Over the past few months, the topic of inflation has been hotly debated – specifically, whether it will be transitory or persistent. In particular, much attention has been paid to short-term supply shocks, which the Fed and others have routinely cited as the explanation for the recent rise in prices. The distinction between transitory and persistent inflation is critically important, as Fed policy hinges on long-term expectations – their view will determine when they taper bond purchases and, ultimately, normalize interest rates.

Hard data about supply imbalances is supported by countless anecdotes, but these only paint a contemporaneous view of inflation and do not offer strong insight into whether the current surge is something we will be tackling months or years from now. The drivers are many and diverse, and the resolution of these drivers are less clear.

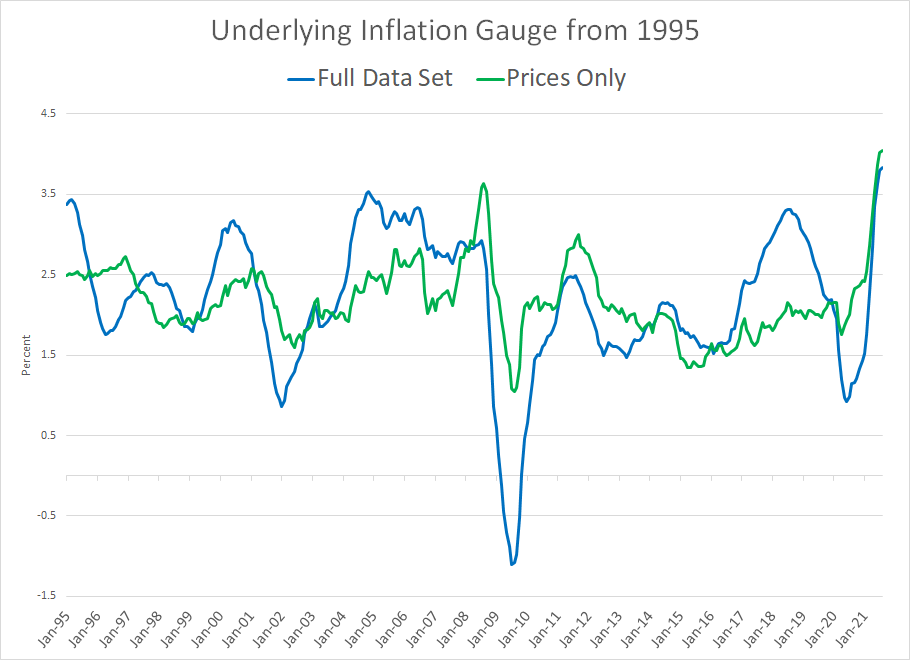

After combing through dozens of inflation indicators, we believe a single one emerges as the most accurate predictor of persistent inflation – the Underlying Inflation Gauge. We’ve discussed UIG previously, and we continue to feel it is the most reliable forward-looking indicator of macroeconomic activity for the coming months. It is published by the Federal Reserve Bank of New York, so even though it is little used by market participants, one can assume it is part of the Fed’s data arsenal, in addition to traditional metrics such as CPI, PPI, and the PCE Price Index.

According to the FAQ section of the New York Fed’s website, “UIG provides a measure of underlying inflation and is defined as the persistent part of the common component of monthly inflation.”

Source: FRBNY

As you can see from the above chart, the index is divided into two subindices – a “prices-only” measure which includes the subcomponents of CPI, and a “full data set” measure which includes CPI components plus a slew of “nominal, real, and financial variables.” Although the two measures generally move in the same direction, they have frequently disagreed in magnitude. At the moment, however, they are nearly identical – both sitting around 4% – which suggests the current inflation level likely has some staying power (the “prices only” index is 4.05%, and the “full data set” is at 3.84%). While the Fed has officially stated that they are willing to let inflation drift above 2% in the short run, we believe 4% is likely outside their comfort zone.

To conclude, the Fed has had access to this data since inflation became an issue earlier this year, but their public comments suggest they are not paying much attention to it. In fact, in their latest statement, on September 22, they wrote that “[i]nflation is elevated, largely reflecting transitory factors” – even though UIG tells a materially different story. Our recommendation is to respect the Fed’s words for their ability to move markets, and to respect their UIG data for reflecting the truth in the evolution of inflation.

© Osterweis Capital Management