Chief Economist Scott Brown discusses current economic conditions.

Real GDP rose at a 6.4% annual rate in the government’s second estimate of first quarter GDP growth, the same as in the advance estimate. However, Private Domestic Final Purchases (GDP less government, net exports, and the change in inventories), a better measure of underlying domestic demand, rose at an 11.3% annual rate (vs. +10.6% in the advance estimate). Demand outpaced supply, reflected by a decrease in inventories and a wider trade deficit.

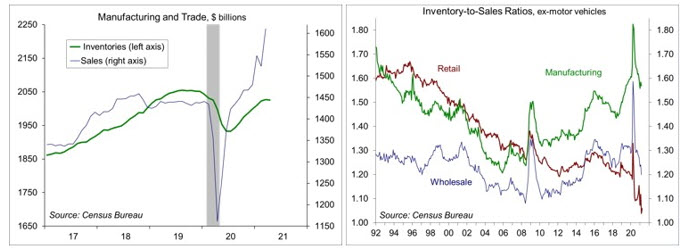

In the revised GDP report, real (that is, inflation adjusted) consumer spending rose at an 11.3% annual rate in 1Q21 (revised from +10.7%), led by a 48.6% pace in durable goods. Business fixed investment rose 10.8% (vs. 9.9%), as strength in intellectual property products and equipment offset further weakness in business structures. Residential fixed investment (homebuilding and improvements) rose 12.7% (revised from +10.8%). Net exports subtracted 1.2 percentage points from headline GDP growth, while a drop in inventories subtracted 2.8 percentage points. Note that the change in inventories contributes to the level of GDP, so the change in the change in inventories contributes to GDP growth (in this case, we went from moderate inventory growth in 4Q20 to a large inventory decline in 1Q21). Inflation-adjusted inventories fell across all major categories in the first quarter, but the decline was especially pronounced in retail autos. The semiconductor shortage has led to some softness in motor vehicle production (reported down 4.3% in the Fed’s industrial production report for April) and in new orders (down 6.2% in April). Retail auto inventories will be rebuilt, but it’s likely to take some time.

Click here to enlarge

What about non-auto inventories? Manufacturing, wholesale, and non-auto retail inventories are all higher than they were before the pandemic. Inventory-to-sales ratios are not terribly out of line with pre-pandemic figures, but retail inventories are leaner. That may be part of a longer trend, reflecting increased online sales – a trend that accelerated during the pandemic. However, we should be careful in looking at broad categories, as changes in individual industries can alter the inventory-to-sales ratio. Demand for consumer goods should moderate as consumer services recover, fiscal stimulus fades, and household savings are depleted.

Some have suggested that the pandemic exposed weakness in just-in-time inventory management. The trade policy issues of the last few years have led most major manufacturers to secure supply chains, planning alternatives to possible disruptions, but the pandemic has restrained production in many areas. In addition, some of the manufacturing surveys suggest that firms may have hoarded inputs in anticipation of higher prices. That is, fear of inflation in prices of raw materials leads to actual inflation in prices of raw materials – but eventually, firms have enough and prices begin to relax. Short-term spikes in commodity prices have been a recurring phenomenon in recent decades, but never with a sustained increase in consumer price inflation.

Inventory rebuilding may have a moderate impact on GDP growth in the quarters ahead, but the bigger issue will be the rebound in consumer services and associated labor market dynamics. We should find out a little more in the May Employment Report. (3612437)

Recent Economic Data

Real GDP rose at a 6.4% annual rate in the 2nd estimate for 1Q21, same as the advance estimate. However, the key components (consumer spending, business fixed investment, residential investment) were revised up. Private Domestic Final Sales rose at an 11.3% annual rate (vs. +10.6% in the advance estimate).

Personal income fell 13.1% in April, reflecting a pull back from March stimulus payments. Private-sector wage and salary income rose 1.1%, following a similar rise in March (+19.4% y/y).

