Fundamentals over incidentals. What’s next for U.S. stocks after an impressive showing year-to-date? We encourage equity investors to focus on long-term fundamentals, not daily headlines, as their barometer. As year-end approaches, we see:

- Compelling value in equities relative to bonds

- Pent-up demand and pricing power providing support

- Market risk from the Delta variant as manageable

Market overview and outlook

The summer saw some reversal of the “reflation trade,” a strong uptrend by economically sensitive stocks that kicked off with vaccine announcements last November. Fears centered on the Delta variant and its potential economic impacts. Concerns that earnings, valuations and gross domestic product (GDP) growth are at or near peak levels also weighed heavy.

Company earnings have been stellar, especially among cyclicals, and the key driver of S&P 500 returns this year. Our view: Peaks are inevitable, but they don’t suggest a cycle’s end. We see strong underpinnings for equities in the months ahead, and advocate a focus on quality and stock selection to capture opportunities in those companies with solid underlying fundamentals.

"Starting points matter, so more muted return expectations are sensible at this stage of the market recovery. But we remain constructive on U.S. stocks."

Taking on the skeptics

While daily gyrations and headlines questioning the market’s grit can be sources of consternation, we remain optimistic on the medium-term outlook for U.S. stocks. The key components of an investment thesis ― earnings, fundamentals and valuations ― support a case for continued strength, even as longer-term return expectations should be tempered.

Earnings

The skeptic: They can only go down from here

Our take: The composition of earnings speaks to corporate resilience

Company earnings have been impressive by any measure. The S&P 500 in Q2 recorded the highest year-over-year earnings growth in over a decade. That may not seem like a high bar given dismal earnings last year amid the COVID-19 crisis and a powerful economic restart in 2021.

Perhaps more telling is the makeup of the earnings progress. Overall, companies have beat analyst expectations on both earnings per share (EPS) and revenue growth. But the latter has been particularly strong. This suggests to us that even as inflation has been driving an increase in input costs, companies have the pricing power to offset it. They have been able to raise prices and push higher costs on to the end consumer, a reflection of pent-up demand and consumer willingness to pay.

While the vast majority of companies have surprised to the upside and by a wide margin, the market reaction to the historically large beats has been undersized. Stock performance, especially among cyclicals, has not popped at a magnitude consistent with the beat. This suggests some skepticism among investors while also affirming that blockbuster results don’t necessarily receive bigger rewards from the market.

At the risk of stating the obvious, earnings have to slow from here. The data back to 2003 shows no historic precedent for sales growth to sustain at this level. But recent results demonstrate corporate dynamism: Companies successfully managed costs through the crisis period. They have weathered inflation equally well, and we’d expect cost pressures to abate as pandemic-dented supply rebuilds and demand normalizes.

In all, the likelihood for earnings to slow from historic peaks does nothing to sully our outlook on stocks.

Fundamentals

The skeptic: “Meme stock mania” suggests fundamentals are less important today

Our take: Fundamentals are real, measurable and always prevail in the end

Companies are feeling they can raise prices, and the level of revenue surprise is bearing this out. This is partly because consumer income and balance sheets are exceptionally strong and able to endure price increases. Personal savings saw a notable increase during the pandemic while consumer debt declined. Typically, economies see pent-up demand after a recession but an inability on behalf of the consumer to spend. This time, government infusions and reduced expenses during lockdowns helped to pad pocketbooks. More recent data from the Federal Reserve Bank of New York shows a second-quarter climb in household debt as mortgages and auto loans increased. Consumers are spending.

One optimistic sign from the bond market: Credit spreads ― the difference in yield between corporate bonds and Treasuries of comparable maturity ― are narrow. The limited yield differentiation between riskier and “risk-free” debt is a signal from the market that it sees a low probability of companies defaulting any time soon.

Valuations

The skeptic: They are unsustainably high

Our take: “High” is a relative term

U.S. stock valuations are high on a price-to-earnings (PE) basis, which values a stock relative to its prior or future earnings potential. We’d make two points on this front: First, analyses of PE multiples versus returns over different time horizons have shown that PE has little ability to predict near-term returns (think one to three years) but does have greater predictive power over the longer term (think five to 10 years). This makes sense in that EPS estimates are changeable and the shorter the horizon, the greater room for anomalies. This year will be such an outlier.

