsored by the Blue Chip Economic Consensus, goes each year to the panelist who produced the most accurate projections over the past four years.

Carl was invited to offer some thoughts at the award ceremony on October 11. An abridged and augmented version of those remarks follows.

When I was notified that Northern Trust would be recognized with this year’s Lawrence Klein award, I laughed with surprise. We work hard at the forecasting process, but there are many others who are far better at it than we are. I have to suspect that the strange patterns produced by the pandemic leveled the playing field a bit. Or as my son generously observed: even a stopped clock is right twice a day.

When I related the news to my wife, she also laughed with surprise. My predictions in other arenas…such as when Sunday dinner will be on the table…are fraught with inaccuracy. But whether at home or at work, I have learned that if you keep at it long enough, you may occasionally hit the mark.

Northern Trust’s forecasting process is hardly a one-man show. I am very grateful to my teammates in the Economics Department, Ryan Boyle and Vaibhav Tandon, whose insights are essential to our effort. The two of them certainly deserve no small share of the recognition that has come our way.

More broadly, we benefit from interactions with a broad range of partners at Northern. Their views on economics and markets have an important influence on our thinking; it is a real treat to work within a community that places a high value on the collective intelligence.

That tone comes from the top. I am indebted to Rick Waddell and Mike O’Grady, the Chairmen at Northern that I have been privileged to serve. They’ve created a context that is conducive to our success. I also inherited a tradition of economic excellence from my immediate predecessors, the late Bob Dederick and Paul Kasriel (a Klein award winner himself), who set a high bar at Northern Trust that we work hard to clear every day.

As you’ve gathered from my introductory passages, I don’t consider myself an overly accurate forecaster, Klein Award notwithstanding. Because of that, I’ve often focused on out of consensus scenarios, the study of which can be very illuminating. The results feed naturally into risk management, which has been a focal point for my career, and for the careers of many economists.

So rather than working through an overview of our forecast for 2022, I thought I would use my prepared remarks to highlight some of the themes that we are tracking that could push us away from a central tendency. Resolutions on each of these fronts will have a critical impact on results.

Public Health

For most of my career, public health has not been of much interest to economic forecasters. AIDS, SARS, and MERS, while highly impactful for the affected communities, did not do material damage to global commerce.

COVID-19 changed all of that. Many of us have been learning far more about epidemiology in the last two years, becoming familiar with r factors (describing the rate of contagion) and vaccine efficacy rates. Since early 2020, the course of the pandemic has determined the course of the global economy and economic policy, and continues to do so today.

Happily, COVID-19 is in something of a retreat in many parts of the world after a mid-summer flare up. Vaccinations are expanding, and the Delta variant is receding. It has been tempting to declare that the worst is behind us.

|

COVID-19 anywhere is a risk everywhere.

|

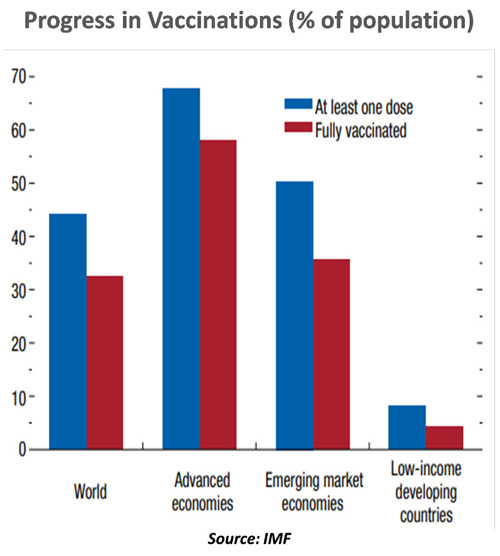

But a cursory reading of the history reveals that viruses of this kind rarely sit still. Mutation is almost constant; if populations are lucky, those mutations will be more benign than pernicious. Only about 36% of the global population has been vaccinated, and many of those have been covered by products that are less than fully effective. And many countries in the developing world have frighteningly low vaccination rates.

