In this Issue:

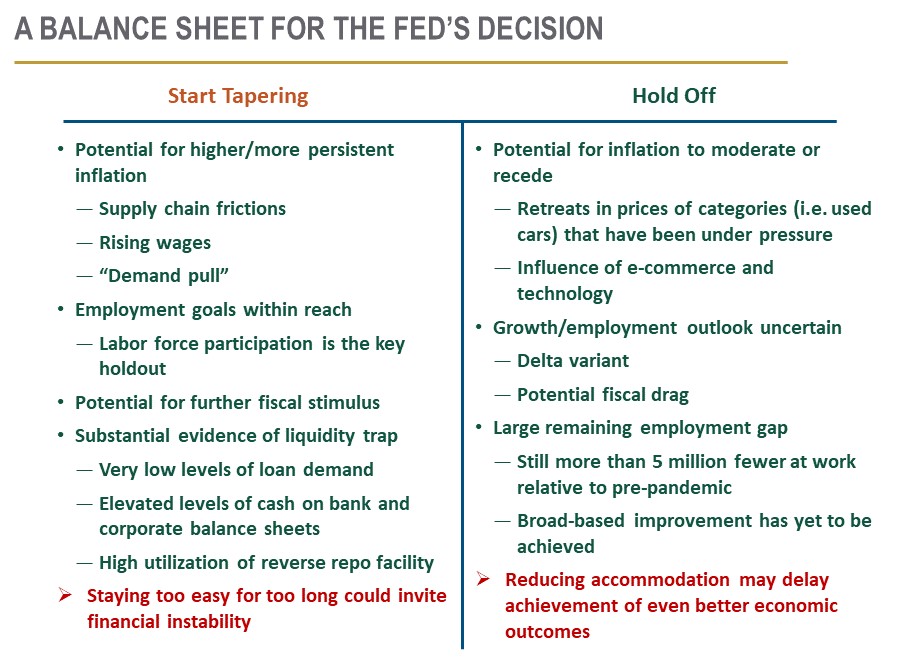

The Federal Open Market Committee (FOMC) will be gathering next week to take stock of monetary policy. The main question to be addressed is whether to begin reducing the central bank’s purchases of securities. The Bank of Canada began the tapering process earlier this year; the Reserve Bank of Australia and the European Central Bank both announced plans to follow suit earlier this month.

If we had a seat on the FOMC, we would be in favor of easing off of the accommodative policies, for the following reasons:

-

The growth outlook is strong. As reflected in our updated U.S. forecast, activity is expected to recover from a late summer slump. COVID-19 cases appear to have peaked, which should reduce hesitation among consumers to gather and travel.

-

Labor markets are on track to meet the Fed’s expectations. There are an immense number of job openings available, wages are rising, and unemployment benefits are shrinking. Those still on the sidelines should be back in the game soon.

-

Inflation risks are to the upside. Few think that the price level will continue increasing at a 5% annual pace, which it has over the past twelve months. But excesses of demand over supply and kinks in global supply chains may prevent inflation from settling down soon, or completely.

-

Liquidity in the financial system is more than sufficient. Credit demand is modest, and evidence of excess cash can be seen in many different places. Financial conditions are easy. Leaving too many reserves in the system could foster unwanted inflation in the prices of goods or assets.

-

The market is ready. The Fed has been dropping hints about reducing bond purchases for two months, and long-term interest rates haven’t budged. A repeat of the 2013 “taper tantrum” seems highly unlikely.

The statements and forecasts following next week’s conclave should set the stage for a tapering announcement at the November 2-3 FOMC meeting. The pace of tapering will start small and potentially increase over time. Interest rate increases are still at least a year off, although the Fed’s dot plot will likely show more members calling for more hikes sooner than they did in June.

Following are additional details on the factors the group will consider, with both sides of each issue presented.

