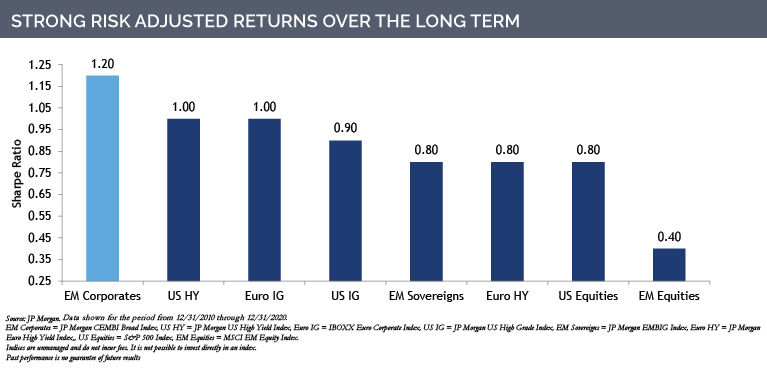

For some time, bond investors have been yield hungry, even starved. In such an environment, emerging market (EM) corporate debt has stood out for its potential yield premiums. However, this characteristic is only part of a broader favorable picture. Consider that on a risk-adjusted basis, EM corporate debt has bested other major asset classes over the long term. With its strong risk/reward and incremental spread, we believe EM corporates offer an investment opportunity for a variety of objectives, including total return, income and liability matching.

Within the broader EM debt universe, we believe EM corporates have a particularly strong value proposition. Here are some reasons why:

- Over time, the EM corporate universe has become more robust with an expansion of sectors and issuers. At five times the size of the EM sovereign segment, the EM corporate debt universe consists of approximately 1,000 corporate and quasi-sovereign issuers. This has meant more choices for investors.

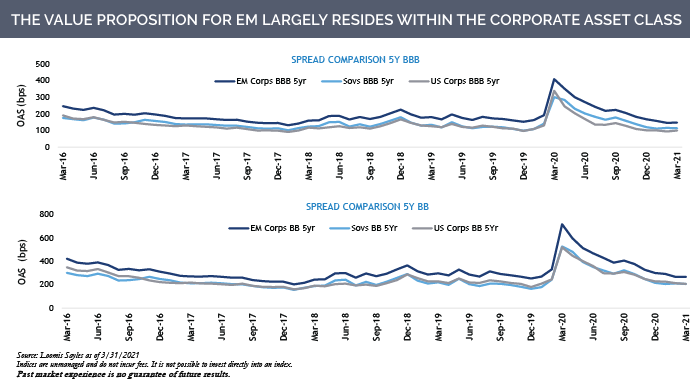

- EM corporate credit ratings often belie underlying business metrics because, according to ratings agency methodology, companies generally cannot be rated above their sovereign rating. So on a fundamental basis, some EM corporates can be significantly higher quality than their credit ratings indicate.

- In contrast to bond issuers in developed markets, we believe EM corporate bond issuers are more often driven to achieve an investment grade rating. Comparatively, EM corporates tend to issue debt for productive purposes rather than financial engineering.

- Looking at defaults in recent years, EM high yield (HY) sovereigns have outpaced that of EM HY corporates. In 2020, the default rate for EM sovereign HY issues increased by double digits compared to a fairly benign 3.5% for EM HY corporates.