Given its proven ability to travel with relative ease (something still denied to most humans), COVID-19 anywhere is a threat everywhere. And while governments have largely abandoned zero tolerance policies in favor of “learning to live with the virus,” the risk of falling ill will still influence consumption and labor force participation around the world. I suspect that infection and vaccination rates will continue to be standard entries in our chart packs for some time to come.

The long term consequences of the pandemic on the locus and nature of work, and on the way economies organize themselves, are just beginning to take form. We may never return to old norms; models and perceptions rooted in those norms will have to be updated.

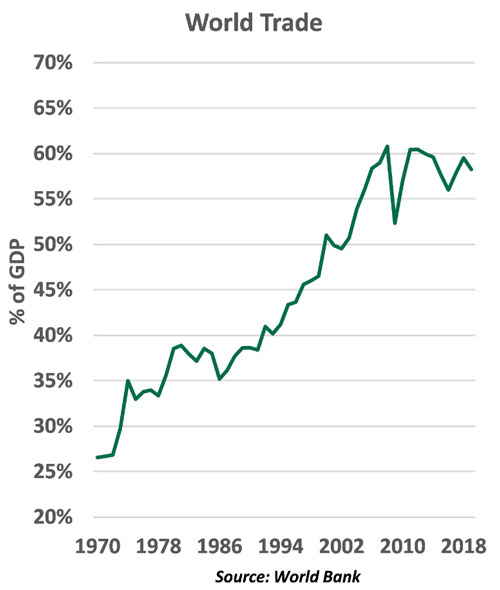

Globalization: In Retreat

The pandemic has at once shown the importance of globalization and its weaknesses. International collaboration to manage the pandemic has been essential, but the disruption caused by COVID-19 has many countries looking inward.

Chains come in a range of sizes: links of those tethered to the anchors of aircraft carriers can weigh well over 100 pounds, while those used in necklaces are barely a centimeter thick. The past two years have illustrated that economic supply chains are far more brittle than we may have suspected. Just-in-time production and logistics systems do not deal well with stress.

Add to that the sharp swings in both supply and demand that have occurred in the last 18 months, and you have a recipe for the severe bottlenecks we are dealing with today. These are proving especially costly on many levels, and may linger for much longer than anticipated. The resulting impact on inflation is one which will absorb no small amount of time on central bank agendas in the coming year.

|

Expect supply chains to get shorter in the years ahead.

|

The pandemic also highlighted the immense dependence that Western nations have on output from China and Southeast Asia. From semiconductors to personal protective equipment, this reliance has been a source of frustration and discomfort. This sentiment dovetails with the rising levels of economic nationalism that have been on prominent display for well over a decade now.

A movement away from unfettered globalization seems well underway; the question is: how far will it go? As the world’s economic geography shifts, so will growth, employment, and inflation. And that could produce challenges for debt sustainability and corporate profits, among other things.

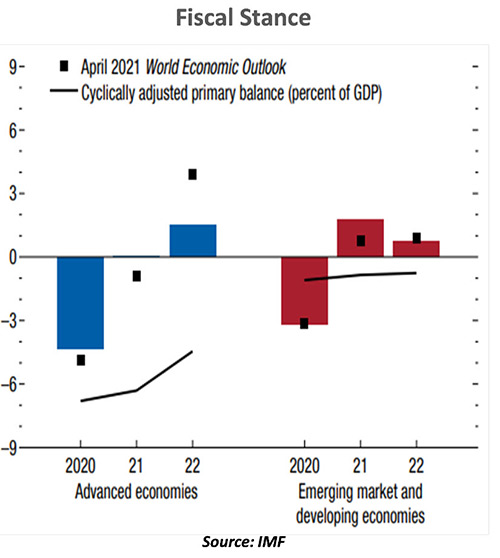

Policy Retreat

Fiscal and monetary policy moved with both size and speed to address the challenges presented by the pandemic. While there are certainly examples where programs were less successful, this is a situation where judging policy in retrospect is very, very difficult. When you’re “in the movie,” as they say, the ending is still unclear.