Economic Growth

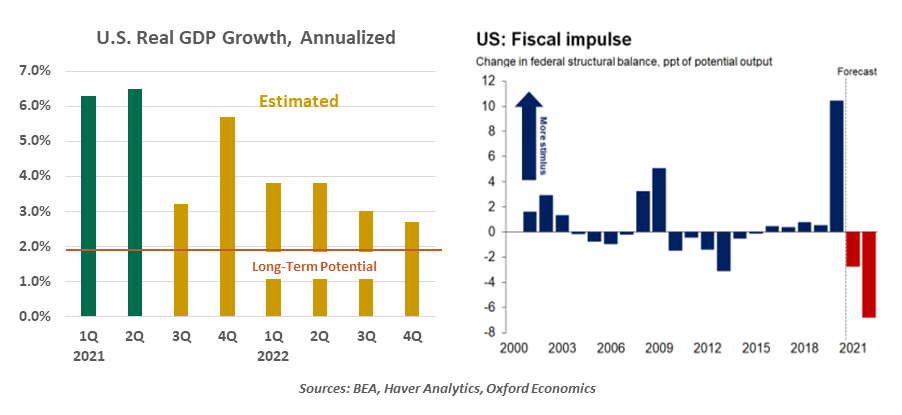

As measured by gross domestic product (GDP), recovery is complete, and expansion has begun. However, activity cooled a bit as summer concluded, leading some to wonder whether the outlook had grown cloudier. Has the business cycle only just begun, or is the end in sight?

|

The U.S. economic outlook remains positive.

|

|

Tailwinds

|

Headwinds

|

|

The Delta variant of COVID-19 curtailed activity in the late summer, but should ease as we move through the fall. Consumers still have substantial pent-up savings and demand, and further employment gains will provide additional means. Inventories in the U.S. economy are at very low levels, and will need to be rebuilt; this should keep producers very busy. Housing is likely to remain strong well into next year, and further fiscal stimulus could provide fuel for infrastructure.

|

American consumers may have used recent stimulus to place their financial houses into better order, so saving rates may not descend to pre-pandemic levels. Fiscal policy is likely to be a drag on the expansion over the next four quarters, with benefit programs ending; the tax increases proposed to pay for new fiscal initiatives may limit the benefit they will have on growth. COVID-19 will likely be a lingering threat, with periodic outbreaks interrupting economic activity.

|

Each component of GDP seems to have upside potential over the next four quarters. Strong investment performance over the past year will create wealth effects. Credit remains underutilized. The expansion has a lot of room to run.

Inflation

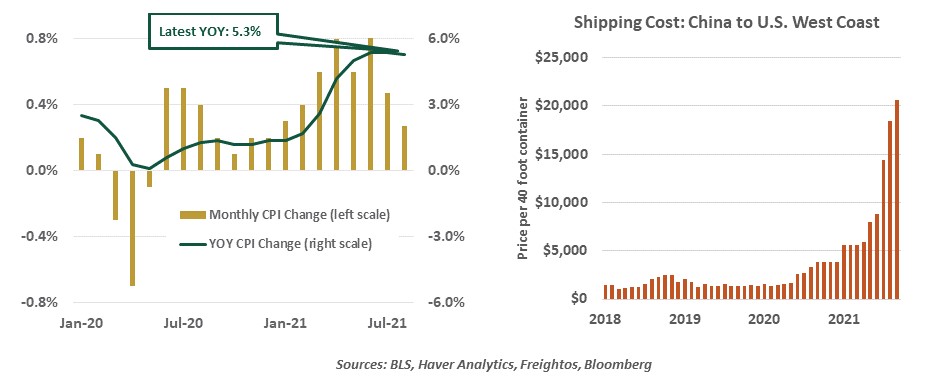

We know where inflation is today: too high. We know, generally, where inflation is heading in the year ahead: lower. But trying to refine those broad expectations is not easy.

Excesses of demand over supply have led the price level much higher over the last six months. Will inflation settle sufficiently, or will it be sustained at uncomfortable levels?

|

Wait and Watch

|

Act Now

|

|

An outsized portion of recent CPI increases have come from a handful of minor items (like used cars) which have already shown signs of easing. High prices are slowing demand and prompting additional supply, as they are supposed to.