Click here to enlarge

Personal spending rose 0.5%, reflecting a 4.1% increase in motor vehicles. Spending on services rose 1.1%, offset partly by reduced spending on nondurables and non-auto durables. Adjusted for inflation, consumer spending fell 0.1%, following a 4.1% jump in March (+24.0% y/y).

The PCE Price Index rose 0.6% in April (+3.6% y/y), up 0.7% ex-food & energy (+3.1% y/y). Note that the PCE Price Index rose 0.5% in the 12 months ending April 2020 (+0.9% y/y ex-food & energy). The Dallas Fed’s Trimmed-Mean PCE Price Index rose 0.2% in April (+1.8% y/y).

Click here to enlarge

Durable Goods Orders fell 1.3% in April, reflecting a 6.2% decline in motor vehicle (semiconductor shortage), but up 1.0% ex-transportation. Orders for nondefense capital goods ex-aircraft rose 2.3%.

The Chicago Business Barometer rose to 75.2 in May, the highest since November 1973. The Pending Home Sales Index fell 4.4% in April (+51.7% y/y), reflecting supply constraints.

Gauging the Recovery

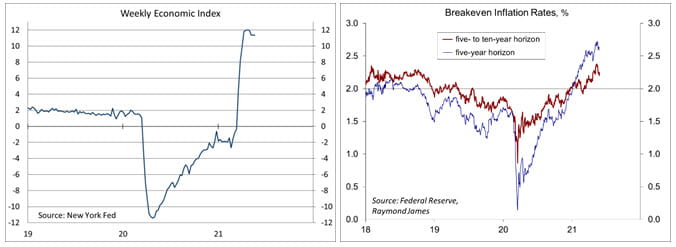

The New York Fed’s Weekly Economic Index was little changed, at +11.35% for the week ending May 22, vs. +11.37% a week earlier (revised from +11.58%), signifying strength relative to the terrible level of a year ago. The WEI is scaled to year-over-year GDP growth (GDP was down 9.0% y/y in 2Q20).

Click here to enlarge

Breakeven inflation (the spread between inflation-adjusted and fixed-rate Treasuries, not quite the same as inflation expectations) continues to suggest a moderately higher inflation outlook for the next five years. The 5-10-year outlook has crept above the Fed’s long-term goal of 2% (worth keeping an eye on).

As more people become vaccinated, the number of COVID-19 cases continues to trend lower. Despite the downtrend in new cases, we are still losing more than 3,000 people per week (vs. 4,000 at the end of April).

Click here to enlarge

Jobless claims fell by 34,000, to 444,000 (another pandemic low), in the week ending May 15. Claims are trending lower, but are still well above pre-pandemic levels (a little over 200,000).

The University of Michigan’s Consumer Sentiment Index fell to 82.8 in the mid-month assessment for May (the survey covered April 28 to May 12), vs. 88.3 in April and 84.9 in March. The increase reflected growing concerns about inflation. The expected inflation rate for the next year rose to 4.6% (from 3.4% in April), while the expected rate for the next five years rose to 3.1% (from 2.7%). Two-thirds of those surveyed expect the Fed to raise short-term interest rates within a year.

The opinions offered by Dr. Brown are provided as of the date above and subject to change. For more information about this report – to discuss how this outlook may affect your personal situation and/or to learn how this insight may be incorporated into your investment strategy – please contact your financial advisor or use the convenient Office Locator to find our office(s) nearest you today.

This material is being provided for informational purposes only. Any information should not be deemed a recommendation to buy, hold or sell any security. Certain information has been obtained from third-party sources we consider reliable, but we do not guarantee that such information is accurate or complete. This report is not a complete description of the securities, markets, or developments referred to in this material and does not include all available data necessary for making an investment decision. Prior to making an investment decision, please consult with your financial advisor about your individual situation. Investing involves risk and you may incur a profit or loss regardless of strategy selected. There is no guarantee that the statements, opinions or forecasts provided herein will prove to be correct.

© Raymond James

Read more commentaries by Raymond James