With the global economy nearing a full, but somewhat uneven recovery, calibrating the retreat from crisis-era policy will be no less challenging. Pulling back prematurely could leave the recovery incomplete; staying too accommodative for too long could one day stress investor appetite for sovereign debt. Organic private demand is improving from its pandemic lows, but most economies will be facing some degree of fiscal drag in the years ahead.

Over the long term, government spending that produces a sufficient increment in economic activity will have an easier time attracting financing. Unfortunately, politics complicate the process of program design, and the gap between parochial estimates of fiscal multipliers is wide enough to drive a truck through. (If you are fortunate enough to find a driver for the truck in this environment.)

Monetary policy has certainly done its part; to some, it has done more than enough. The cooperation between central banks and legislatures was essential during the depth of the pandemic; at some point, the two may need to go their separate ways.

Assessing the level of long run inflation is very complicated at the moment. Even more complicated is the task of identifying inflation’s root causes. The empirical relationship between money growth and inflation has reversed; Phillips Curves have flattened; and a recent Federal Reserve paper casts doubt (in very blunt terms) about the role of inflation expectations. It feels as if our understanding of how inflation evolves has become unmoored; without sufficient theoretical tethers, it may be difficult to know when inflation itself has become unmoored.

|

Monetary and fiscal policy will turn into headwinds next year.

|

What is a bit more clear is that there is ample liquidity in the system, and many asset prices in many countries appear to be in the upper reaches of their valuation ranges. Quantitative easing is intended to work through the “portfolio channel;” I wonder if investors realize that quantitative tightening works the same way.

As the expansion continues, we expect the community of central banks moving away from balance sheet growth and the zero lower bound to expand in the year ahead. Appropriately previewed and formulated, the retreat should not come at a great cost to market performance.

Accelerated Adoption

The changing nature of inflation is partly due to the advance of technology, the fourth of the major themes I’d like to touch on. My friend Martin Fleming, the retired chief economist of IBM, refers to what’s going on in this space as the fourth industrial revolution.

My wife and I recently took a trip to Arizona to celebrate a milestone birthday. At almost every turn, we were able to use technology that saved time and improved our experience. But while this undoubtedly added to the value of our leisure time, it wasn’t clear how accretive it was to gross domestic product (GDP). As Robert Solow said more than thirty years ago, the computer age is everywhere, except in the productivity statistics.

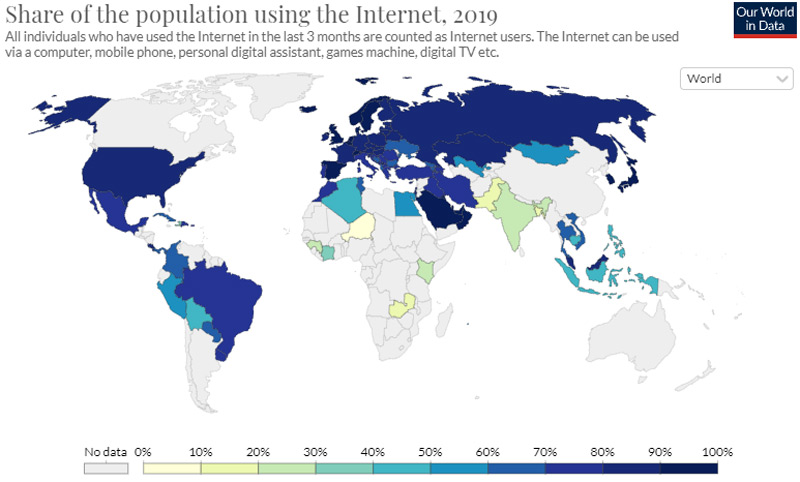

The pandemic led more of us to do more things more often virtually, accelerating movement down the adoption curve that is unlikely to reverse. The resulting boost to automation and e-commerce is changing cost and pricing structures in ways that we are only beginning to comprehend.

