Chief Economist Scott Brown discusses the latest market data.

Nonfarm payrolls rose by 559,000 in the initial estimate for May (+973,000 before seasonal adjustment), down 7.6 million (-5.0%) from February 2020 (although we would have added more than two million jobs if not for the pandemic, leaving us about 9.6 million below the pre-pandemic trend). Leisure and hospitality added 293,000 (still down 15% from February 2020). The three-month average payroll gain was 541,000. The unemployment rate fell to 5.8% (from 6.1% in April), due partly to a drop in labor force participation.

The Fed Beige Book reported that economic growth was “moderate,” although “somewhat faster” than the previous assessment. Firms reported difficulties in hiring, especially for low-wage workers, truck drivers and skilled tradespeople, but wage increases were described as “moderate” overall. Input price pressures increased further, which “some” businesses could pass along. The ISM Manufacturing Index rose to 61.2 in May (vs. 60.7 in April), reflecting faster growth in new orders and production. The ISM Services Index rose to a record 64.0 in May (vs. 62.7 in April), with faster growth in business activity and new orders. Both reports indicated longer supplier delivery times, rising order backlogs and increased input price pressures. Unit motor vehicle sales fell 9.5% in May, reflecting production constraints (semiconductor shortage).

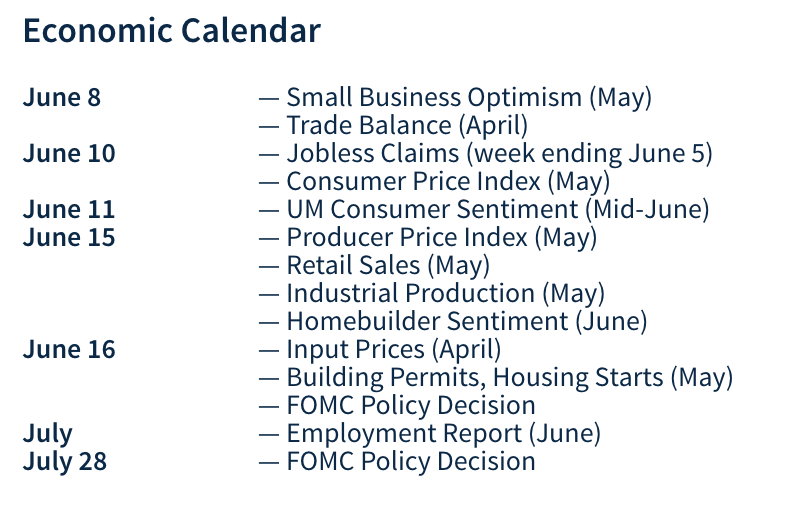

Next week, the economic calendar thins out but investors will pay close attention to the May Consumer Price Index. Base effects (a rebound from the low levels of a year ago) will continue (the CPI rose 0.1% y/y in April 2020 and is expected to be up about 4.5% y/y in May 2021). Bottleneck pressures and materials shortages are more likely to show up in the PPI, but some may add to the CPI in the near term.