High-yield bonds remain attractive, but keep an eye on recovery rates

While it’s true that high-yield bonds’ price appreciation is limited by already tight credit spreads, there are also technical factors working in their favor. For example, default rates are declining as Gross Domestic Product expands.

In further good news for the asset class, recovery rates on defaults are also improving from the concerningly low levels of recent months, as energy-sector defaults have worked through the system.

However, recovery rates are still well below their historical level. This indicates weak bond covenants, which means higher intrinsic risk for investors. We went into the pandemic with already weak covenants in the high-yield arena. Then, coming out of recession, more companies issued bonds—and many stayed afloat thanks to strong monetary and fiscal policy support. Usually, coming out of recession, covenants start to tighten. That didn’t happen this time.

At the most basic level, it’s important to keep in mind that high-yield bonds have tended to do well coming out of recessions. We always seek to participate in price uptrends when supported by our models—and have welcomed the recent strength—but even if high yields were to trade sideways for a while, we see the yield they offer as attractive relative to the risk taken.

Of course, all that could change. A fast-surging 10-year Treasury rate to 2% or beyond could quickly swing investors from optimistic to fearful. Problems with the vaccination rollout could also change the investment picture. Longer term, a stubbornly poor employment picture—new jobless claims are still at recessionary levels—may wear out investors’ positive outlook. There is, after all, no guarantee the economy will regain its pre-pandemic footing.

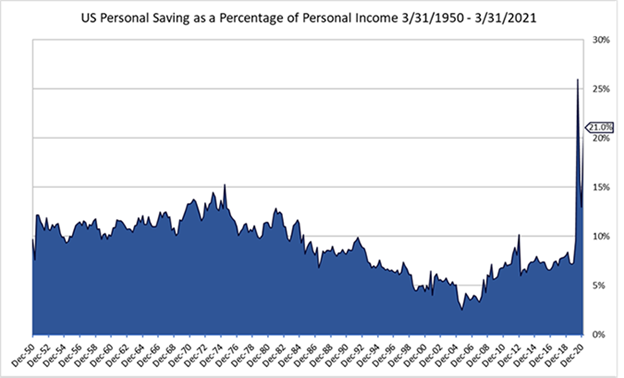

Another potential concern is American consumers’ high savings rate. As shown in the chart below, the savings rate skyrocketed last year. If all that savings starts hitting the marketplace, inflation pressure could be substantial as consumer demand leads to suppliers’ price hikes. This could be a factor as soon as the second quarter—or markets may look beyond it.

Savings rate skyrocketed last year; remains above 1970s all-time high

Source: Bloomberg