Last year, after our newly-adopted dog demonstrated her ability to jump over our fence, a neighbor shared a useful anecdote: “Every dog owner will utter the sentence: Wow, we’ve never seen him do that before!” Training is important, but we also must think quickly when confronted with new behavior.

We have uttered similar feelings of surprise and exasperation when digesting economic data since the COVID-19 crisis. Many measures have scaled the fences of our comprehension.

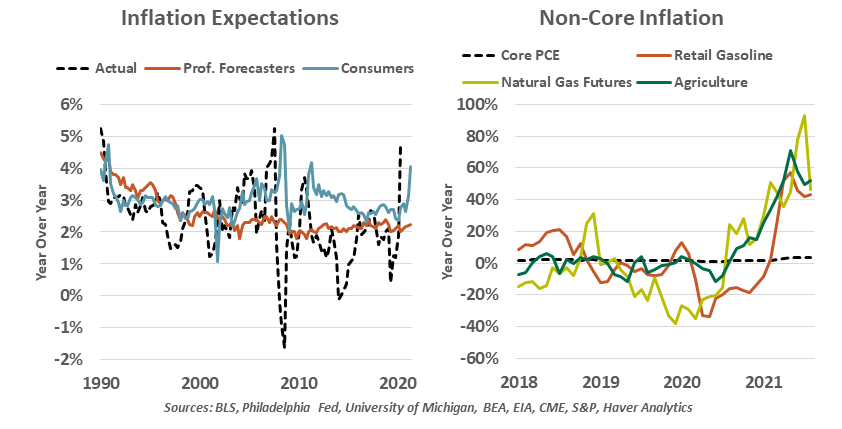

Inflation is one of them. Recent elevated readings on the price level have captured attention and required careful analysis. Economists have often turned to inflation expectations as a reason to look past any one month’s measure of inflation, but also as a guide for when inflation may come. Prices are more likely to rise when there is a widespread expectation of rising prices.

Last week, the practice of using inflation expectations as a guide to future inflation came under question from a researcher at the Federal Reserve. His paper was provocatively entitled: “Why Do We Think That Inflation Expectations Matter for Inflation? (And Should We?).”

The author argued that relying on expectations is “unnecessary and unsound…[and has] no compelling theoretical or empirical basis and could potentially result in serious policy errors.” A key takeaway was that, in a well-functioning economy, a typical person shouldn’t need to pay much thought to inflation. When asked to measure inflation, professional and lay survey respondents alike tend to overestimate it. Mainstream attention to inflation is a warning sign, and policymakers should manage inflation based on observed evidence, not expectations.

The Fed’s new average inflation target acknowledged this new understanding. Fed governors will need to see inflation measures stay above the target of 2% core inflation on a sustained basis; forecasts of inflation are secondary.

Inflation measures do not always reflect the inflation experience. If asked, it would be difficult for most of us to describe how 1% inflation feels different from 3%. We would think of changes to real prices, which can be concealed by relying on measures like core inflation.

Are inflation forecasts reliable enough to shape policy?

The Fed targets 2% growth in the personal consumption index less food and energy. This narrower index excludes the most volatile categories: Energy markets are subject to global supply and demand dynamics, while food prices can shift unpredictably for idiosyncratic reasons. On an academic basis, it makes sense to set them aside. But that approach ignores the means through which most people experience inflation.

The Fed targets 2% growth in the personal consumption index less food and energy. This narrower index excludes the most volatile categories: Energy markets are subject to global supply and demand dynamics, while food prices can shift unpredictably for idiosyncratic reasons. On an academic basis, it makes sense to set them aside. But that approach ignores the means through which most people experience inflation.

The price of a gallon or liter of gasoline is prominently advertised; utility bills may soon grow uncomfortable; changes to grocery and restaurant prices are readily observable. Dismissing them as “non-core” ignores an important element of how inflation affects consumer behavior.

The study of inflation has been a story of evolution. When inflation roared in the 1970s and 80s, there was a simple explanation: “Inflation is always and everywhere a monetary phenomenon.” However, the relationship between money supply and inflation has since broken down. We also once turned to the Phillips Curve, which expects lower unemployment to lead to higher wages and thus inflation. However, in the last cycle, unemployment held below 4% for nearly two years, yet the Phillips Curve stayed dormant, and inflation did not return. Now, economists are casting doubt over the use of inflation expectations as a leading indicator of actual inflation.

Inflation models have been easier to criticize than to create. If we are too quick to dismiss them, we can be left with no gauge for vital metrics. Some important forces, like sentiment and expectations and policy preferences, may not have a firm quantitative basis. That does not mean they should be ignored.

As she settled into her new home, our dog’s behavior became more predictable. Surprises, and occasional messes, are part of the journey. We hoped for a steadier experience to come, and after testing our patience, our expectations proved correct.

Information is not intended to be and should not be construed as an offer, solicitation or recommendation with respect to any transaction and should not be treated as legal advice, investment advice or tax advice. Under no circumstances should you rely upon this information as a substitute for obtaining specific legal or tax advice from your own professional legal or tax advisors. Information is subject to change based on market or other conditions and is not intended to influence your investment decisions.

© 2021 Northern Trust Corporation. Head Office: 50 South La Salle Street, Chicago, Illinois 60603 U.S.A. Incorporated with limited liability in the U.S. Products and services provided by subsidiaries of Northern Trust Corporation may vary in different markets and are offered in accordance with local regulation. For legal and regulatory information about individual market offices, visit northerntrust.com/terms-and-conditions.

© Northern Trust

Read more commentaries by Northern Trust