This week US CPI inflation for June rose at a stunning 0.9% MoM, or 11% annualized, placing it among the highest sequential inflation readings in the past 40 years. Sure, much of the reading can be chalked up to used car prices and airline tickets, which are unlikely to continue to rise at this pace and may actually fall back. Still, food inflation rose 0.8% MoM, energy inflation rose 1.5% MoM, and rents increased 0.5% MoM. When food, energy and rent prices rise like this it inevitably starts to crimp consumer confidence and consumption related activity. That may be what we are seeing now.

The rest of this piece will focus on the recently released University of Michigan consumer survey for June, and we’ll try to draw the connection between inflation and consumer related activity.

In the first chart here we are showing 1-year forward inflation expectations according to the survey. At 4.8%, this June reading was the second highest going back to 2000.

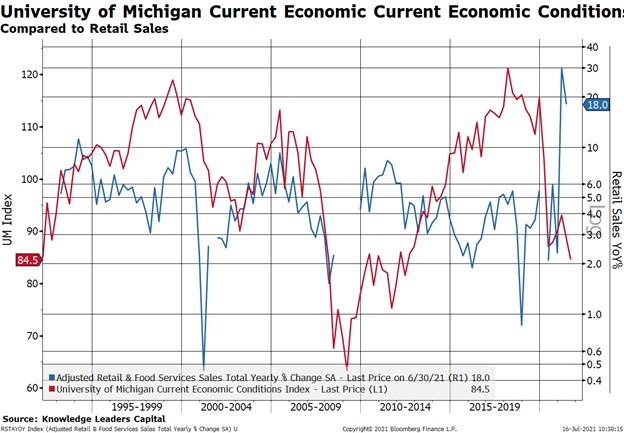

Meanwhile, survey respondents are saying current economic conditions are plummeting. Current conditions have fallen from the high 90s back toward 84.5, which is on par with the depressed readings from the 2010-2011 period.

It’s not just current conditions that are deteriorating, it’s expectations about the future as well. As the reader can see, consumer expectations have fallen from the mid-80s back to the high 70s in recent months as inflation has surged.

We think the rise in inflation expectations and the fall back in consumer confidence/expectations are directly related. For example, the most respondents since the early 1980s think now is a bad time to buy a house. Recall that in the early 1980s mortgage rates were in the mid-teens. Today, mortgage rates are in the low 3% range, suggesting that the issue today is not interest rates but house prices/inventory (obviously). The point is that the cure for the housing problem today may be somewhat more complicated than in the 1980s since lower rates won’t necessarily fix the problem.

The same can be said for autos. The highest level of respondents since the early 1980s think now is a bad time to buy a car. No wonder they think this since used car prices jumped 10% MoM in June. At least on the auto front we remain optimistic that a slow normalization of supply chain bottlenecks will resolve the inventory and pricing issues we are seeing currently.

Our concern here is that rising costs of living expenses in general will soon affect consumption (especially consumption of non-essentials) in a rather large and obvious way. Retail sales in June rose 18% YoY, but the relationship between retail sales and consumer confidence suggests retail sales growth could fall sharply in the months ahead as consumers bide their income and savings amid surging prices.