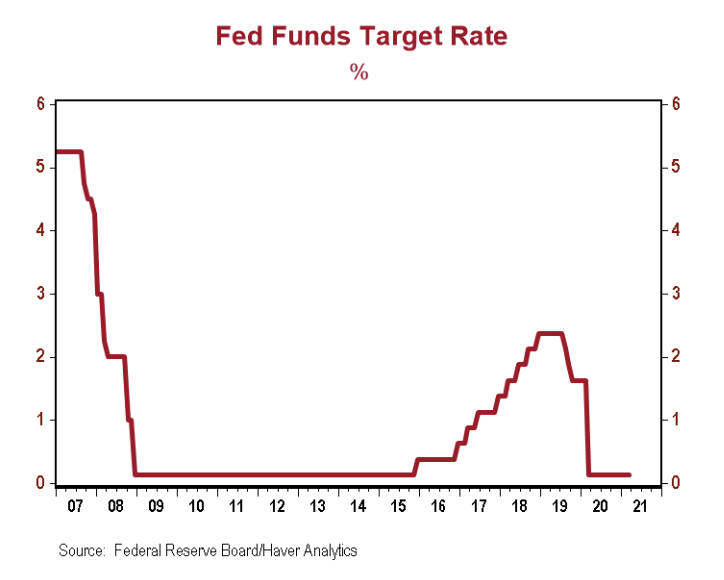

Nobody expected the Fed would lift interest rates today. In fact, virtually nobody expects them to raise rates before the end of next year (and the March dot plots show the Fed’s own forecasts have them on hold through 2023). But there are actions – such as tapering asset purchases – that are likely to come before rates lift off. And indeed, this was the first question out of the gate as the Q&A portion of Chair Powell’s press conference began. In response, the Chairman stated that the Fed is not even “talking about talking about tapering,” before elaborating on a few of the reasons the Fed expects to be on pause for the foreseeable future.

First, on employment, the Fed wants to see a string of strength in job creation. While the March gains were strong, it was only one month, and nonfarm payrolls remain down more than 8.4 million from pre-COVID levels. Even with record employment growth in 2021, the employment market is likely to remain below pre-COVID levels for a while. The economy is not a light switch, and when things were shut down last year, it caused lasting damage. Hundreds of thousands of companies closed their doors, and it will take time for jobs to get back to where they were. With damage concentrated among low-income jobs, the employment mandate is likely to be the key factor keeping policy accommodative for a while.

Chair Powell also reiterated the Fed's belief that labor market slack – and not the massive increase in the M2 money supply – will be the primary factor preventing inflation from moving sustainably higher. In the short term, he said, inflation is being pushed higher for two reasons: 1) base effects, meaning that readings will run high in the short-term simply due to the low levels we are coming off of, and 2) supply chain bottlenecks, which the Fed expects will be resolved as companies and workers get back towards normal. In effect, the Fed puts little weight on the above-trend inflation readings that look likely in the coming months. We expect that inflation pressure from massive money printing will sustain even as supply chain issues ease, but only time will tell. In the meantime, the Fed will continue to purchase Treasury securities at a pace of $80 billion per month, and agency mortgage-back securities at a pace of $40 billion monthly. For now, the Fed will remain incredibly accommodative. This means faster economic growth (and positive backdrop for equities), but the risk into the future of too loose for too long is rising. The good news is that entrepreneurship is not dead, businesses will re-open, and the US will benefit from productivity gains as a by-product of technology adoption forced by the COVID-19 disaster. Growth will continue, and at an above-trend pace, but the sugar high from spending and loose policy warrants careful scrutiny in the year ahead.

Brian S. Wesbury, Chief Economist Robert Stein, Deputy Chief Economist

Text of the Federal Reserve's Statement: The Federal Reserve is committed to using its full range of tools to support the U.S. economy in this challenging time, thereby promoting its maximum employment and price stability goals. The COVID-19 pandemic is causing tremendous human and economic hardship across the United States and around the world. Amid progress on vaccinations and strong policy support, indicators of economic activity and employment have strengthened. The sectors most adversely affected by the pandemic remain weak but have shown improvement. Inflation has risen, largely reflecting transitory factors. Overall financial conditions remain accommodative, in part reflecting policy measures to support the economy and the flow of credit to U.S. households and businesses. The path of the economy will depend significantly on the course of the virus, including progress on vaccinations. The ongoing public health crisis continues to weigh on the economy, and risks to the economic outlook remain. The Committee seeks to achieve maximum employment and inflation at the rate of 2 percent over the longer run. With inflation running persistently below this longer-run goal, the Committee will aim to achieve inflation moderately above 2 percent for some time so that inflation averages 2 percent over time and longer‑term inflation expectations remain well anchored at 2 percent. The Committee expects to maintain an accommodative stance of monetary policy until these outcomes are achieved. The Committee decided to keep the target range for the federal funds rate at 0 to 1/4 percent and expects it will be appropriate to maintain this target range until labor market conditions have reached levels consistent with the Committee's assessments of maximum employment and inflation has risen to 2 percent and is on track to moderately exceed 2 percent for some time. In addition, the Federal Reserve will continue to increase its holdings of Treasury securities by at least $80 billion per month and of agency mortgage‑backed securities by at least $40 billion per month until substantial further progress has been made toward the Committee's maximum employment and price stability goals. These asset purchases help foster smooth market functioning and accommodative financial conditions, thereby supporting the flow of credit to households and businesses.

In assessing the appropriate stance of monetary policy, the Committee will continue to monitor the implications of incoming information for the economic outlook. The Committee would be prepared to adjust the stance of monetary policy as appropriate if risks emerge that could impede the attainment of the Committee's goals. The Committee's assessments will take into account a wide range of information, including readings on public health, labor market conditions, inflation pressures and inflation expectations, and financial and international developments. Voting for the monetary policy action were Jerome H. Powell, Chair; John C. Williams, Vice Chair; Thomas I. Barkin; Raphael W. Bostic; Michelle W. Bowman; Lael Brainard; Richard H. Clarida; Mary C. Daly; Charles L. Evans; Randal K. Quarles; and Christopher J. Waller.

© First Trust Advisors

Read more commentaries by First Trust Advisors