Chief Economist Scott Brown discusses current economic conditions.

The Bureau of Economic Analysis will report the advance estimate of 1Q21 GDP growth on April 28, the day after the Federal Open Market Committee meeting. There’s always a lot of uncertainty heading into the initial GDP estimate. We don’t have all the pieces of the puzzle. Recent economic data reports have generally been stronger than expected, which is encouraging, but the first quarter figures may not tell us much about what lies ahead.

Recall that the year began with a huge surge in COVID-19 cases. We were averaging around 250,000 per day. Following a sharp, but partial, rebound in 3Q20, growth moderated considerably in 4Q20. Real GDP rose at a 4.3% annual rate, which would normally be pretty good, but that followed a 33.4% pace in the third quarter, leaving us 4.1% below the level of 4Q19. The holiday shopping season was relatively lackluster. Retail sales rose at a 0.9% annual rate (4Q20/3Q20), following sharp improvement in in the previous quarter (boosted partly by the fact that the ability to spending on consumer services was limited). Still, 4Q20 retail sales were up 3.8% y/y (vs. +4.1% y/y in 3Q20). The vaccine news was good in late 2020, but the surge in COVID-19 cases cast doubt on the strength of consumer spending into the early 2021. In contrast, consumer spending in the first three months of the year was surprisingly strong

Weather added noise to the monthly data. January and March were milder than usual, while February was exceptionally bad. Retail sales were strong for the quarter as a whole – a 34.7% annual rate (relative to 4Q20) and up 14.3% from 1Q20.

Fiscal policy played a key role, with $600 checks going out in January and another $1400 in mid-March. However, we won’t see checks going out again and much if the first quarter strength in retail sales should moderate without such support. However, with a growing number of people vaccinated, consumer services should continue to rebound, more than making up the difference. It’s likely that we’ll find the consumer spending on durables will have been pulled forward to some extent.

While consumer spending growth was strong in the first quarter, other sectors faced some headwinds. Manufacturing did not fall as much as consumer spending did a year ago. Despite a 5.0% drop in manufacturing in March 2020, factory output was still down 0.6% y/y in March 2021. Bad weather weakened manufacturing and construction activity in February, but March failed to make up the difference. Supply chain issues, exacerbated by the pandemic, have continued, preventing stronger gains in manufacturing. Builders continue to report higher input costs and a lack of skilled labor. The Fed’s Beige Book of anecdotal conditions highlighted these issues. Despite widespread supply chain disruptions, manufacturing activity “expanded further with half the Fed districts citing robust growth.” The pace of job growth “varied by industry but was generally strongest in manufacturing, construction, and leisure and hospitality.” However, “hiring remained a widespread challenge, particularly for low-wage or hourly workers, restraining job growth in some cases.” Absenteeism due to COVID-19 has been a problem throughout the pandemic, but the Beige Book noted that this was down more recently. Wage growth “accelerated slightly overall,” according to the Beige Book, “with more significant wage pressures in industries like manufacturing and construction where finding and retaining workers was particularly difficult.” Some of the Fed’s contacts mentioned raising starting pay and offering signing bonuses to attract and retain employees.

Matching unemployed workers to available jobs is likely to be a significant challenge as the economy opens up. Labor and other input costs are rising, “especially in the manufacturing, construction, retail, and transportation sectors—specifically, metals, lumber, food, and fuel prices.” Cost increases were partly attributed to supply chain disruptions, (temporarily) made worse by February’s bad weather. The Beige Book noted “widespread reports of increased selling prices also, but typically not on pace with rising costs.”

As expected, the March consumer price data showed “base effects” lifting the year-over-year increase (+2.6% in March, and we’ll likely see +3.5% or more in April). This effect is pretty well known now, and shouldn’t cause much agitation among investors. It’s likely that input cost pressures will prove to be transitory, but there is a lot of fiscal stimulus in the pipeline and there is no small debate amongst economists about whether inflation will pick up beyond the anticipated temporary increase. The key for the Fed is inflation expectations, which, while higher in the near- term outlook, remain well-anchored near the Fed’s 2% target over the longer term. That could change, but until it does, Federal Reserve policy should remain on hold.

The risks to the growth outlook remain centered on the virus, with some resistance to getting vaccinated, new strains, and an ongoing pandemic in the rest of the world. As Fed Chair Powell said, the pandemic won’t be behind us until it is behind us everywhere.

Recent Economic Data

The Fed’s Beige Book noted that “national economic activity accelerated to a moderate pace from late February to early April” (vs. “a modest pace” in the previous assessment). Hiring remained “a widespread challenge, particularly for low-wage or hourly workers, restraining job growth in some cases.” Input costs rose “across the board.” Selling prices also increased, “but typically not on pace with rising costs.”