Recent price jumps should be viewed as “level changes” that will not persist. In addition, the power of secular trends like e-commerce and technology should continue to place downward pressure on inflation. Inflation expectations remain reasonably well-anchored.

|

Wages are rising rapidly, and many U.S. workers are delaying re-entry to the labor force. The leverage currently commanded by labor could last longer than anticipated, putting persistent pressure on service prices. The cost of shelter will undoubtedly trend upward in sympathy with house prices.

Goods prices are being distended by bottlenecks in global supply chains that could take a very long time to untangle. And re-shoring may be gaining steam, bringing higher prices for a range of items.

|

|

Inflation should settle, but not quickly and not completely.

|

It isn’t easy to anticipate how the Fed will react to all of this. Last fall, the FOMC approved an updated policy framework that calls for inflation to average 2% over some period of time. There is no specific mention of what that interval is. The Fed further stated that it would base policy on actual levels and not forecasts; as Fed Chairman Jerome Powell said recently, “forecasters have a lot to be humble about.” But if actual data were the sole driver of policy decisions, recent inflation readings would have prompted a reaction by now.

As we covered in our piece on inflation’s past, present, and future, we believe that current pressure on prices will not be sustained. Some stresses were inevitable, given the speed with which the economy closed down last year and the speed with which demand recovered this year. But risks to inflation are clearly on the upside, and that should prompt corrective monetary action.

Employment

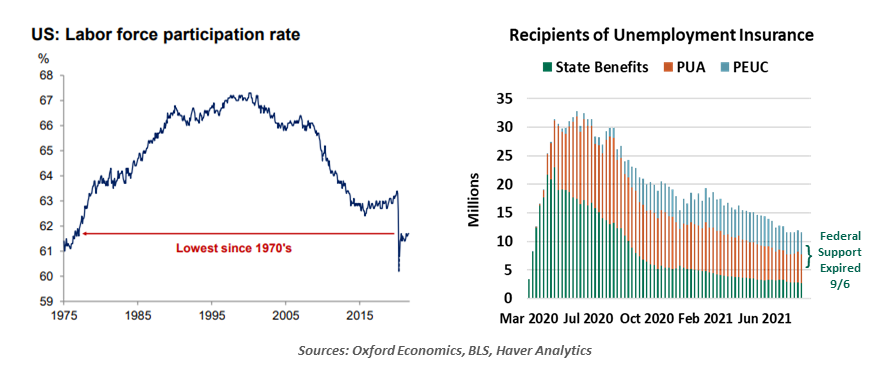

The onset of COVID-19 produced one of the largest labor market retreats ever seen. More than 22 million Americans were thrown out of work in March and April of 2020. Considerable progress has been made since then, but total employment is still more than five million below its pre-pandemic peak. That outcome is not for want of opportunities; at last count, there are almost 11 million open positions in the U.S. economy.

What does full employment look like, and how far are we from that objective?

|

There is every reason to think that full employment isn't far off.

|

|

Room to Improve

|

Already There

|

|

Job creation was very solid through mid-summer, but the August numbers were disappointing. September is likely to bring more of the same, given the lingering impact of the Delta variant on service businesses. The number of job openings is a misleading gauge of opportunity, given mismatches of skills and geography between seekers and employers.

Labor force participation remains at very low levels. While an estimated two million Americans say they have retired since the pandemic started, our research suggests that many of them cannot afford to stay that way. There is still some distance to travel before the job market is fully healed.

|

The latest wave of COVID-19 infections in the U.S. is easing, both overall and in the states which have been hardest hit. Public health restrictions and public hesitation about crowded spaces should ease in the months ahead; both will be very positive for hiring.