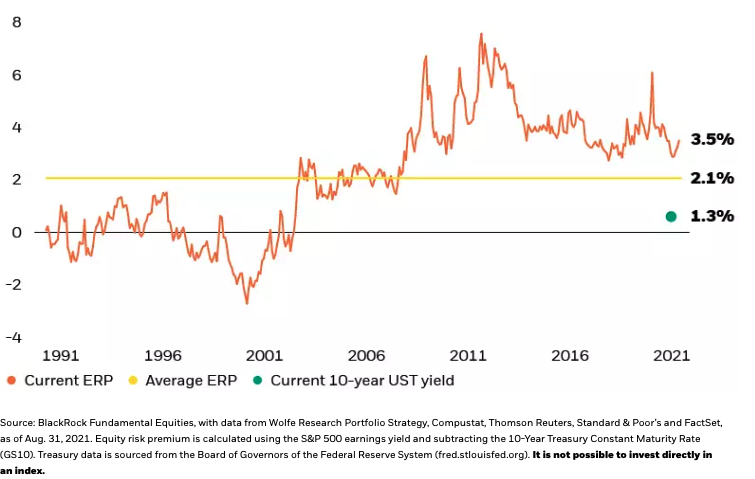

Second, we believe PE is a less informative measure than the equity risk premium (ERP), which values stocks based on the prevailing 10-year Treasury rate. The ERP gauges whether investors are compensated for the greater risk in equities versus “risk-free” government bonds. The ERP has been well above its long-term average for the past 10 years, suggesting stocks are undervalued for the relative risk/reward they offer.

We don’t see much room for change here. The 10-year Treasury yield would essentially have to double from its current level to compete with equities. As shown below, the ERP at the end of August stood at 3.5%, well above its 30-year average of 2.1% ― a gap of 1.4%. By our assessment, the 10-year Treasury yield would have to rise by that much before equity risk/reward would begin to lose its appeal relative to bonds. This would imply 10-year Treasury yields in the area of 2.7%.

Equity risk/reward still attractive vs. bonds

S&P 500 equity risk premium, 1990-2021

A bottom line from BlackRock Fundamental Equities: All told, we are constructive on U.S. equities. The biggest risk to our view, now 18 months into the global pandemic, remains COVID-19. We see stocks managing through the Delta wave, with evidence of peaking cases in the U.S. juxtaposed with a palpable desire to return to "normal." Yet further COVID upsets remain the one variable that is difficult to factor into our calculus, ensuring a necessary measure of humility.

Download full report

Tony DeSpirito

BlackRock Fundamental Active Equity Investment Team

This material is provided for educational purposes only and is not intended to be relied upon as a forecast, research or investment advice, and is not a recommendation, offer or solicitation to buy or sell any securities or to adopt any investment strategy. The opinions expressed are as of September 2021, and may change as subsequent conditions vary. The information and opinions contained in this material are derived from proprietary and nonproprietary sources deemed by BlackRock to be reliable, are not necessarily all-inclusive and are not guaranteed as to accuracy. Past performance is no guarantee of future results. There is no guarantee that any forecasts made will come to pass. Reliance upon information in this material is at the sole discretion of the reader. The material was prepared without regard to specific objectives, financial situation or needs of any investor.

This material may contain “forward-looking” information that is not purely historical in nature. Such information may include, among other things, projections, forecasts, estimates of yields or returns, and proposed or expected portfolio composition. Moreover, where certain historical performance information of other investment vehicles or composite accounts managed by BlackRock, Inc. and/or its subsidiaries (together, “BlackRock”) has been included in this material, such performance information is presented by way of example only. No representation is made that the performance presented will be achieved, or that every assumption made in achieving, calculating or presenting either the forward-looking information or the historical performance information herein has been considered or stated in preparing this material. Any changes to assumptions that may have been made in preparing this material could have a material impact on the investment returns that are presented herein by way of example.

Investing involves risk. Equities may decline in value due to both real and perceived general market, economic, and industry conditions. Diversification does not ensure profits or protect against loss.

You should consider the investment objectives, risks, charges and expenses of any BlackRock mutual fund carefully before investing. The prospectus and, if available, the summary prospectus contain this and other information about the fund and are available, along with information on other BlackRock funds, by calling 800-882-0052 or from your financial professional. The prospectus should be read carefully before investing.

Prepared by BlackRock Investments, LLC, member FINRA.

Not FDIC Insured | May Lose Value | No Bank Guarantee

© 2021 BlackRock, Inc. All Rights Reserved. BLACKROCK is a trademark of BlackRock, Inc. All other trademarks are those of their respective owners.

USRRMH0921U/S-1835343

© BlackRock

Read more commentaries by BlackRock