Chief Economist Scott Brown discusses current economic conditions.

The economy strengthened considerably in the first half of this year, much more than the headline GDP figure would suggest. The key components, consumer spending and business fixed investment, each rose at double-digit percentage rates. Higher inflation is widely expected to be transitory, but there are concerns that it could last longer and lead to a higher trend. The delta variant is a wildcard.

Real GDP rose at a 6.5% annual rate in the advance estimate for 2Q21, following +6.3% in 1Q21 (averaging 6.4% in 1H21). Inventories fell in the first quarter and even more sharply in the second, lopping nearly 2 percentage points from headline GDP growth in the first half. The trade deficit rose, subtracting a full percentage point. Consumer spending rose at an 11.8% annual rate in 2Q21 (following +11.4% in 1Q12), while business fixed investment rose at an 8.0% pace (following 12.9%). This is extremely strong.

The monthly data showed a mix in consumer spending. Spending on services picked up, while spending on consumer durables decreased. One of the surprises in the pandemic has been the strength in consumer durables (a 31.2% increase from February 2020 to June 2021, up 22.7% adjusting for inflation). Spending on services is now up 0.5% relative to the pre-pandemic level (although still down 3.1% adjusting for inflation). The areas hit hardest by the pandemic (transportation, restaurants, live entertainment, etc.) improved significantly in the first half of the year and there is potential for further strengthening in the second half. We can expect a further moderation in spending on consumer durables as services rebound.

Inflation is elevated. The PCE Price Index, the Fed’s key inflation gauge, rose 4.0% in the 12 months ending in June (in comparison, the Consumer Price Index rose 5.0%). Some of this reflects base effects (a rebound from the low levels of a year ago -- the PCE Price Index was up just 0.5% in the 12 months ending June 2020). Some of the increase reflects restart pressures. Production bottlenecks and materials shortages occur in every recession. They are more intense this time because of the speed of the recovery.

Click here to enlarge

Will the surge in cases of the delta variant have an economic impact? Most likely. It’s difficult to model. The delta variant is more contagious, even passed along by people who have already been vaccinated. The experiences in the U.K. and India suggest that, while not good, the rise in the delta variant may be soon contained (relatively speaking), but it’s hard to say. Many people are expected to cram in a vacation (or two) before the school year begins, spreading the delta variant more widely, and the kids may spread it around further once in school. Much depends on efforts to contain the virus. Even a partial lockdown seems unlikely at this point, but we will likely see an increase in voluntary social distancing, which means a slower recovery in consumer services.

Recall that following a sharp (but partial) rebound in 3Q20, the recovery lost steam in 4Q20 (but strengthened again in 1H21). We could see a more lackluster growth trend in the months ahead, but the recovery should continue. The Fed can be patient for now. Any increase in short-term interest rates is a long way off, but tapering is under discussion and will depend on the data.

Recent Economic Data

The Federal Open Market Committee left short-term interest rates and the monthly pace of asset purchases unchanged, but noted that “the economy has made progress” towards its goals (but not “substantial progress”).

In its World Economic Outlook, the IMF left its forecast for 2021 global growth at 6.0%, but saw sharper divisions across countries (related to the availability of vaccines and the rise of the delta variant).

Real GDP rose at a 6.5% annual rate in the advance estimate for 2Q21 (vs. +6.3% in 1Q21), held back by inventory declines, higher imports (which have a negative sign in the GDP calculation), and lower government spending (relative to 1Q21). Real consumer spending rose 11.8%, while business fixed investment rose 8.0%.

Click here to enlarge

The Employment Cost Index rose 0.7% in the three months ending in June (+2.9% y/y, slightly higher than the +2.7% y/y figure for June 2020). Wages and salaries rose 0.9% (+3.2% y/y). Benefits rose 0.4% (+2.2% y/y).

Personal income edged up 0.1% in June, as a 0.7% gain in wages income offset an 11.0% drop in unemployment benefits. Personal Spending rose 1.0%, as a 1.2% gain in services offset a 1.5% decrease in durable goods.

Click here to enlarge

The PCE Price Index rose 0.5% in June (+4.0% y/y), up 0.5% (+3.5% y/y) ex-food & energy. The Dallas Fed’s Trimmed-Mean PCE Price Index (the largest price moves are thrown out) rose 0.2% in June (+2.0% y/y).

The Conference Board’s Consumer Confidence Index was little changed at 129.1 in the initial estimate for July (vs, 128.9 in June), still at a high level.

Gauging the Recovery

The New York Fed’s Weekly Economic Index edged down to +8.37% for the week ending July 24, vs. +8.94% a week earlier, signifying strength relative to the depressed level of a year ago. The WEI is scaled to year-over- year GDP growth (GDP fell 9.1% y/y in 2Q20 and rose 12.2% y/y in 2Q21).

Click here to enlarge

Breakeven inflation rates (the spread between inflation-adjusted and fixed-rate Treasuries, not quite the same as inflation expectations, but close enough) continue to suggest a moderately higher near-term inflation outlook. The 5- to 10-year outlook remains consistent with the Fed’s long-term goal of 2%.

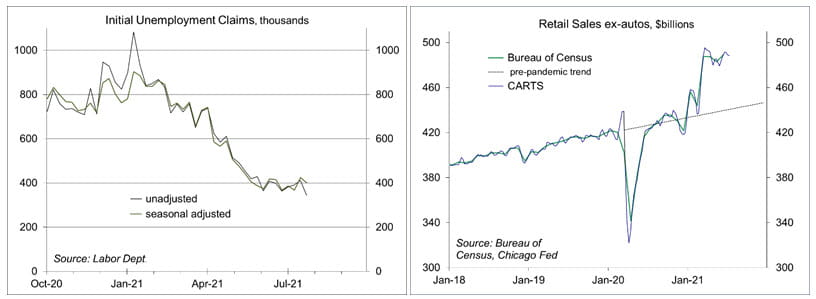

Jobless claims fell by 24,000, to 400,000 in the week ending July 24. Seasonal adjustment can be quirky in July, but the downtrend appears to have flattened in recent weeks.

Click here to enlarge

In the second week in July, the Chicago Fed Advance Retail Trade Summary (CARTS) data (based on multiple sources) showed a 0.1% decrease in retail sales (ex-autos), following a 0.4 decline in the previous week. July sales were projected to be unchanged from June.

The University of Michigan’s Consumer Sentiment Index edged up fell to 81.2 in the mid-month assessment for July (the survey covered June 23 to July 26), vs. 80.8 at mid-month, but down from 85.5 in June. Consumers generally expect higher inflation to be transitory, but remained concerned.

The opinions offered by Dr. Brown are provided as of the date above and subject to change. For more information about this report – to discuss how this outlook may affect your personal situation and/or to learn how this insight may be incorporated into your investment strategy – please contact your financial advisor or use the convenient Office Locator to find our office(s) nearest you today.

This material is being provided for informational purposes only. Any information should not be deemed a recommendation to buy, hold or sell any security. Certain information has been obtained from third-party sources we consider reliable, but we do not guarantee that such information is accurate or complete. This report is not a complete description of the securities, markets, or developments referred to in this material and does not include all available data necessary for making an investment decision. Prior to making an investment decision, please consult with your financial advisor about your individual situation. Investing involves risk and you may incur a profit or loss regardless of strategy selected. There is no guarantee that the statements, opinions or forecasts provided herein will prove to be correct.