Several factors have combined to keep workers away from the labor force: COVID-19 concerns, children learning remotely, day care dislocations, and supplemental unemployment benefits. The significance of these factors is easing; in particular, federal unemployment payments ended earlier this month. Higher wages await those willing to get back to work. We expect broad-based increases in payrolls and participation in the months ahead.

|

Monetary and fiscal policy have combined to create very strong employment opportunities. In addition to the record number of job openings, a record number of workers are departing their current jobs for better ones. From here, the matching process needs time to operate; there isn’t much need for additional policy prompting.

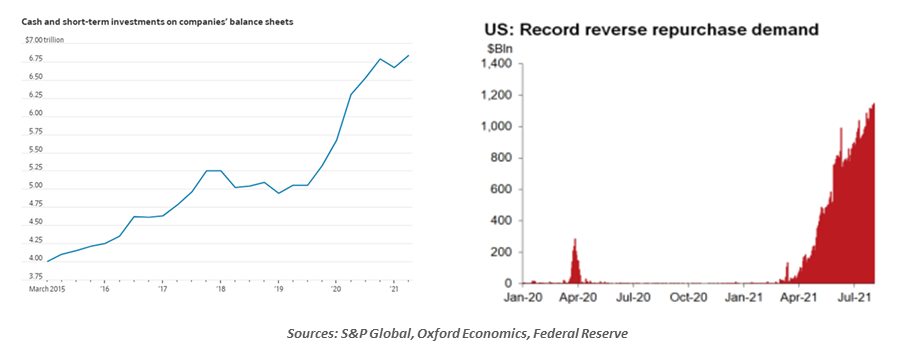

Liquidity

The Federal Reserve’s balance sheet has almost doubled in size since the pandemic started, an increase of $4 trillion. The question is whether those reserves are still having the desired effect.

|

Too Much

|

Not Enough

|

|

Multiple signals suggest that the financial system is awash in liquidity. Corporate balance sheets are flush with cash; banks are keeping a record volume of deposits with the Fed; and more than $1 trillion is being placed each day in the Fed’s reverse repurchase program. On the surface, this seems to provide clear evidence that quantitative easing has been overdone.

|

With interest rates close to zero, quantitative easing is the main avenue through which the Federal Reserve can pursue its policy goals. Since those goals haven’t yet been met (specifically on the employment side), bond purchases should press ahead. With the benefit of hindsight, some within the Fed regret tapering in 2014; fears over inflation turned out to be overdone.

|

|

Liquidity in the financial system is excessive.

|

The pandemic recession was sharp and sudden. The recovery from that recession has also been rapid, and yet Federal Reserve policy has not been adjusted. There is plenty of money out there to be borrowed if needed.

It is also worth noting that tapering is not tightening; asset purchases will be diminished, but the Fed’s balance sheet will still be increasing. Starting to taper early has the benefit of hastening the process of stopping growth in that balance sheet, which is what the Fed should be aiming for.

Information is not intended to be and should not be construed as an offer, solicitation or recommendation with respect to any transaction and should not be treated as legal advice, investment advice or tax advice. Under no circumstances should you rely upon this information as a substitute for obtaining specific legal or tax advice from your own professional legal or tax advisors. Information is subject to change based on market or other conditions and is not intended to influence your investment decisions.

© 2021 Northern Trust Corporation. Head Office: 50 South La Salle Street, Chicago, Illinois 60603 U.S.A. Incorporated with limited liability in the U.S. Products and services provided by subsidiaries of Northern Trust Corporation may vary in different markets and are offered in accordance with local regulation. For legal and regulatory information about individual market offices, visit northerntrust.com/terms-and-conditions.

Monetary and fiscal policy have combined to create very strong employment opportunities. In addition to the record number of job openings, a record number of workers are departing their current jobs for better ones. From here, the matching process needs time to operate; there isn’t much need for additional policy prompting.

Monetary and fiscal policy have combined to create very strong employment opportunities. In addition to the record number of job openings, a record number of workers are departing their current jobs for better ones. From here, the matching process needs time to operate; there isn’t much need for additional policy prompting.