Access to technology around our country and around the world is uneven. Broader access could be a great leveler; failure to provide it will exaggerate inequality.

Technology is certainly changing the nature of work and the skills required to do it. About 60% of Americans do not have a college degree, and that number is far more significant in developing countries. In a digitalizing world, those with more modest levels of education will face rockier paths to prosperity. If policy fails to address the disparity, support for economic systems may come under increasing question.

East And West

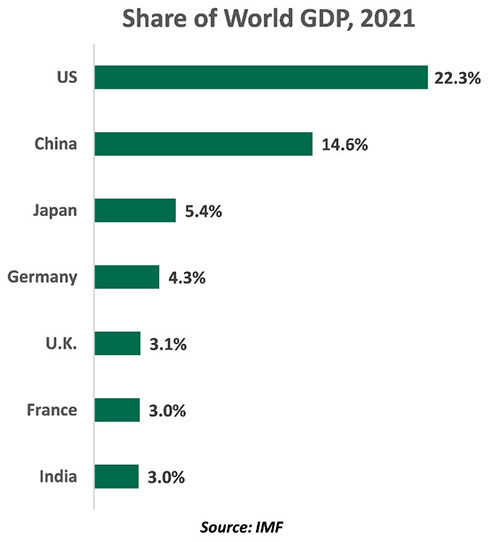

Finally, I want to comment on the bipolar nature of the global economy. I mean this in the literal sense; no offense to London, Frankfurt, or Sydney, but Beijing and Washington are the main centers of international influence. But the term also captures the dysfunction that characterizes the current relationship between those two capitals.

Both China and the United States believe it has an economic model worthy of emulation. Each would like to claim primacy in the realm of development aid. Each accuses the other of slights and transgressions that range from minor to much more serious. Each expects, and in some cases demands, allegiance from other countries, who find themselves caught uncomfortably in the middle.

|

There can be no winner in the battle between the U.S. and China.

|

Each is also deeply in debt, and in need of sustained investor interest. Each is trying to find a balance between capitalist incentives and what the Chinese have called “common prosperity.”

Both are facing significant demographic challenges in the decades ahead, challenges made worse by the impact of COVID-19 on life expectancy and birth rates. Immigration has also been a casualty of the pandemic, as countries close borders to prevent contagion. Beyond the world’s leading economic powers, the impact of demographics on economies is a topic that deserves more attention that it currently garners.

Ultimately, some level of collaboration between China and the United States will produce the best results for the global economy, and for global society. Harmony between the two will be essential to addressing climate change, which many see as a defining economic issue for the next generation.

It will also be critical to the success of international organizations such as the International Monetary Fund, the World Health Organization, the World Trade Organization, and others whose work remains critical to global development. Almost everyone has a stake in the competition between Washington and Beijing, which can have no clear winner.

For those of you hoping for a more detailed discussion of where GDP might be going next year, I apologize. Accounting for consumption, investment, and trade is important, but the narratives that weave through the national accounts have always been far more interesting to me. I look forward to digging into the stories that drive the economy for many years to come.

Information is not intended to be and should not be construed as an offer, solicitation or recommendation with respect to any transaction and should not be treated as legal advice, investment advice or tax advice. Under no circumstances should you rely upon this information as a substitute for obtaining specific legal or tax advice from your own professional legal or tax advisors. Information is subject to change based on market or other conditions and is not intended to influence your investment decisions.

© 2021 Northern Trust Corporation. Head Office: 50 South La Salle Street, Chicago, Illinois 60603 U.S.A. Incorporated with limited liability in the U.S. Products and services provided by subsidiaries of Northern Trust Corporation may vary in different markets and are offered in accordance with local regulation. For legal and regulatory information about individual market offices, visit northerntrust.com/terms-and-conditions.

© Northern Trust

Read more commentaries by Northern Trust