The Sugar High Economy

Mix extremely loose monetary policy, a federal government cutting checks like it’s going out of style, and extensive roll-out of the COVID-19 vaccines, and what do you get? Answer: Some really strong economic data.

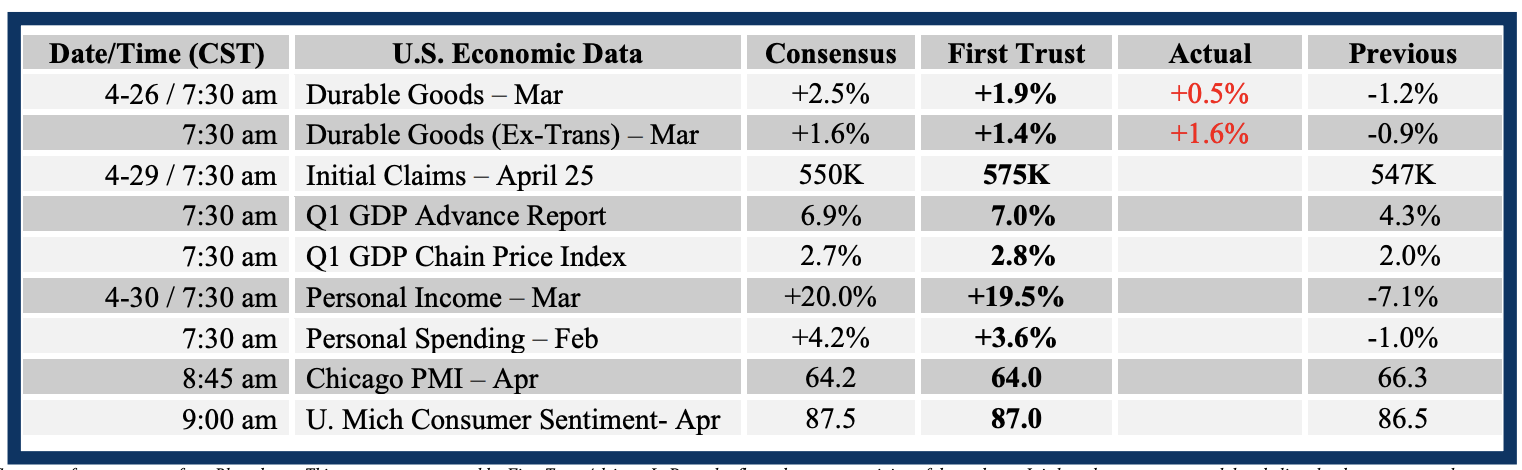

The problem is that this rapid growth, like a “sugar high,” is not going to last. Look for the economy to slow in the future as unprecedented government spending and Federal Reserve money printing slow from the current torrid pace, while we continue to suffer the absence of small businesses that went under during the crisis. The good news is that entrepreneurship is not dead, businesses will re-open, and the US will benefit from productivity gains as a by-product of technology adoption forced by the COVID-19 disaster. The other key is Washington, DC. Tax rates are going up, the only questions are when and by how much? Raising the top capital gains and dividends tax rates to 43.4% (with a personal rate of 39.6% and a Medicare tax of 3.8%) would be a steep hurdle for investors, but we think the most likely outcome is a compromise that doesn’t raise these tax rates nearly that high. In the meantime, this Thursday should deliver a report of about 7.0% annualized real GDP growth in Q1, although we may refine our guess later this week based on reports on deliveries of capital goods as well as international trade and inventories. Here’s how we calculate 7.0% annualized growth in real GDP for Q1:

Consumption: Car and light truck sales rose at a 16.9% annual rate in Q1, while “real” (inflation-adjusted) retail sales outside the auto sector soared at a 29.1% annual rate. We only have reports on spending on services through February, but it looks like real services spending should be up slightly for the quarter. As a result, we estimate that real consumer spending on goods and services, combined, increased at a 10.9% annual rate, adding 7.4 points to the real GDP growth rate (10.9 times the consumption share of GDP, which is 68%, equals 7.4).

Business Investment: The first quarter should look a lot like the last quarter of 2020, as investment in equipment continued to rebound sharply, investment in intellectual property likely grew at a more moderate pace, and commercial construction continued to decline. Combined, business investment looks like it grew at a 7.5% annual rate, which would add 1.0 points to real GDP growth. (7.5 times the 13% business investment share of GDP equals 1.0).

Home Building: Residential construction continued to grow rapidly in Q1. We think home building has much further to grow given the shortage of homes in many places around the country, and the increased appetite for houses with more square footage in the suburbs. We estimate growth at a 16.5% annual rate in Q1, which would add 0.8 points to the real GDP growth. (16.5 times the 5% residential construction share of GDP equals 0.8).

Government: It’s hard to translate government spending into a GDP effect because only direct government purchases of goods and services (and not transfer payments like extra unemployment insurance benefits) count when calculating GDP. We estimate federal purchases grew at a 0.6% annual rate in Q1, which would add 0.1 points to real GDP growth. (0.6 times the 18% government purchase share of GDP equals 0.1).