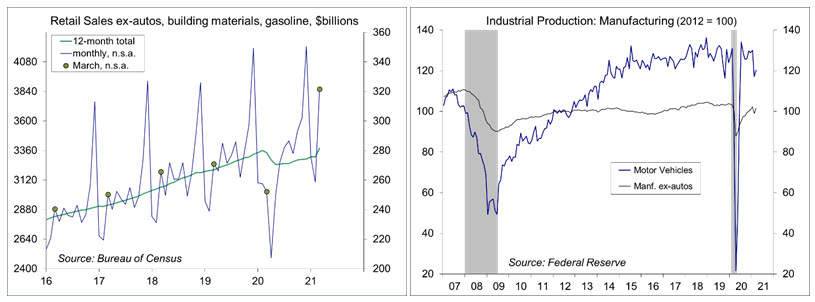

Retail sales jumped 9.8% in March (+27.7% y/y), partly reflecting a rebound from bad weather, but also supported by government checks and deposits. Core sales, which exclude autos, building materials, and gasoline, rose 7.8% (+16.8%) – with the 1Q21 average up at a 34.7% annual rate relative to 4Q20.

Click here to enlarge

Industrial production rose 1.4% in March (+1.0% y/y), held back by an 11.4% drop in the output of utilities (warmer weather). Manufacturing output rose 2.8% (+3.4% y/y), a bit disappointing following February’s 3.7% decline. Factory output for the first quarter was down 2.6% from 1Q20.

Single family building permits rose 4.6% in March, following a 9.7% drop in February, up 35.6% year-over-year. The first quarter average was up 25.6% relative to 1Q20.

Click here to enlarge

Business inventories rose 0.5% in February, down 0.7% y/y. Retail inventories, the only new information in the report, were unchanged (autos -2.6%, ex-autos +1.2%). Business sales fell 1.9% (+5.7% y/y) on bad weather.

The Consumer Price Index rose 0.6% in March (+2.6%), reflecting a 9.1% (+22.5% y/y) increase in gasoline. The increase in headline inflation mostly reflects “base effects” (a rebound from depressed figures from a year ago) and we should see about a 3.5% y/y increase in the CPI in April (as the April 2020 decline of 0.7% rolls off of the 12-month calculation).

Click here to enlarge

Ex-food and energy, the CPI rose 0.3% (+1.6% y/y). Rents have been restrained during the pandemic. Homeowners’ equivalent rent, which makes up 24% over the overall CPI and 30% of the core CPI, rose 2.0% over the last 12 months, vs. 3.2% in the 12 months before that

Click here to enlarge

Import prices rose 1.2% in March (+6.9% y/y), reflecting a 4.8% increase in the index of imported industrial supplies and materials (+29.5% y/y). Petroleum rose 6.7% (+53.9% y/y). Ex-food and fuels, import prices rose 0.8% (+3.8% y/y). Ex-fuels, the index for industrial supplies and materials rose 3.9% (+18.3% y/y).

Inflation in imported finished goods (capital, autos, and consumer goods) remained moderate, with year-over- year gains reflecting a rebound from pandemic-related weakness a year ago.

Gauging the Recovery

The New York Fed’s Weekly Economic Index rose to +11.74% for the week ending April 10, up from +9.80% a week earlier (revised from +9.52%), signifying strength relative to the weak data of a year ago. The WEI is scaled to year-over-year GDP growth.

Click here to enlarge

Breakeven inflation rates (the difference between inflation-adjusted and fixed-rate Treasuries) continue to suggest a moderately higher inflation outlook for the next five years, but the outlook five to ten years out remains close to the Fed’s long-term goal of 2% (consistent with the Fed’s revised monetary policy framework).

The trend in COVID-19 cases has edged higher in recent weeks, still relatively high (about the peak of the second wave). About 550,000 have died from COVID-19 in the U.S.

Click here to enlarge

Jobless claims fell by 193,000, to 576,000, in the week ending April 10. The overall trend is gradually lower, but data for recent weeks have been choppy and the level remains quite high by pre-pandemic standards. The continued elevated level of claims appears to partly reflect people repeatedly getting short-term work.

The University of Michigan’s Consumer Sentiment Index rose to 86.5 (a 12-month high) in the mid-month assessment for April (the survey covered March 24 to April 14), vs. 84.9 in March and 76.8 in February. In a usual recovery, expectations outpace evaluations of current conditions, but that’s not happening (expectations were unchanged at 79.7, while evaluations of current conditions rose from 93.0 to 97.2). Near- term inflation expectations have risen, but five-year-ahead expectations remained “well anchored.”

The opinions offered by Dr. Brown are provided as of the date above and subject to change. For more information about this report – to discuss how this outlook may affect your personal situation and/or to learn how this insight may be incorporated into your investment strategy – please contact your financial advisor or use the convenient Office Locator to find our office(s) nearest you today.

This material is being provided for informational purposes only. Any information should not be deemed a recommendation to buy, hold or sell any security. Certain information has been obtained from third-party sources we consider reliable, but we do not guarantee that such information is accurate or complete. This report is not a complete description of the securities, markets, or developments referred to in this material and does not include all available data necessary for making an investment decision. Prior to making an investment decision, please consult with your financial advisor about your individual situation. Investing involves risk and you may incur a profit or loss regardless of strategy selected. There is no guarantee that the statements, opinions or forecasts provided herein will prove to be correct.

© Raymond James

Read more commentaries by Raymond James